Bank of America 2003 Annual Report Download - page 53

Download and view the complete annual report

Please find page 53 of the 2003 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61

|

|

102 BANK OF AMERICA 2003 BANK OF AMERICA 2003 103

Note 16 Employee Benefit Plans

Pension and Postretirement Plans

The Corporation sponsors noncontributory trusteed qualified pension

plans that cover substantially all officers and employees. The plans

provide defined benefits based on an employee’s compensation, age

and years of service. The Bank of America Pension Plan (the Pension

Plan) provides participants with compensation credits, based on age

and years of service. The Pension Plan allows participants to select

from various earnings measures, which are based on the returns of

certain funds or common stock of the Corporation. The participant-

selected earnings measures determine the earnings rate on the indi-

vidual participant account balances in the Pension Plan. Participants

may elect to modify earnings measure allocations on a daily basis.

The benefits become vested upon completion of five years of service.

It is the policy of the Corporation to fund not less than the minimum

funding amount required by ERISA. During 2004, the Corporation will

contribute at least $87 million to the Pension Plan, the Nonqualified

Pension Plans and the Post Retirement Health and Life Plans.

The Pension Plan has a balance guarantee feature, applied at

the time a benefit payment is made from the plan, that protects par-

ticipant balances transferred and certain compensation credits from

future market downturns. The Corporation is responsible for funding

any shortfall on the guarantee feature.

The Corporation sponsors a number of noncontributory, non-

qualified pension plans. These plans, which are unfunded, provide

defined pension benefits to certain employees.

In addition to retirement pension benefits, full-time, salaried

employees and certain part-time employees may become eligible to

continue participation as retirees in health care and/or life insurance

plans sponsored by the Corporation. Based on the other provisions

of the individual plans, certain retirees may also have the cost of

these benefits partially paid by the Corporation.

Reflected in these results are key changes to the Postretirement

Health and Life Plans and the nonqualified pension plans. In 2002, a

one-time curtailment charge resulted from freezing benefits for

supplemental executive retirement agreements. Additionally, on

December 8, 2003, the President signed the Medicare Prescription

Drug, Improvement and Modernization Act of 2003 (the Act) into law.

The Act introduces a voluntary prescription drug benefit under

Medicare as well as a federal subsidy to sponsors of retiree health

care plans that provide at least an actuarially equivalent benefit. As

permitted by FASB Staff Position (FSP) No. FAS 106-1 “Accounting and

Disclosure Requirements Related to the Medicare Prescription Drug,

Improvement and Modernization Act of 2003” (FSP 106-1), the

Corporation has elected to defer recognizing the effects of the Act on

its Postretirement Health and Life Plans. As a result, any measures of

the accumulated projected benefit obligation (APBO) of the

Postretirement Health and Life Plans or the net periodic postretire-

ment benefit cost in the consolidated financial statements do not

reflect the effects of the Act on the Postretirement Health and Life

Plans. Specific authoritative guidance on the accounting for the fed-

eral subsidy is pending and that guidance, when issued, may or may

not require the Corporation to change previously reported information.

The following table summarizes the changes in fair value of plan

assets, changes in the projected benefit obligation (PBO), the funded

status of both the accumulated benefit obligation (ABO), and the PBO

and the weighted average assumptions used to determine benefit

obligations for the pension plans and postretirement plans for 2003

and 2002. Prepaid and accrued benefit costs are reflected in other

assets, and accrued expenses and other liabilities, respectively, on

the Consolidated Balance Sheet. The discount rate assumption is

based on the internal rate of return for a portfolio of high quality

bonds (Moody’s Aa Corporate bonds) with maturities that are consis-

tent with projected future cash flows. For both the Pension Plan and

the Postretirement Health and Life Plans, the discount rate at

December 31, 2003 was 6.25 percent. For both the Pension Plan and

the Postretirement Health and Life Plans, the expected long-term

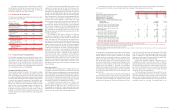

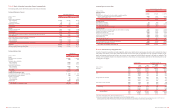

The following table presents the regulatory risk-based capital ratios, actual capital amounts and minimum required capital amounts for the

Corporation, Bank of America, N.A. and Bank of America, N.A. (USA) at December 31, 2003 and 2002:

December 31

2003 2002

Actual Minimum Actual Minimum

(Dollars in millions)

Ratio Amount Required(1) Ratio Amount Required(1)

Tier 1 Capital

Bank of Ame rica Corporation

7.85% $44,050 $22,452 8.22% $43,012 $20,930

Bank of America, N.A.

8.73 42,030 19,247 8.61 40,072 18,622

Bank of America, N.A. (USA)

8.41 3,079 1,465 8.95 2,346 1,049

Total Capital

Bank of Ame rica Corporation

11.87 66,651 44,904 12.43 65,064 41,860

Bank of America, N.A.

11.31 54,408 38,494 11.40 53,091 37,244

Bank of America, N.A. (USA)

12.29 4,502 2,930 11.97 3,137 2,098

Leverage

Bank of Ame rica Corporation

5.73 44,050 30,741 6.29 43,012 27,335

Bank of America, N.A.

6.88 42,030 24,425 7.02 40,072 22,846

Bank of America, N.A. (USA)

9.17 3,079 1,344 9.58 2,346 980

(1) Dollar amount required to meet guidelines for adequately-capitalized institutions.

