Bank of America 2003 Annual Report Download - page 48

Download and view the complete annual report

Please find page 48 of the 2003 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

-

60

-

61

|

|

92 BANK OF AMERICA 2003

a material impact on the Corporation’s results of operations or finan-

cial condition. At December 31, 2003, the remaining consolidated

assets and liabilities were reflected in available-for-sale debt securi-

ties, other assets, and commercial paper and other short-term bor-

rowings in the Global Corpo rate and Inve stme nt Banking business

segment. As of December 31, 2003, the Corporation’s loss expo-

sure associated with these entities including unfunded lending com-

mitments was approximately $6.4 billion.

Additionally, the Corporation had significant involvement with

other VIEs that it did not consolidate because it was not deemed to

be the primary beneficiary. In such cases, the Corporation does not

absorb the majority of the entities’ expected losses nor does it

receive a majority of the entities’ expected residual returns, or both.

These entities facilitate client transactions, and the Corporation func-

tions as administrator for all of these and provides either liquidity and

letters of credit or derivatives to the VIE. The Corporation typically

obtains variable interests in these types of entities at the inception

of the transaction. Total assets of these entities at December 31,

2003 and 2002 were approximately $28.7 billion and $11.1 billion,

respectively; revenues associated with administration, liquidity, let-

ters of credit and other services were approximately $334 million in

2003 and $341 million in 2002. At December 31, 2003 and 2002,

the Corporation’s loss exposure associated with these VIEs was

approximately $17.7 billion and $5.1 billion, respectively, which is net

of amounts syndicated.

Additionally, the Corporation had contractual relationships with

other VIEs that engaged in leasing or lending activities and were con-

solidated by the Corporation prior to FIN 46. The amount of assets of

these entities as of December 31, 2003 was $1.5 billion and the

Corporation’s maximum possible loss exposure was $1.3 billion.

Management does not believe losses resulting from its

involvement with the entities discussed above will be material.

See Note 1 of the consolidated financial statements for additional

discussion of special purpose financing entities.

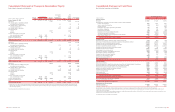

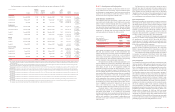

Note 10 Goodwill and Other Intangibles

At December 31, 2003 and 2002, allocated goodwill was $7.7 billion

in Consume r and Comme rcial Banking,$1.5 billion in Asse t

Manage me nt and $134 million in Equity Inve stme nts. At December 31,

2003 and 2002, goodwill was $2.1 billion and $2.0 billion, respec-

tively, in Global Corporate and Inve stme nt Banking.

In accordance with SFAS 142, no goodwill amortization was

recorded in 2003 or 2002. Goodwill amortization expense in 2001

was $662 million. Net income in 2001 was $6.8 billion or $4.26 per

common share ($4.18 per diluted common share). Net income

adjusted to exclude goodwill amortization expense would have been

$7.4 billion or $4.64 per common share ($4.56 per diluted com-

mon share) in 2001. The impact of goodwill amortization on net

income in 2001 was $616 million or $0.38 per common share

(basic and diluted).

The gross carrying value and accumulated amortization related

to core deposit intangibles and other intangibles at December 31,

2003 and 2002 are presented below:

December 31, 2003 December 31, 200

2

Gross Gross

Carrying Accumulated Carrying Accumulated

(Dollars in millions)

Value Amortization Value Amortization

Core deposit intangibles

$1,495 $ 886 $1,495 $ 726

Other intangibles

787 488 757 431

Total

$2,282 $1,374 $2,252 $1,157

Amortization expense on core deposit intangibles and other intangi-

bles was $217 million, $218 million and $216 million in 2003, 2002

and 2001, respectively. The Corporation estimates that aggregate

amortization expense will be $216 million for 2004, $214 million for

2005, $206 million for 2006, $125 million for 2007 and $61 million

for 2008.

Note 11 Deposits

The Corporation had domestic certificates of deposit of $100 thou-

sand or more totaling $32.8 billion and $23.0 billion at December

31, 2003 and 2002, respectively. The Corporation had other domes-

tic time deposits of $100 thousand or more totaling $1.0 billion and

$977 million at December 31, 2003 and 2002, respectively. Foreign

certificates of deposit and other foreign time deposits of $100 thou-

sand or more totaled $15.4 billion and $16.4 billion at December 31,

2003 and 2002, respectively.

The following table presents the maturities of domestic certifi-

cates of deposit of $100 thousand or more and of other domestic

time deposits of $100 thousand or more at December 31, 2003.

BANK OF AMERICA 2003 93

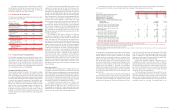

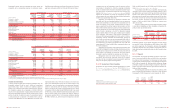

Corporation’s balance sheet and increasing net interest income and

charge-offs, with a corresponding reduction in noninterest income.

