Bank of America 2003 Annual Report Download - page 25

Download and view the complete annual report

Please find page 25 of the 2003 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

|

|

Foreign Portfolio

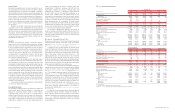

Table 12 sets forth total foreign exposure broken out by region at

December 31, 2003 and 2002. Total foreign exposure is defined to

include credit exposure plus securities and other investments for all

exposure with a country of risk other than the United States.

Table 12

Regional Foreign Exposure and Selected

Emerging Markets Exposure(1,2)

December 31

(Dollars in millions)

2003 2002

Regional Foreign Exposure

Asia

$13,605 $13,912

Europe

49,532 43,034

Africa

108 80

Middle East

584 435

Latin America

4,974 3,915

Other(3)

9,998 8,709

Total

$78,801 $70,085

Selected Emerging Markets(4)

Asia

$11,012 $10,296

Central and Eastern Europe

270 364

Latin America

4,974 3,915

Total

$16,256 $14,575

(1) The balances above do not reflect the netting of local funding or liabilities against local

exposures as allowed by the Federal Financial Institutions Examinations Council (FFIEC).

(2) Exposures for Asia and Latin America have been reduced by $12 and $173, respectively,

at December 31, 2003, and $12 and $763, respectively, at December 31, 2002. Such amounts

represent the fair value of U.S. Treasury securities held as collateral outside the country of

exposure.

(3) Other includes Australia, Bermuda, Canada, Cayman Islands, New Zealand and supranational

entities.

(4) There is no generally accepted definition of emerging markets. The definition that we used

included all countries in Asia excluding Japan; all countries in Latin America excluding Cayman

Islands and Bermuda; and all countries in Central and Eastern Europe except Greece.

Our total foreign exposure was $78.8 billion at December 31, 2003,

an increase of $8.7 billion from December 31, 2002. Our foreign

exposure was concentrated in Europe, which accounted for $49.5 bil-

lion, or 63 percent, of total foreign exposure. Growth in exposure in

Europe during 2003 took place in Western Europe and was distrib-

uted across a variety of industries with the largest concentration in

the banking sector that accounted for approximately 63 percent of

the growth. At December 31, 2003 and 2002, the United Kingdom

and Germany were the only countries whose total cross-border out-

standings exceeded 0.75 percent of our total assets. The United

Kingdom had total cross-border exposure of $10.1 billion and $9.4

billion, respectively, representing 1.37 percent and 1.42 percent of

total assets, respectively. At December 31, 2003 and 2002, Germany

had total cross-border exposure of $6.9 billion and $5.8 billion,

respectively, representing 0.93 percent and 0.87 percent of total

assets, respectively. The bulk of the exposure to both of these coun-

tries was concentrated in the banking sector.

At December 31, 2003, foreign exposure to entities in countries

defined as emerging markets increased 12 percent to $16.3 billion,

or 21 percent of total foreign exposure, compared to $14.6 billion or

21 percent of total exposure at the end of 2002. At December 31,

2003, 68 percent of the emerging markets exposure was in Asia

compared to 71 percent at December 31, 2002. Growth in Asian

emerging markets was largely concentrated in South Korea due to

increases in short-term trade financing. India also contributed to

growth in Asian emerging markets with increases in acceptances and

trading of Indian government securities. A decline in Singapore due

to a decrease in client activity partially offset this growth.

Growth in Latin America was attributable to the acquisition of

24.9 percent of the Mexican entity GFSS in the first quarter of 2003

for $1.6 billion. This growth was partially offset by a reduction in

Mexican Brady Bonds that were called during the second quarter of

2003 as well as reductions in loans and trading activity in Brazil and

continued reductions of our exposure in Argentina. Mexico is the only

country in the region where we significantly increased our exposure.

We will continue to participate in trading activities to take advantage

of favorable market conditions.

The primary components of our exposure in Brazil at December 31,

2003 and 2002 were $406 million and $562 million, respectively, of tra-

ditional credit exposure (loans, letters of credit, etc.) and $159 million

and $290 million, respectively, of Brazilian government securities.

