Bank of America 2003 Annual Report Download - page 19

Download and view the complete annual report

Please find page 19 of the 2003 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

|

|

Consumer and Commercial Banking

Our Consume r and Comme rcial Banking strategy is to attract, retain

and deepen customer relationships. A critical component of that

strategy includes continuously improving customer satisfaction. We

believe this focus will help us achieve our goal of being recognized as

the best retail bank in America. Customer satisfaction increased

eight percent at December 31, 2003 compared to December 31,

2002. We added 1.24 million net new checking accounts in 2003,

exceeding the full-year goal of one million and more than doubling

last year’s total net new checking account growth of 528,000. This

growth resulted from the introduction of new products, advancement

of our multicultural strategy and strong customer retention. In 2004,

we anticipate checking account growth to exceed 2003 levels. Access

to our services through online banking, which saw a 52 percent

increase in active online subscribers, our network of domestic bank-

ing centers, card products, ATMs, telephone and Internet channels,

and our product innovations, such as an expedited mortgage appli-

cation process, all contributed to success with our customers.

The major subsegments of Consume r and Comme rcial Banking

are Banking Re gions, Consume r Products and Comme rcial Banking.

Banking Re gions serves consumer households and small busi-

nesses in 21 states and the District of Columbia through its network

of 4,277 banking centers, 13,241 ATMs, telephone and Internet

channels on www.bankofamerica.com. Banking Re gions provides a

wide range of products and services, including deposit products such

as checking accounts, money market savings accounts, time

deposits and IRAs, debit card products and credit products such as

home equity, mortgage and personal auto loans. It also provides

treasury management, credit services, community investment, e-com-

merce and brokerage services to nearly two million small business

relationships across the franchise. Banking Re gions also includes

Pre mie r Banking,which provides high-touch banking, which repre-

sents more direct contact with the client, and investment solutions to

affluent clients with balances up to $3 million.

Consume r Products provides services including the origination,

fulfillment and servicing of residential mortgage loans, issuance and

servicing of credit cards, direct banking via telephone and Internet,

student lending and certain insurance services. Consume r Products

also provides retail finance and floorplan programs to marine, RV and

auto dealerships.

Comme rcial Banking provides commercial lending and treasury

management services primarily to middle-market companies with

annual revenue between $10 million and $500 million. These services

are available through relationship manager teams as well as through

alternative channels such as the telephone via the commercial serv-

ice center and the Internet by accessing Bank of America Direct.

Comme rcial Banking also includes the Real Estate Banking Group,

which provides project financing and treasury management to private

developers, homebuilders and commercial real estate firms across

the U.S. Comme rcial Banking also provides lending and investing serv-

ices to develop low- and moderate-income communities.

Consume r and Comme rcial Banking drove our financial results in

2003 as total revenue increased $2.7 billion, or 11 percent. Net

income rose $1.0 billion, or 15 percent. The increase in net income

and a decrease in the capital charge resulting from the reduction in

the rate used to calculate the charge for the use of capital drove a

$1.1 billion, or 24 percent, increase in SVA.

Net interest income increased $765 million due to overall

deposit and loan portfolio growth. This increase was offset by the

compression of deposit interest margins and the net results of ALM

activities. Net interest income was positively impacted by the $6.2

billion, or three percent, increase in average loans and leases in

2003, compared to 2002, resulting from a $6.3 billion, or six per-

cent, increase in consumer loans. An eight percent increase in aver-

age direct/indirect loans contributed to the growth in the consumer

loan portfolio. Average commercial loans remained relatively

unchanged in 2003.

Deposit growth also positively impacted net interest income.

Higher consumer deposit balances as a result of government tax

cuts, higher customer retention and our efforts to add new cus-

tomers, as evidenced by the increase in net new checking accounts,

drove the $29.3 billion, or 10 percent, increase in average deposits

in 2003.

