Bank of America 2003 Annual Report Download - page 27

Download and view the complete annual report

Please find page 27 of the 2003 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

|

|

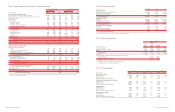

higher bankruptcy filings. General reserves on loans and leases at

December 31, 2003 were $1.2 billion, up $223 million from

December 31, 2002, reflecting the uncertainty around the extent and

depth of the domestic recovery, the impact of rising interest rates on

sectors of the portfolio, the uncertainty in the global arena and con-

tinued exposure to large single name defaults or event risk. The

reserve for unfunded lending commitments decreased $77 million

between December 31, 2003 and December 31, 2002 due to

improvements in the overall commercial credit quality. Given our over-

all assessment of probable losses in the portfolio, the allowance for

credit losses was reduced by $272 million from December 31, 2002.

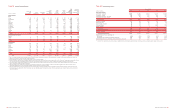

Problem Loan Management

SSI was established in 2001 to better align the management of com-

mercial loan credit workout operations by providing more effective and

efficient management processes afforded by a closely aligned end-to-

end function. We believe that economic returns will be maximized by

assisting distressed companies in refinancing with other lenders or

through the capital markets, facilitating the sale of the entire company

or certain assets/subsidiaries, negotiating traditional restructurings

using company cash flows to repay debts, selling individual assets in

the secondary market when the market prices are attractive relative to

assessed collateral values and by executing collateralized debt obli-

gations or otherwise disposing of assets in bulk. From time to time,

we may contribute or sell certain loans to SSI.

In September 2001, Bank of America, N.A. contributed to SSI

commercial loans with a gross book balance of $3.2 billion in

exchange for a class of preferred and for a class of common stock of

SSI. For financial reporting under GAAP,the loan contribution was

accounted for at carryover book basis as appropriate for entities

under common control, and there was no change in the designation

or measurement of the loans because the individual loan resolution

strategies were not affected by the realignment or contribution. From

time to time, management may identify certain loans to be consid-

ered for accelerated disposition. At that time, such loans or pools of

loans would be redesignated as held for sale and remeasured at the

lower of cost or market.

The loan contribution was effected as an exchange for tax pur-

poses. As is common in workout situations, the loans had a tax basis

higher than their fair market value. Under the Internal Revenue Code

(the Code), SSI received a carryover tax basis in the contributed

loans. In addition, under the Code, the aggregate tax basis of the

class of preferred and the class of common stock received in the

exchange was equal to the basis of the loans contributed. Under the

Code, the preferred stock’s allocated tax basis was equal to its fair

market value and the common stock was allocated the remaining tax

basis, resulting in a tax basis in excess of its fair market value and

book basis. We took into account the tax loss that resulted from the

difference in tax basis and fair market value, recognized on the sale

of this class of common stock to an unrelated third party, as well as

the carryover tax basis in the contributed loans. We believe that

recognition of the tax loss continues to be appropriate.

During 2003 and 2002, Bank of America, N.A. sold commercial

loans with a gross book balance of approximately $3.0 billion

and $2.7 billion, respectively, to SSI. For tax purposes, under the

Code, the sales were treated as a taxable exchange. The tax and

accounting treatment of these sales had no financial statement

impact on us because the sales were transfers among entities under

common control, and there was no change in the individual loan

resolution strategies.

Market Risk Management

Market risk is the potential loss due to adverse changes in the mar-

ket value or yield of a position. This risk is inherent in the financial

instruments associated with our operations and/or activities includ-

ing loans, deposits, securities, short-term borrowings, long-term debt,

trading account assets and liabilities, and derivatives. Market-sensi-

tive assets and liabilities are generated through loans and deposits

associated with our traditional banking business, our customer and

proprietary trading operations, our ALM process, credit risk manage-

ment, and mortgage banking activities.

Our traditional banking loan and deposit products are nontrad-

ing positions and are not reported at market value but instead are

reported at amortized cost for assets or the amount owed for liabili-

ties (historical cost). While the accounting rules require an historical

cost view of traditional banking assets and liabilities, these positions

are still subject to changes in economic value based on varying mar-

ket conditions. Interest rate risk is the effect of changes in the eco-

nomic value of our loans and deposits, as well as our other interest

rate sensitive instruments, and is reflected in the levels of future

income and expense produced by these positions versus levels that

would be generated by current levels of interest rates. We seek to

mitigate interest rate risk as part of the ALM process.

We seek to mitigate trading risk within our prescribed risk

appetite using hedging techniques. Trading positions are reported at

estimated market value with changes reflected in income. Trading

positions are subject to various risk factors, which include exposures

to interest rates and foreign exchange rates, as well as equity, mort-

gage, commodity and issuer risk factors. We seek to mitigate these

risk exposures by utilizing a variety of financial instruments. The fol-

lowing discusses the key risk components along with respective risk

mitigation techniques.

Inte re st Rate Risk

Interest rate risk represents exposures we have to instruments

whose values vary with the level of interest rates. These instruments

include, but are not limited to, loans, deposits, bonds, futures, for-

wards, options and other derivative instruments. We seek to mitigate

risks associated with the exposures in a variety of ways that typically

involve taking offsetting positions in cash or derivative markets. The

cash and derivative instruments allow us to seek to mitigate risks by

reducing the effect of movements in the level of interest rates,

changes in the shape of the yield curve as well as changes in inter-

est rate volatility. Hedging instruments used to mitigate these risks

include related derivatives – options, futures, forwards, swaps, swap-

tions, and caps and floors.