Portfolio balances, delinquency and historical loss amounts of the man-

aged loans and leases portfolio for 2003 and 2002 were as follows:

Variable Interest Entities

In January 2003, the FASB issued FIN 46 that addresses VIEs. The

Corporation adopted FIN 46 on July 1, 2003 and consolidated

approximately $12.2 billion of assets and liabilities related to

certain of its multi-seller asset-backed commercial paper conduits.

The Corporation entered into a transaction in October 2003 that

resulted in the deconsolidation of approximately $8.0 billion of the

previously consolidated assets and liabilities related to one of these

entities (the Entity). The Entity’s issuance of a subordinated note to

a third party reduced our exposure to the Entity’s losses under liq-

uidity and credit agreements as these agreements are senior to the

subordinated note issued. There was no impact to net income as a

result of the deconsolidation. There was no material impact to Tier

1 Capital as a result of consolidation or the subsequent deconsoli-

dation and prior periods were not restated. There was no material

impact to net income as a result of applying FIN 46 on July 1, 2003.

In December 2003, the FASB issued FIN 46R. FIN 46R is an update

of FIN 46 and contains different implementation dates based on the

types of entities subject to the standard and based on whether a

company has adopted FIN 46. The Corporation anticipates adopting

FIN 46R as of March 31, 2004 and does not expect that it will have

December 31, 2003 December 31, 2002

Total Principal Principal Principal Total Principal Principal Principal

Amount of Amount of Loans Amount of Amount of Amount of Loans Amount of

Loans and Past Due Nonperforming Loans and Past Due Nonperforming

(Dollars in millions)

Leases 90 Days or More(1) Loans Leases 90 Days or More(1) Loans

Commercial – domestic

$96,644 $ 110 $ 1,507 $105,053 $132 $ 2,781

Commercial – foreign

15,293 29 586 19,912 – 1,359

Commercial real estate – domestic

19,043 23 140 19,910 91 161

Commercial real estate – foreign

324 – 2 295 – 3

Total commercial

131,304 162 2,235 145,170 223 4,304

Residential mortgage

140,513 – 531 108,197 – 612

Home equity lines

23,859 – 43 23,236 – 66

Direct/Indirect consumer

33,415 47 28 31,068 56 30

Consumer finance

5,589 35 32 8,384 61 19

Credit card

36,596 647 – 29,461 502 –

Foreign consumer

1,969 – 4 1,971 – 6

Total consumer

241,941 729 638 202,317 619 733

Total managed loans and leases

373,245 $ 891 $ 2,873 347,487 $842 $ 5,037

Loans in revolving securitizations

(1,782) (4,732)

Total held loans and leases

$371,463 $342,755

Year Ended December 31, 2003 Year Ended December 31, 2002

Average Average

Loans and Loans and Loans and Loans and

Leases Leases Net Net Loss Leases Leases Net Net Loss

(Dollars in millions)

Outstanding Losses Ratio(2) Outstanding Losses Ratio(2)

Commercial – domestic

$99,000 $ 757 0.76% $110,073 $1,471 1.34%

Commercial – foreign

17,489 306 1.75 21,287 521 2.45

Commercial real estate – domestic

19,740 41 0.21 21,161 37 0.18

Commercial real estate – foreign

302 – – 408 – –

Total commercial

136,531 1,104 0.81 152,929 2,029 1.33

Residential mortgage

127,059 40 0.03 97,204 42 0.04

Home equity lines

22,890 11 0.05 22,807 26 0.11

Direct/Indirect consumer

32,593 181 0.55 30,264 210 0.69

Consumer finance

6,888 212 3.08 10,533 255 2.42

Credit card

31,552 1,691 5.36 27,352 1,443 5.28

Other consumer – domestic

–39n/m –36n/m

Foreign consumer

1,977 5 0.24 2,021 5 0.25

Total consumer

222,959 2,179 0.98 190,181 2,017 1.06

Total managed loans and leases

359,490 $ 3,283 0.91% 343,110 $4,046 1.18%

Loans in revolving securitizations

(3,342) (6,291)

Total held loans and leases

$356,148 $336,819

n/m = not meaningful

(1) Excludes consumer real estate loans, which are placed on nonperforming status at 90 days past due.

(2) The net loss ratio is calculated by dividing managed loans and leases net losses by average managed loans and leases outstanding for each loan and lease category.

Over

Three Over three six months

months months to to twelve

(Dollars in millions)

or less six months months Thereafter Total

Certificates of deposit of $100 thousand or more

$13,569 $7,163 $7,684 $4,351 $ 32,767

Other time deposits of $100 thousand or more

77 73 117 772 1,039