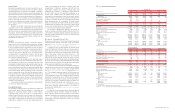

Significant Noninterest Income Components

(Dollars in millions)

2003 2002

Service charges $4,353 $4,069

Mortgage banking income 1,922 761

Card income 3,052 2,620

Trading account profits (losses)

(169) (7)

Increases in both consumer and corporate service charges led to the

$284 million, or seven percent, increase in service charge income.

Consumer service charges increased $247 million, or eight percent,

to $3.2 billion due to favorable repricing and increased levels of

deposit fees from new account growth of $254 million. Corporate

service charges increased $37 million, or three percent, to $1.2 billion

due to a $31 million increase in income from pricing initiatives and

account growth.

Decreasing mortgage interest rates in the first half of 2003

drove a sharp increase in refinance volumes within the mortgage

industry leading to increases in our loan production and sales

activity. First mortgage loan originations increased $43.1 billion to

$131.1 billion in 2003, resulting from elevated refinancing levels

and broader market coverage from our ongoing deployment of

LoanSolutions

®

,which was first rolled out in the second quarter

of 2002. Total mortgages funded through LoanSolutions

®

totaled

$36.3 billion and $7.3 billion in 2003 and 2002, respectively. First

mortgage loan origination volume was composed of approximately

$91.8 billion of retail loans and $39.3 billion of wholesale loans in

2003, compared to $59.9 billion and $28.1 billion, respectively, in

2002. Increased mortgage prepayments, resulting from the

extended low interest rate environment of 2003, led to a $32.6 bil-

lion net decline in the average portfolio of first mortgage loans

serviced to $250.4 billion in 2003. Increased sales of loans to the

secondary market in 2003, along with improved profit margins

drove the $1.2 billion increase in mortgage banking income. In

2003 and 2002, loan sales to the secondary market were $107.4

billion and $51.6 billion, respectively.

As we have seen interest rates rise from mid-year levels, the

warehouse and pipeline of mortgage loan applications at December

31, 2003 were approximately 70 percent lower compared to June 30,

2003 levels. At current or increased mortgage interest rate levels,

the mortgage industry would be expected to experience a significant

decline in first mortgage origination volume. We are not in a position

to determine the ultimate impact to the mortgage banking industry or

our related business at this time. As industry origination volumes

decline, we believe we can garner market share from increased dis-

tribution, increased advertising and sales productivity; however, we

do expect the decline in industry volumes to negatively impact mort-

gage banking income in 2004 compared to 2003. We also believe

our increased focus on home equity lending will replace a portion of

the drop in mortgage revenue with higher net interest income.

Trading account profits (losses) primarily represent the net

mark-to-market adjustments on mortgage banking assets and related

derivative instruments used as an economic hedge on the assets.

Impacting trading account profits (losses) in 2003 was a net reduc-

tion, including the negative impact of changes in prepayment speeds,

in the value of our mortgage banking assets and related derivative

instruments of $159 million, due to a difference between the change

in the value of our mortgage banking assets and the related deriva-

tives. The value of mortgage banking assets increased to $2.7 billion

at December 31, 2003 compared to $2.1 billion at December 31,

2002 due to new additions from loan sales, offset by normal pay-

downs, amortization and negative mark-to-market adjustments.

Increases in both debit and credit card income resulted in the

16 percent increase in card income. The increase in debit card

income of $111 million, or 14 percent, to $896 million was due to

increases in purchase volumes related to account growth and higher

activation and penetration levels. Credit card income increased $321

million, or 18 percent, resulting from higher interchange fees of $154

million, driven by increased credit card purchase volumes, late fees

of $113 million, overlimit fees of $86 million, cash advance fees of

$43 million and other miscellaneous fees of $95 million offset by

lower excess servicing income of $170 million. Debit card purchase

volumes grew 22 percent while credit card purchases increased 13

percent in 2003 from 2002. Currently, management anticipates that

credit and debit card purchase volumes will continue to increase in

2004. Card income included activity from the securitized portfolio of

$116 million and $157 million in 2003 and 2002, respectively.

