Bank of America 2003 Annual Report Download - page 23

Download and view the complete annual report

Please find page 23 of the 2003 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

|

|

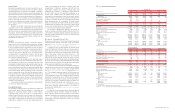

Table 8 presents total long-term debt and other obligations at

December 31, 2003.

Table 8

Long-term Debt and Other Obligations

December 31, 2003

Due in

1 year

(Dollars in millions)

or less Thereafter Total

Long-term debt and

capital leases(1) $12,193 $63,150 $ 75,343

Purchase obligations 14,074 2,850 16,924

Operating lease obligations 1,308 8,075 9,383

Other long-term liabilities 87 – 87

Total $27,662 $74,075 $101,737

(1) Includes principal payments only and capital lease obligations of $26.

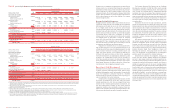

Many of our lending relationships contain both funded and unfunded

elements. The funded portion is reflected on our balance sheet. The

unfunded component of these commitments is not recorded on our

balance sheet until a draw is made under the loan facility.

These commitments, as well as guarantees, are more fully dis-

cussed in Note 13 of the consolidated financial statements.

The following table summarizes the total unfunded, or off-bal-

ance sheet, credit extension commitment amounts by expiration

date. Charge cards (nonrevolving card lines) to individuals and gov-

ernment entities guaranteed by the U.S. government in the amount

of $13.7 billion (related outstandings of $233 million) were not

included in credit card line commitments in the table below.

Table 9

Credit Extension Commitments

December 31, 2003

Expires in

1 year

(Dollars in millions)

or less Thereafter Total

Loan commitments(1)

$80,563 $131,218 $211,781

Standby letters of credit and

financial guarantees

19,077 12,073 31,150

Commercial letters of credit

2,973 287 3,260

Legally binding commitments

102,613 143,578 246,191

Credit card lines

84,940 8,831 93,771

Total

$187,553 $152,409 $339,962

(1) Equity commitments of $1,678 related to obligations to fund existing equity investments were

included in loan commitments at December 31, 2003.

On- and Off-balance Sheet Financing Entities

In addition to traditional lending, we also support our customers’

financing needs by facilitating their access to the commercial paper

markets. These markets provide an attractive, lower-cost financing

alternative for our customers. Our customers sell assets, such as

high-grade trade or other receivables or leases, to a commercial

paper financing entity, which in turn issues high-grade short-term

commercial paper that is collateralized by the assets sold.

Additionally, some customers receive the benefit of commercial paper

financing rates related to certain lease arrangements. We facilitate

these transactions and collect fees from the financing entity for the

services it provides including administration, trust services and mar-

keting the commercial paper.

We receive fees for providing combinations of liquidity, standby

letters of credit (SBLCs) or similar loss protection commitments, and

derivatives to the commercial paper financing entities. These forms

of asset support are senior to the first layer of asset support pro-

vided by customers through over-collateralization or by support pro-

vided by third parties. The rating agencies require that a certain

percentage of the commercial paper entity’s assets be supported by

both the seller’s over-collateralization and our SBLC in order to

receive their respective investment rating. The SBLC would be drawn

on only when the over-collateralization provided by the seller and third

parties is not sufficient to cover losses of the related asset. Liquidity

commitments made to the commercial paper entity are designed to

fund scheduled redemptions of commercial paper if there is a market

disruption or the new commercial paper cannot be issued to fund the

redemption of the maturing commercial paper. The liquidity facility

has the same legal priority as the commercial paper. We do not enter

into any other form of guarantee with these entities.

We manage our credit risk on these commitments by subjecting

them to our normal underwriting and risk management processes. At

December 31, 2003 and 2002, the Corporation had off-balance sheet

liquidity commitments and SBLCs to these financing entities of $23.5

billion and $34.2 billion, respectively. Substantially all of these liquid-

ity commitments and SBLCs mature within one year. These amounts

are included in Table 9. $6.4 billion of the decrease in the liquidity

commitments and SBLCs was due to the entities consolidated as a

result of FIN 46. Net revenues earned from fees associated with these

off-balance sheet financing entities were approximately $355 million

and $484 million for 2003 and 2002, respectively.

