Bank of America 2003 Annual Report Download - page 47

Download and view the complete annual report

Please find page 47 of the 2003 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

-

59

-

60

-

61

|

|

The sensitivities in the preceding table and related to the Certificates

are hypothetical and should be used with caution. As the amounts

indicate, changes in fair value based on variations in assumptions

generally cannot be extrapolated because the relationship of the

change in assumption to the change in fair value may not be linear.

Also, the effect of a variation in a particular assumption on the fair

value of the retained interest is calculated without changing any other

assumption. In reality, changes in one factor may result in changes in

another, which might magnify or counteract the sensitivities.

Additionally, the Corporation has the ability to hedge interest rate risk

associated with retained residual positions. The above sensitivities

do not reflect any hedge strategies that may be undertaken to miti-

gate such risk.

Static pool net credit losses are considered in determining the

value of retained interests. Static pool net credit losses include

actual losses incurred plus projected credit losses divided by the orig-

inal balance of each securitization pool. Expected static pool net

credit losses at December 31, 2003 were 5.83 percent, 9.91 per-

Foreclosed properties amounted to $148 million and $225 mil-

lion at December 31, 2003 and 2002, respectively. The cost of car-

rying foreclosed properties amounted to $3 million, $7 million and

$15 million in 2003, 2002 and 2001, respectively.

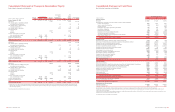

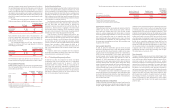

Note 8 Allowance for Credit Losses

The table below summarizes the changes in the allowance for credit

losses for 2003, 2002 and 2001:

(Dollars in millions)

2003 2002 2001

Allowance for loan and

lease losses, January 1

$6,358 $6,278 $ 6,365

Loans and leases charged off

(3,867) (4,460) (4,844)

Recoveries of loans and

leases previously charged off

761 763 600

Net charge-offs

(3,106) (3,697) (4,244)

Provision for loan and

lease losses

2,916 3,801 4,163

Other, net

(5) (24) (6)

Allowance for loan and

lease losses, December 31

$6,163 $6,358 $ 6,278

Reserve for unfunded lending

commitments, January 1

$493 $597 $ 473

Provision for unfunded lending

commitments

(77) (104) 124

Reserve for unfunded

lending commitments,

December 31

$416 $493 $ 597

Total

$6,579 $6,851 $ 6,875

Note 9 Special Purpose Financing Entities

The Corporation securitizes assets and may retain a portion or all of

the securities, subordinated tranches, interest-only strips and, in

some cases, a cash reserve account, all of which are considered

retained interests in the securitized assets. Those assets may be

serviced by the Corporation or by third parties to whom the servicing

has been sold. See Note 1 of the consolidated financial statements

for a more detailed discussion of securitizations.

Mortgage-related Securitizations

The Corporation securitizes the majority of its mortgage loan origina-

tions in conjunction with or shortly after loan closing. In 2003 and

2002, the Corporation converted a total of $121.1 billion (including

$13.0 billion originated by other entities on behalf of the Corporation)

and $53.7 billion (including $2.8 billion originated by other entities

on behalf of the Corporation), respectively, of residential first mort-

gages into mortgage-backed securities issued through Fannie Mae,

Freddie Mac, Government National Mortgage Association (Ginnie

Mae) and Banc of America Mortgage Securities. At December 31,

2003, the Corporation retained $1.7 billion of securities. The

Corporation did not retain any of the securities issued in 2002. At

December 31, 2002, $1.8 billion of securities issued prior to 2002

had been retained. These retained interests are valued using quoted

market values.

For 2003, the Corporation reported $2.4 billion in gains on loans

converted into securities and sold, of which $2.0 billion was from

loans originated by the Corporation and $381 million was from loans

originated by other entities on behalf of the Corporation. For 2002, the

Corporation reported $480 million in gains on loans converted into

securities and sold, of which $408 million was from loans originated

by the Corporation and $72 million was from loans originated by other

entities on behalf of the Corporation. At December 31, 2003, the

Corporation had recourse obligations of $531 million with varying

terms up to seven years on loans that had been securitized and sold.

In addition to the retained interests in the securities, the

Corporation has retained the servicing asset and the Certificates

from securitized mortgage loans (see the Mortgage Banking Assets

section of Note 1 of the consolidated financial statements). Mort-

gage Certificate and servicing fee income on all loans serviced,

including securitizations, was $738 million and $944 million in 2003

and 2002, respectively.

The Certificates of $2.3 billion at December 31, 2003 and

$1.6 billion at December 31, 2002 are classified as MBAs and

marked to market with gains or losses recorded in trading account

profits. At December 31, 2003, key economic assumptions and the

sensitivities of the valuations of the Certificates and MSRs to imme-

diate changes in those assumptions were analyzed. The sensitivity

analysis included the impact on fair value of modeled prepayment

and discount rate changes under favorable and adverse conditions.