Noninterest income, rather than net interest income and provision for

credit losses, is recorded for assets that have been securitized as we

are compensated for servicing the securitized assets and record

servicing income and gains or losses on securitizations, where appro-

priate. New advances on previously securitized accounts will be

recorded on our balance sheet after the revolving period of the secu-

ritization, which has the effect of increasing loans on our balance

sheet and increasing net interest income and charge-offs, with a cor-

responding reduction in noninterest income. Average on-balance

sheet credit card outstandings increased 32 percent, due to over

4 million new accounts and an increase of $2.6 billion in new

advances on previously securitized balances that are recorded on our

balance sheet after the revolving period of the securitization. Average

managed credit card outstandings, which include securitized credit

card loans, increased 15 percent in 2003 due to new account growth

from direct marketing programs and the branch network.

On January 23, 2004, the Federal District Court in the Eastern

District of New York approved Visa U.S.A.’s previously entered into

agreement in principle to settle the class action anti-trust lawsuit filed

against it by Wal-Mart and other retailers (the settlement). Effective

January 1, 2004, the settlement permitted retailers who accept Visa

U.S.A. cards to reject payment from consumers signing for purchases

using their debit card, changing Visa U.S.A.’s longstanding “honor all

cards” policy. In addition, beginning August 1, 2003, interchange fees

charged to retailers were reduced by approximately 30 percent. This

reduction was effective until January 1, 2004, at which time Visa U.S.A.

was free to set competitive rates. The after-tax impact of the reduction

in interchange fees on net income in 2003 was $52 million. While it is

difficult to predict volume and interchange fees, we believe that, on an

after-tax basis, the impact of the reduction in interchange fees will likely

reduce net income by approximately $90 million in 2004.

An increase in provision in the held consumer credit card loan

portfolio of $613 million and declines in provision for other consumer

loans of $239 million and commercial loans of $140 million resulted

in a $256 million, or 14 percent, increase in the provision for credit

losses. The increase in held consumer credit card provision to $1.8

billion was due to increases of $192 million related to higher out-

standings, $173 million from charge-offs of new advances on previ-

ously securitized balances, and $255 million from charge-offs related

to continued seasoning of outstandings from new account growth and

economic conditions, including higher bankruptcies. Seasoning refers

to the length of time passed since an account was opened.

Noninterest expense increased $1.0 billion, or nine percent,

due to increases in data processing costs of $305 million, personnel

expense of $291 million, other general operating expenses of $142

million, marketing and promotional fees of $112 million and occu-

pancy expense of $92 million. Personnel expense increased as a

result of higher incentive compensation of $178 million driven by

increased mortgage sales production. Marketing and promotional

fees were up due to increased advertising and marketing investments

of $105 million in direct marketing for the credit card business.

Asset Management

Asse t Manage me nt provides wealth and investment management

services through three businesses: The Private Bank, which focuses

on high-net-worth individuals and families; Banc of America

Investments (BAI), providing investment and financial planning serv-

ices to individuals; and Banc of America Capital Management

(BACAP), the asset management group serving the needs of institu-

tional clients, high-net-worth individuals and retail customers.

Together, these businesses are focusing on attracting and deepening

client relationships, with the ultimate goal of becoming America’s

advisor of choice. Our strategy is threefold: (i) to continue to expand

distribution capabilities to reach key constituencies and markets; (ii)

to complete the expansion and rollout of integrated wealth manage-

ment models to better serve our clients’ financial needs; and (iii) to

continue to strengthen and develop our full array of investment man-

agement products and services for individuals and institutions. Asse t

Manage me nt exceeded its goal of increasing financial advisors by 20

percent and ended the year with 1,150 financial advisors. In addition,

the Premier Banking and Investments partnership has developed an

integrated financial services model and as a component of the

continued strategic distribution channel expansion opened 10 new

wealth centers. The Private Bank successfully completed the rollout

of its high-net-worth model to all markets. BACAP has experienced

growth in assets under management led by higher market valuations,

sales in assets advised by Marsico and sales in the fee-based assets

of BACAP’s Consulting Services Group.

34 BANK OF AMERICA 2003 BANK OF AMERICA 2003 35