We generally do not purchase any commercial paper issued by

these financing entities other than during the underwriting process

when we act as issuing agent nor do we purchase any of the com-

mercial paper for our own account. Derivative instruments related to

these entities are marked to market through the statement of income.

SBLCs and liquidity commitments are accounted for pursuant to SFAS

No. 5, “Accounting for Contingencies” (SFAS 5), and are discussed fur-

ther in Note 13 of the consolidated financial statements.

In January 2003, the FASB issued FIN 46 that addresses off-bal-

ance sheet financing entities. We adopted FIN 46 on July 1, 2003

and consolidated approximately $12.2 billion of assets and liabilities

related to certain of our multi-seller asset-backed commercial paper

conduits. There was no material impact to Tier 1 Capital as a result

of consolidation or subsequent deconsolidation and prior periods

were not restated. On October 8, 2003, one of these entities entered

into a Subordinated Note Purchase Agreement with an unrelated third

party. As a result of the sale of the subordinated note to a third party,

we deconsolidated approximately $8.0 billion of the previously con-

solidated conduits. There was no impact to net income as a result of

the deconsolidation. In December 2003, the FASB issued FASB

Interpretation No. 46 (Revised December 2003) “Consolidation of

Variable Interest Entities, an interpretation of ARB No. 51” (FIN 46R).

FIN 46R is an update of FIN 46 and contains different implementa-

tion dates based on the types of entities subject to the standard and

based on whether a company has adopted FIN 46. We anticipate

adopting FIN 46R as of March 31, 2004 and do not expect that it will

have a material impact on our results of operations or financial

condition. There was no material impact to net income as a result

of applying FIN 46 on July 1, 2003. At December 31, 2003, the

remaining consolidated assets and liabilities were reflected in avail-

able-for-sale debt securities, other assets, and commercial paper and

other short-term borrowings in the Global Corporate and Inve stme nt

Banking business segment. As of December 31, 2003, our loss expo-

sure associated with these entities including unfunded lending com-

mitments was approximately $6.4 billion.

In addition, to control our capital position, diversify funding

sources and provide customers with commercial paper investments,

from time to time we will sell assets to off-balance sheet commercial

paper entities. The commercial paper entities are Qualified Special

Purpose Entities that have been isolated beyond our reach or that of

our creditors, even in the event of bankruptcy or other receivership.

Assets sold to the entities consist of high-grade corporate or municipal

bonds, collateralized debt obligations and asset-backed securities.

These entities issue collateralized commercial paper to third party mar-

ket participants and passive derivative instruments to us. Assets sold

to the entities typically have an investment rating ranging from Aaa/AAA

to Aa/AA. We may provide liquidity, SBLCs or similar loss protection

commitments to the entity, or we may enter into derivatives with the

entity in which we assume certain risks. The liquidity facility and deriv-

atives have the same legal standing with the commercial paper.

The derivatives provide interest rate, currency and a pre-speci-

fied amount of credit protection to the entity in exchange for the com-

mercial paper rate. These derivatives are provided for in the legal

documents and help to alleviate any cash flow mismatches. In some

cases, if an asset’s rating declines below a certain investment qual-

ity as evidenced by its investment rating or defaults, we are no longer

exposed to the risk of loss. At that time, the commercial paper hold-

ers assume the risk of loss. In other cases, we agree to assume all

of the credit exposure related to the referenced asset. Legal docu-

ments for each entity specify asset quality levels that require the

entity to automatically dispose of the asset once the asset falls

below the specified quality rating. At the time the asset is disposed,

we are required to reimburse the entity for any credit-related losses

depending on the pre-specified level of protection provided.