Derivatives exposure totaled $7 million at December 31, 2003 com-

pared to $55 million at December 31, 2002. At December 31, 2003

and 2002, the allowance for credit losses related to Brazil consisted of

$76 million and $60 million, respectively, related to traditional credit

exposure. Nonperforming loans in Brazil were $39 million at December

31, 2003 compared to $90 million at December 31, 2002. Net charge-

offs in 2003 totaled $33 million compared to $8 million in 2002.

The primary components of our exposure in Argentina at

December 31, 2003 and 2002, were $144 million and $339 million,

respectively, of traditional credit exposure, and $65 million and $62

million, respectively, of Argentine government securities. Derivatives

exposure totaled $2 million at both December 31, 2003 and 2002.

The allowance for credit losses related to Argentina’s traditional

credit exposure was $104 million and $177 million at December 31,

2003 and 2002, respectively. At December 31, 2003 and 2002,

Argentina nonperforming loans were $107 million and $278 million,

respectively. Net charge-offs in 2003 totaled $82 million compared to

$113 million in 2002.

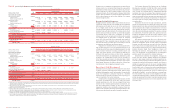

Credit Quality Performance

Overall credit quality continued to improve in 2003 as all major com-

mercial asset quality indicators showed positive trends while con-

sumer credit quality performance remained stable. In 2003,

commercial criticized exposure declined $8.7 billion to $12.7 billion,

as presented in Table 13. Decreases in criticized exposure resulted

from overall improvement in credit quality, paydowns and payoffs that

resulted largely from increased refinancings in the capital markets,

reduced levels of inflows, loan sales and charge-offs. Most of the

decrease in 2003 was in our large corporate portfolio, which was

down $7.0 billion for the year. Reductions were concentrated in the

commercial – domestic product in the utilities, telecommunications

services, media and chemicals industries.

We routinely review the loan and lease portfolio to determine if

any credit exposure should be placed on nonperforming status. An

asset is placed on nonperforming status when it is determined that

principal and interest are not expected to be fully collected in accor-

dance with its contractual terms. As evidenced by the improvement

in credit quality, nonperforming assets, presented in Table 14,

declined $2.2 billion from December 31, 2002 due to decreases in

the nonperforming commercial loan category. Decreases in total non-

performing commercial loans were due to reduced levels of inflows of

$2.8 billion, loan sales of $1.5 billion, paydowns and payoffs of $1.3

billion that resulted from increased refinancings in the capital markets,

improvements in the credit quality of individual exposures and

charge-offs. There are no assurances that the elevated levels of pay-

downs and payoffs experienced in 2003 will continue in 2004. Eighty-

four percent of the reduction in nonperforming commercial loans was

in our large corporate portfolio. Nonperforming commercial – domestic

loans decreased by $1.3 billion and represented 1.56 percent of

commercial – domestic loans at December 31, 2003 compared to

2.65 percent at December 31, 2002. Nonperforming commercial –

foreign loans decreased $773 million and represented 3.83 percent

of commercial – foreign loans at December 31, 2003 compared to

6.83 percent at December 31, 2002.

Within the consumer portfolio, nonperforming loans decreased

$95 million to $638 million, and represented 0.27 percent of con-

sumer loans at December 31, 2003 compared to $733 million, rep-

resenting 0.37 percent of consumer loans at December 31, 2002.

The decrease in nonperforming consumer loans was driven by loan

sales, while the improvement in the percentage of nonperforming

consumer loans to the total consumer portfolio was due to growth in

residential mortgages stemming from our ALM strategies to capitalize

on the large increase of refinancings in the market.

Sales of nonperforming assets in 2003 totaled $1.7 billion,

comprised of $1.5 billion of nonperforming commercial loans, $141

million of nonperforming consumer loans and $123 million of fore-

closed properties. Sales of nonperforming assets in 2002 totaled

$543 million, comprised of $296 million of nonperforming commer-

cial loans, $105 million of nonperforming consumer loans and $142

million of foreclosed properties.

Table 13

Commercial Criticized Exposure(1)

December 31

2003 2002

(Dollars in millions)

Amount Percent(2) Amount Percent(2)

Commercial – domestic

$8,847 6.08% $16,401 10.78%

Commercial – foreign

2,820 6.71 3,804 8.93

Commercial real estate

– domestic

956 3.83 1,150 4.62

Commercial real estate

– foreign

27 8.40 20.79

Total commercial

criticized exposure

$12,650 5.94% $21,357 9.71%

(1) Criticized exposure corresponds to the Special Mention, Substandard and Doubtful asset cate-

gories defined by regulatory authorities. Exposure amounts include loans and leases, foreclosed

properties, letters of credit, bankers’ acceptances, derivatives and assets held for sale.

