Bank of America 2003 Annual Report Download - page 18

Download and view the complete annual report

Please find page 18 of the 2003 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

|

|

BANK OF AMERICA 2003 33

Accrued Taxes

We estimate tax expense based on the amount we expect to owe var-

ious tax jurisdictions. We currently file income tax returns in approxi-

mately 85 jurisdictions. Our estimate of tax expense is reported in

the Consolidated Statement of Income. Accrued taxes represent the

net estimated amount due or to be received from taxing jurisdictions

either currently or in the future and are reported as a component of

accrued expenses and other liabilities on the Consolidated Balance

Sheet. In estimating accrued taxes, we assess the relative merits

and risks of the appropriate tax treatment of transactions taking into

account statutory, judicial and regulatory guidance in the context of

our tax position.

Changes to our estimate of accrued taxes occur periodically due

to changes in the tax rates, implementation of new tax planning

strategies, resolution with taxing authorities of issues with previously

taken tax positions and newly enacted statutory, judicial and regula-

tory guidance. These changes, when they occur, affect accrued taxes

and can be material to our operating results for any particular quar-

ter. Taxes are discussed in more detail in Notes 1 and 18 of the con-

solidated financial statements.

Goodwill

The nature and accounting for goodwill is discussed in detail in

Notes 1 and 10 of the consolidated financial statements. Assigned

goodwill is subject to a market value recoverability test that records

a loss if the implied fair value of goodwill is less than the amount

recorded in the financial statements for any individual reporting unit.

The first part of this test is a comparison, at the reporting unit level,

of the fair value of each reporting unit to its carrying amount,

including goodwill. The reporting units utilized for this test were

those that are one level below the core business segments identi-

fied in Business Segment Operations.

The fair values of the reporting units are determined using a

discounted cash flow model. The discounted cash flows were calcu-

lated by taking the net present value of estimated cash flows using

a combination of historical results, estimated future cash flows and

an appropriate price to earnings multiple. We use our internal fore-

casts to estimate future cash flows and actual results typically differ

from forecasted results. However, these differences have not been

material and we believe that this methodology provides a reasonable

means to determine fair values. Cash flows are discounted using a

discount rate based on a weighted average cost of capital resulting

in a range of 8.7 percent to 11 percent. Weighted average cost of

capital is determined using the 10-year U.S. Treasury rate adjusted

for estimated required market returns and risk/return rates for similar

industries of the reporting unit.

Our evaluations for the year ended December 31, 2003 indicated

that none of our goodwill was impaired.

Accounting Standards

Our accounting for hedging activities, securitizations and off-balance

sheet entities requires significant judgment in interpreting and

applying the accounting principles related to these matters.

Judgments include, but are not limited to: the determination of

whether a financial instrument or other contract meets the definition

of a derivative in accordance with SFAS 133 and the applicable

hedge criteria including whether the derivative used in our hedging

transactions is expected to be or has been highly effective as a

hedge; the accounting for the transfer of financial assets and

extinguishments of liabilities in accordance with SFAS No. 140,

“Accounting for Transfers and Servicing of Financial Assets and

Extinguishments of Liabilities – a replacement of FASB Statement

No. 125” (SFAS 140) and the applicable determination as to

whether assets transferred meet the specific criteria for sale

accounting; and the determination of when certain special purpose

entities should be consolidated on our balance sheet and statement

of income in accordance with Financial Accounting Standards Board

(FASB) Interpretation No. 46 “Consolidation of Variable Interest

Entities, an interpretation of ARB No. 51” (FIN 46) and the applica-

ble determination of expected losses and returns as defined in FIN

46. For a more complete discussion of these principles, see Notes

1, 6 and 9 of the consolidated financial statements.

The remainder of Management’s Discussion and Analysis of

Results of Operations and Financial Condition should be read in con-

junction with the consolidated financial statements and related notes

presented on pages 74 through 115. See Note 1 for Recently Issued

Accounting Pronouncements.

Business Segment Operations

We provide our customers and clients both traditional banking and

nonbanking financial products and services through four business

segments: Consume r and Comme rcial Banking, Asse t Manage me nt,

Global Corporate and Inve stme nt Banking and Equity Inve stme nts.

In managing our four business segments, we evaluate results

using both financial and nonfinancial measures. Financial measures

consist primarily of revenue, net income and SVA. Nonfinancial meas-

ures include, but are not limited to, market share and customer satis-

faction. Total revenue includes net interest income on a fully

taxable-equivalent basis and noninterest income. The net interest

income of the business segments includes the results of a funds

transfer pricing process that matches assets and liabilities with simi-

lar interest rate sensitivity and maturity characteristics. Net interest

income also reflects an allocation of net interest income generated by

certain assets and liabilities used in our ALM process.