Fo re ign Exc hange Risk

Foreign exchange risk represents exposures we have to changes in

the values of current holdings and future cash flows denominated in

other currencies. The types of instruments exposed to this risk

include investments in foreign subsidiaries, foreign currency-denomi-

nated loans, foreign currency-denominated securities, future cash

flows in foreign currencies arising from foreign exchange transac-

tions, and various foreign exchange derivative instruments whose val-

ues fluctuate with changes in currency exchange rates or foreign

interest rates. Instruments used to mitigate this risk are foreign

exchange options, futures, forwards and deposits. These instruments

help insulate us against losses that may arise due to volatile move-

ments in foreign exchange rates or interest rates.

Mortgage Risk

Our exposure to mortgage risk takes several forms. First, we trade and

engage in market-making activities in a variety of mortgage securities,

including whole loans, pass-through certificates, commercial mort-

gages, and collateralized mortgage obligations. Second, we originate

a variety of asset-backed securities, which involves the accumulation

of mortgage-related loans in anticipation of eventual securitization.

Third, we may hold positions in mortgage securities and residential

mortgage loans as part of the ALM portfolio. These activities generate

market risk since these instruments are sensitive to changes in the

level of market interest rates, changes in mortgage prepayments and

interest rate volatility. Options, futures, forwards, swaps, swaptions

and U.S. Treasury securities are used to hedge mortgage risk by seek-

ing to mitigate the effects of changes in interest rates.

Equity Marke t Risk

Equity market risk arises from exposure to securities that represent

an ownership interest in a corporation in the form of common stock or

other equity-linked instruments. The instruments held that would lead

to this exposure include, but are not limited to, the following: common

stock, listed equity options (puts and calls), over-the-counter equity

options, equity total return swaps, equity index futures and convertible

bonds. We seek to mitigate the risk associated with these securities

via portfolio hedging that focuses on reducing volatility from changes

in stock prices. Instruments used for risk mitigation include options,

futures, swaps, convertible bonds and cash positions.

Commodity Risk

Commodity risk represents exposures we have to products traded in

the petroleum, natural gas and power markets. Our principal exposure

to these markets emanates from customer-driven transactions. These

transactions consist primarily of futures, forwards, swaps and options.

We seek to mitigate exposure to the commodity markets with instru-

ments including, but not limited to, options, futures and swaps in the

same or similar commodity product, as well as cash positions.

Issue r Risk

Our trading portfolio is exposed to issuer risk where the value of a

trading account asset may be adversely impacted for various reasons

directly related to the issuer, such as management performance,

financial leverage or reduced demand for the issuer’s goods or serv-

ices. Perceived changes in the creditworthiness of a particular debtor

or sector can have significant effects on the replacement costs of

both cash and derivative positions. We seek to mitigate the impact of

credit spreads, credit migration and default risks on the market value

of the trading portfolio with the use of credit default swaps, and credit

fixed income and similar securities.

Trading Risk Management

Trading-related revenues represent the amount earned from our trad-

ing positions, which include trading account assets and liabilities,

derivative positions and mortgage banking assets. Trading positions

are taken in a diverse range of financial instruments and markets,

and are reported at fair value. For more information on fair value, see

Complex Accounting Estimates and Principles on page 30. Trading

account profits can be volatile and are largely driven by general mar-

ket conditions and customer demand. Trading account profits are

dependent on the volume and type of transactions, the level of risk

assumed, and the volatility of price and rate movements at any given

time within the ever-changing market environment.

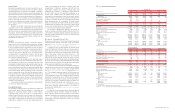

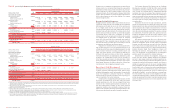

The histogram of daily revenue or loss below is a simple graphic

depicting trading volatility and tracking success of trading-related rev-

enue for 2003. Trading-related revenue encompasses both propri-

etary trading and customer-related activities. In 2003, positive

trading-related revenue was recorded for 88 percent of trading days.

Furthermore, only four percent of the total trading days had losses

greater than $10 million, and the largest loss was $41 million. This

can be compared to 2002 and 2001 as follows:

■

In 2002, positive trading-related revenue was recorded for 86

percent of trading days and only five percent of the total trad-

ing days had losses greater than $10 million. The largest loss

realized in 2002 was $32 million.

■

In 2001, positive trading-related revenue was recorded for 88

percent of trading days and only four percent of the total trad-

ing days had losses greater than $10 million. The largest loss

realized in 2001 was $58 million.

50 BANK OF AMERICA 2003 BANK OF AMERICA 2003 51

Revenue

Number of Days

(Dollars in millions)

Histogram of Daily Trading-related Revenue

Twelve Months Ended December 31, 2003

<-50 -50 > < -40 -40 > < -30 -30 > < -20 -20 > < -10 -10 > < 0 0 > < 10 10 > < 20 20 > < 30 30 > < 40 40 > < 50 > 50

0

30

60

80

70

50

40

20

10