A decrease of 10 percent and 20 percent in modeled prepayments

would result in an increase in value ranging from $134 million to

$282 million, and an increase in modeled prepayments of 10 percent

and 20 percent would result in a decrease in value ranging from

$122 million to $234 million. A decrease of 100 and 200 basis

points (bps) in the discount rate would result in an increase in value

ranging from $119 million to $248 million, and an increase in the

discount rate of 100 and 200 bps would result in a decrease in value

ranging from $110 million to $211 million. See Note 1 of the

consolidated financial statements for additional disclosures related

to the Certificates.

Other Securitizations

In December 2001, in conjunction with the strategic decision to exit

the subprime real estate lending business, the Corporation securitized

$17.5 billion of subprime real estate loans in two bond-insured trans-

actions and retained all of the related AAA-rated securities in the avail-

able-for-sale portfolio. During 2002, the Corporation re-securitized and

sold $10.4 billion of those securities to third parties. At December 31,

2003 and 2002, $2.1 billion and $3.5 billion, respectively, of the AAA-

rated securities remained in the available-for-sale portfolio.

The Corporation has provided protection on a subset of one

consumer finance securitization in the form of a guarantee with a

maximum payment of $220 million that is only paid out if over-

collateralization is not sufficient to absorb losses and certain other

conditions are met. The Corporation projects no payments will be due

over the life of the contract, which is approximately two years.

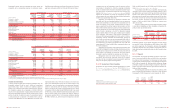

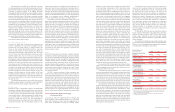

Key economic assumptions used in measuring the fair value of certain residual interests (included in other assets) in securitizations

and the sensitivity of the current fair value of residual cash flows to changes in those assumptions are as follows:

cent, 8.22 percent, 5.50 percent and 10.83 percent for 2001, 1999,

1998, 1997 and 1995, respectively. Expected static pool net credit

losses at December 31, 2002 were 6.86 percent, 8.28 percent,

6.69 percent, 5.30 percent, 4.87 percent and 6.27 percent for 2001,

1999, 1998, 1997, 1996 and 1995, respectively.

Proceeds from collections reinvested in revolving credit card

securitizations were $14.7 billion and $16.1 billion in 2003 and

2002, respectively. Other cash flows received from retained interests

that represent amounts received on retained interests by the trans-

feror other than servicing fees such as cash flows from interest-only

strips, were $279 million and $451 million in 2003 and 2002,

respectively, for credit card securitizations.

The Corporation reviews its loans and leases portfolio on a man-

aged basis. Managed loans and leases are defined as on-balance

sheet loans and leases as well as securitized credit card loans. New

advances under previously securitized accounts will be recorded on

the Corporation’s balance sheet after the revolving period of the

securitization, which has the effect of increasing loans on the

90 BANK OF AMERICA 2003 BANK OF AMERICA 2003 91

Credit Card Consumer Finance(1)

(Dollars in millions) 2003 2002 2003 2002

Carrying amount of residual interests (at fair value)

$76 $123 $328 $395

Balance of unamortized securitized loans(2)

1,782 4,732 9,409 15,545

Weighted-average life to call (in years)(3)

1.43 1.47 1.64 3.04

Revolving structures – annual payment rate

14.9% 14.2%

Amortizing structures – annual constant prepayment rate:

Fixed rate loans

7.8-32.6% 9.3-29.1%

Adjustable rate loans

27.0-42.41% 27.0%

Impact on fair value of 100 bps favorable change

$– $3 $(11) $–

Impact on fair value of 200 bps favorable change

–7(15) 2

Impact on fair value of 100 bps adverse change

–(3) 4(1)

Impact on fair value of 200 bps adverse change

–(5) 11 (2)

Expected credit losses(4)

5.3% 5.6% 4.6-11.02% 4.2-10.0%

Impact on fair value of 10% favorable change

$2 $6 $37 $40

Impact on fair value of 25% favorable change

515 100 115

Impact on fair value of 10% adverse change

(2) (7) (37) (36)

Impact on fair value of 25% adverse change

(5) (16) (82) (79)

Residual cash flows discount rate (annual rate)

6.0% 6.0% 15.0-30.0% 15.0-30.0%

Impact on fair value of 100 bps favorable change

$– $– $8 $14

Impact on fair value of 200 bps favorable change

––16 29

Impact on fair value of 100 bps adverse change

––(8) (13)

Impact on fair value of 200 bps adverse change

––(15) (26)

(1) Consumer finance includes subprime real estate loan and manufactured housing loan securitizations, which are all serviced by third parties.

(2) Balances represent securitized loans at December 31, 2003 and 2002. At December 31, 2003 and 2002, the Corporation retained in the available-for-sale portfolio $2.1 billion and $3.5 billion, respec-

tively, of the AAA-rated bonds created from the December 2001 subprime real estate loan securitizations.

(3) Before any optional clean-up calls are executed, economic analyses will be performed.

(4) Annual rates of expected credit losses are presented for credit card and commercial – domestic securitizations. Cumulative lifetime rates of expected credit losses (incurred plus projected) are presented

for consumer finance loans.