From time to time, we refine the business segment strategy and

reporting. As we continued to refine our business segment strategy

in 2002, we moved a portion of our thirty-year mortgage portfolio

from the Consume r and Comme rcial Banking segment to Corporate

Othe r. The mortgages designated solely for our ALM process were

moved to Corpo rate Othe r to reflect the fact that management deci-

sions regarding this portion of the mortgage portfolio are driven by

corporate ALM considerations and not by the business segments’

management. In the third quarter of 2002, certain consumer finance

businesses in the process of liquidation (subprime real estate, auto

leasing and manufactured housing) were transferred from Consume r

and Comme rcial Banking to Corporate Othe r and in the first quarter of

2003, certain commercial lending businesses in the process of

liquidation were transferred from Consume r and Co mme rcial Banking

to Corporate Othe r.

See Note 20 of the consolidated financial statements for addi-

tional business segment information including the allocation of

certain expenses, selected financial information for the business

segments, reconciliations to consolidated amounts and information on

Corporate Othe r. Certain prior period amounts have been reclassified

among segments and their components to conform to the current

period presentation.

32 BANK OF AMERICA 2003

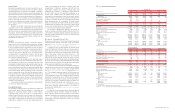

Table 4

Business Segment Summary

Consumer and

Total Corporation Commercial Banking(1) Asset Management(1)

(Dollars in millions) 2003 2002 2003 2002 2003 2002

Net interest income (fully taxable-equivalent basis)

$22,107 $21,511 $15,970 $15,205 $754 $752

Noninterest income

16,422 13,571 10,333 8,411 1,880 1,626

Total revenue

38,529 35,082 26,303 23,616 2,634 2,378

Provision for credit losses

2,839 3,697 2,062 1,806 1318

Gains on sales of debt securities

941 630 12 45 ––

Amortization of intangibles

217 218 179 175 66

Other noninterest expense

19,909 18,218 12,301 11,301 1,608 1,488

Income before income taxes

16,505 13,579 11,773 10,379 1,019 566

Income tax expense

5,695 4,330 4,252 3,836 349 191

Net income

$10,810 $9,249 $7,521 $6,543 $670 $375

Shareholder value added

$5,621 $3,760 $5,450 $4,392 $368 $81

Net interest yield (fully taxable-equivalent basis)

3.36% 3.75% 4.67% 5.26% 3.14% 3.06%

Return on average equity

21.99 19.44 36.79 33.77 23.97 14.99

Efficiency ratio (fully taxable-equivalent basis)

52.23 52.55 47.45 48.60 61.29 62.84

Average:

Total loans and leases

$356,148 $336,819 $188,706 $182,463 $23,143 $23,916

Total assets

764,132 662,943 364,703 312,973 25,851 26,079

Total deposits

406,233 371,479 312,582 283,255 13,162 12,030

Common equity/Allocated equity

49,148 47,552 20,444 19,376 2,794 2,500

Year end:

Total loans and leases

371,463 342,755 196,307 186,069 24,666 23,009

Total assets

736,445 660,951 386,330 339,976 27,540 25,645

Total deposits

414,113 386,458 326,235 297,646 14,710 13,305

Global Corporate and

Investment Banking(1) Equity Investments(1) Corporate Other

(Dollars in millions) 2003 2002 2003 2002 2003 2002

Net interest income (fully taxable-equivalent basis)

$4,825 $4,797 $(160) $(165) $718 $922

Noninterest income

4,108 3,880 (94) (281) 195 (65)

Total revenue

8,933 8,677 (254) (446) 913 857

Provision for credit losses

477 1,208 25 7274 358

Gains (losses) on sales of debt securities

(14) (97) ––943 682

Amortization of intangibles

28 32 3312

Other noninterest expense

5,407 5,031 108 88 485 310

Income before income taxes

3,007 2,309 (390) (544) 1,096 869

Income tax expense (benefit)

995 748 (141) (213) 240 (232)

Net income (loss)

$2,012 $1,561 $(249) $(331) $856 $1,101

Shareholder value added

$983 $251 $(475) $(583) $(705) $(381)

Net interest yield (fully taxable-equivalent basis)

1.98% 2.38% n/m n/m n/m n/m

Return on average equity

20.94 13.96 (11.91)% (15.56)% n/m n/m

Efficiency ratio (fully taxable-equivalent basis)

60.85 58.35 n/m n/m n/m n/m

Average:

Total loans and leases

$49,365 $63,133 $259 $440 $94,675 $66,867

Total assets

292,301 241,522 6,245 6,179 75,032 76,190

Total deposits

66,181 64,767 ––14,308 11,427

Common equity/Allocated equity(2)

9,611 11,183 2,086 2,125 14,213 12,368

Year end:

Total loans and leases

41,170 57,823 77 437 109,243 75,417

Total assets

248,833 220,241 6,251 6,064 67,491 69,025

Total deposits

58,590 67,212 ––14,578 8,295

n/m = not meaningful

(1) There were no material intersegment revenues among the segments.

(2) Equity in Corporate Othe r represents equity of the Corporation not allocated to the business segments.