We also receive fees for the services we provide to the entities,

and we manage any credit or market risk on commitments or deriva-

tives through normal underwriting and risk management processes.

Derivative activity related to these entities is included in Note 6 of the

consolidated financial statements. At December 31, 2003 and 2002,

the Corporation had off-balance sheet liquidity commitments, SBLCs

and other financial guarantees to the financing entities of $5.4 billion

and $4.5 billion, respectively. Substantially all of these liquidity com-

mitments, SBLCs and other financial guarantees mature within one

year. These amounts are included in Table 9. Net revenues earned

from fees associated with these entities were $50 million and $37

million in 2003 and 2002, respectively.

We generally do not purchase any of the commercial paper

issued by these types of financing entities other than during the

underwriting process when we act as issuing agent nor do we pur-

chase any of the commercial paper for our own account. We do not

consolidate these types of entities because they are considered

Qualified Special Purpose Entities as defined in SFAS 140. Derivative

instruments related to these entities are marked to market through

the statement of income. SBLCs and liquidity commitments are

accounted for pursuant to SFAS 5 and are discussed further in Note

13 of the consolidated financial statements.

Because we provide liquidity and credit support to these financ-

ing entities, our credit ratings and changes thereto will affect the bor-

rowing cost and liquidity of these entities. In addition, significant

changes in counterparty asset valuation and credit standing may also

affect the liquidity of the commercial paper issuance. Disruption in the

commercial paper markets may result in our having to fund under

these commitments and SBLCs discussed above. We manage these

risks, along with all other credit and liquidity risks, within our policies

and practices. See Notes 1 and 9 of the consolidated financial state-

ments for additional discussion of off-balance sheet financing entities.

Capital Management

The final component of liquidity risk is capital management, which

focuses on the level of shareholders’ equity. Shareholders’ equity was

$48.0 billion at December 31, 2003 compared to $50.3 billion at

December 31, 2002, a decrease of $2.3 billion. This decrease was

driven by share repurchases of $9.8 billion, dividends paid of $4.3 bil-

lion and net unrealized losses on derivatives of $2.8 billion offset by

net income of $10.8 billion and common stock issued under employee

plans of $4.2 billion. The net impact to earnings per share of share

repurchases and issuances under employee plans in 2003 was $0.06

per share. We will continue to repurchase shares, from time to time,

in the open market or private transactions through our previously

approved repurchase plan. For additional discussion on share repur-

chases, see Note 14 of the consolidated financial statements.

We have, from time to time, sold put options on our common

stock to independent third parties. The put option program was

designed to partially offset the cost of share repurchases. As of

December 31, 2003, all put options under this program had matured

and there were no remaining put options outstanding. For additional

information on the put option program, see Note 14 of the consoli-

dated financial statements.

As part of the SVA calculation, equity is allocated to business

units based on an assessment of risk. The allocated amount of cap-

ital varies according to the risk characteristics of the individual busi-

ness segments and the products they offer. Capital is allocated

separately based on the following types of risk: credit, market and

operational. Average common equity allocated to business units was

$34.9 billion in 2003 and $35.2 billion in 2002. Average unallocated

common equity (not allocated to business units) was $14.2 billion in

2003 and $12.4 billion in 2002.

As a regulated financial services company, we are governed by

certain regulatory capital requirements. The regulatory Tier 1 Capital

ratio was 7.85 percent at December 31, 2003, a decrease of 37 bps

from a year ago, reflecting higher risk-weighted assets. The minimum

Tier 1 Capital ratio required is four percent. As of December 31, 2003,

we were classified as “well-capitalized” for regulatory purposes, the

highest classification. For additional information on the regulatory cap-

ital ratios along with a description of the components of risk-based

capital, capital adequacy requirements and prompt corrective action

provisions, see Note 15 of the consolidated financial statements.

42 BANK OF AMERICA 2003 BANK OF AMERICA 2003 43