(2) Commercial criticized exposure is taken as a percentage of total utilized exposure which

includes loans and leases, foreclosed properties, letters of credit, bankers’ acceptances, deriva-

tives and assets held for sale.

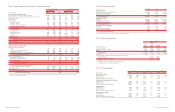

Table 14

Nonperforming Assets(1)

December 31

(Dollars in millions)

2003 2002

Commercial – domestic

$1,507 $2,781

Commercial – foreign

586 1,359

Commercial real estate – domestic

140 161

Commercial real estate – foreign

23

Total commercial

2,235 4,304

Residential mortgage

531 612

Home equity lines

43 66

Direct/Indirect consumer

28 30

Consumer finance

32 19

Foreign consumer

46

Total consumer

638 733

Total nonperforming loans

2,873 5,037

Foreclosed properties

148 225

Total nonperforming assets(2)

$3,021 $5,262

(1) In 2003, $575 in interest income was contractually due on nonperforming loans and troubled

debt restructured loans. Of this amount, $141 was actually recorded as interest income in 2003.

(2) Balances do not include $202 and $120 of nonperforming assets included in other assets

at December 31, 2003 and 2002, respectively.

Table 15 presents the additions to and reductions in nonperform-

ing assets in the commercial and consumer portfolios during 2003

and 2002.

Table 15

Nonperforming Assets Activity

(Dollars in millions)

2003 2002

Nonperforming assets, January 1

$5,262 $4,908

Commercial

Additions to nonperforming assets:

New nonaccrual loans and

foreclosed properties

2,134 4,963

Advances on loans

199

244

Total commercial additions

2,333

5,207

Reductions in nonperforming assets:

Paydowns, payoffs and sales

(2,804) (2,171)

Returns to performing status

(197) (149)

Charge-offs(1)

(1,352) (2,354)

Transfers to assets held for sale

(108) –

Total commercial reductions

(4,461) (4,674)

Total commercial net additions to

(reductions in) nonperforming assets

(2,128) 533

Consumer

Additions to nonperforming assets:

New nonaccrual loans and

foreclosed properties

1,583 1,694

Transfers from assets held for sale(2)

5

77

Total consumer additions

1,588 1,771

Reductions in nonperforming assets:

Paydowns, payoffs and sales

(712) (957)

Returns to performing status

(878) (886)

Charge-offs(1)

(111) (107)

Total consumer reductions

(1,701) (1,950)

Total consumer net reductions in

nonperforming assets

(113) (179)

Total net additions to (reductions in)

nonperforming assets

(2,241) 354

Nonperforming assets, December 31

$3,021 $5,262

(1) Certain loan products, including commercial credit card, consumer credit card and consumer

non-real estate loans, are not classified as nonperforming; therefore, the charge-offs on these

loans are not included above.

(2) Includes assets held for sale that were foreclosed and transferred to foreclosed properties.

Domestic commercial loans past due 90 days or more and still accru-

ing interest were $133 million and $223 million at December 31,

2003 and 2002, respectively. Consumer loans past due 90 days or

more and still accruing interest were $698 million and $541 million

at December 31, 2003 and 2002, respectively, which included held

credit card loans of $616 million and $424 million, respectively.

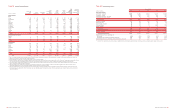

Commercial – domestic loan net charge-offs, as presented in

Table 17, decreased $714 million to $757 million in 2003 compared

to 2002, reflecting overall improvement in the portfolio and to a

lesser extent, reductions in various industry sectors, the largest of

which was telecommunications services.

Commercial – foreign loan net charge-offs were $306 million in

2003 compared to $521 million in 2002. The decrease was attributable

to reductions in exposure to the telecommunications and media industry

sectors. The largest concentration of commercial – foreign loan net

charge-offs in 2003, excluding Parmalat, was attributable to Argentina.

Held credit card net charge-offs increased $420 million to $1.5

billion in 2003 compared to 2002, of which $173 million were from

new advances on previously securitized balances. Such advances are

46 BANK OF AMERICA 2003 BANK OF AMERICA 2003 47