Note 15 Regulatory Requirements and Restrictions

The Board of Governors of the Federal Reserve System (FRB) requires

the Corporation’s banking subsidiaries to maintain reserve balances

based on a percentage of certain deposits. Average daily reserve bal-

ances required by the FRB were $4.1 billion and $3.7 billion for 2003

and 2002, respectively. Currency and coin residing in branches and

cash vaults (vault cash) are used to partially satisfy the reserve

requirement. The average daily reserve balances, in excess of vault

cash, held with the Federal Reserve Bank amounted to $317 million

and $95 million for 2003 and 2002, respectively.

The primary source of funds for cash distributions by the

Corporation to its shareholders is dividends received from its bank-

ing subsidiaries. Bank of America, N.A. declared and paid dividends

of $8.1 billion for 2003 to its Parent. In 2004, Bank of America, N.A.

can declare and pay dividends to its Parent in an amount not to

exceed 2004 net income. The other subsidiary national banks can

initiate aggregate dividend payments in 2004 of $1.9 billion plus an

additional amount equal to their net profits for 2004, as defined by

statute, up to the date of any such dividend declaration. The amount

of dividends that each subsidiary bank may declare in a calendar year

without approval by the OCC is the subsidiary bank’s net profits for

that year combined with its net retained profits, as defined, for the

preceding two years.

The FRB, the OCC and the Federal Deposit Insurance

Corporation (collectively, the Agencies) have issued regulatory capital

guidelines for U.S. banking organizations. Failure to meet the capital

requirements can initiate certain mandatory and discretionary

actions by regulators that could have a material effect on the

Corporation’s financial statements. At December 31, 2003 and

2002, the Corporation and Bank of America, N.A. were classified as

well-capitalized under this regulatory framework. There have been no

conditions or events since December 31, 2003 that management

believes have changed either the Corporation’s or Bank of America,

N.A.’s capital classifications.

The regulatory capital guidelines measure capital in relation to

the credit and market risks of both on- and off-balance sheet items

using various risk weights. Under the regulatory capital guidelines,

Total Capital consists of three tiers of capital. Tier 1 Capital includes

common shareholders’ equity, Trust Securities, minority interests and

qualifying preferred stock, less goodwill and other adjustments. Tier

2 Capital consists of preferred stock not qualifying as Tier 1 Capital,

mandatory convertible debt, limited amounts of subordinated debt,

other qualifying term debt, the allowance for credit losses up to 1.25

percent of risk-weighted assets and other adjustments. Tier 3 Capital

includes subordinated debt that is unsecured, fully paid, has an orig-

inal maturity of at least two years, is not redeemable before maturity

without prior approval by the FRB and includes a lock-in clause pre-

cluding payment of either interest or principal if the payment would

cause the issuing bank’s risk-based capital ratio to fall or remain

below the required minimum. Tier 3 Capital can only be used to sat-

isfy the Corporation’s market risk capital requirement and may not be

used to support its credit risk requirement. At December 31, 2003

and 2002, the Corporation had no subordinated debt that qualified

as Tier 3 Capital.

The capital treatment of Trust Securities is currently under review

by the FRB due to the issuing trust companies being deconsolidated

under FIN 46. Depending on the capital treatment resolution, Trust

Securities may no longer qualify for Tier 1 Capital treatment, but

instead would qualify for Tier 2 Capital. On July 2, 2003, the FRB

issued a Supervision and Regulation Letter (the Letter) requiring that

bank holding companies continue to follow the current instructions for

reporting Trust Securities in its regulatory reports. Accordingly, the

Corporation will continue to report Trust Securities in Tier 1 Capital

until further notice from the FRB. On September 2, 2003, the FRB and

other regulatory agencies, issued the Interim Final Capital Rule for

Consolidated Asset-backed Commercial Paper Program Assets (the

Interim Rule). The Interim Rule allows companies to exclude from risk-

weighted assets, the newly consolidated assets of asset-backed com-

mercial paper programs required by FIN 46, when calculating Tier 1

and Total Risk-based Capital ratios through March 31, 2004. As of

December 31, 2003, the Corporation consolidated approximately

$4.3 billion of assets from multi-seller asset-backed commercial

paper conduits, in accordance with FIN 46, as originally issued. See

Notes 1 and 9 of the consolidated financial statements for additional

information on FIN 46.

To meet minimum, adequately-capitalized regulatory require-

ments, an institution must maintain a Tier 1 Capital ratio of four

percent and a Total Capital ratio of eight percent. A well-capitalized

institution must generally maintain capital ratios 100 to 200 bps

higher than the minimum guidelines. The risk-based capital rules

have been further supplemented by a leverage ratio, defined as Tier

1 Capital divided by quarterly average total assets, after certain

adjustments. The leverage ratio guidelines establish a minimum of

100 to 200 bps above three percent. Banking organizations must

maintain a leverage capital ratio of at least five percent to be

classified as well-capitalized. As of December 31, 2003, the Corpo-

ration was classified as well-capitalized for regulatory purposes, the

highest classification.

Net unrealized gains (losses) on available-for-sale debt securities,

net unrealized gains on available-for-sale marketable equity securities

and the net unrealized gains (losses) on derivatives included in share-

holders’ equity at December 31, 2003 and 2002 are excluded from the

calculations of Tier 1 Capital, Total Capital and leverage ratios.