Bank of America 2003 Annual Report Download - page 22

Download and view the complete annual report

Please find page 22 of the 2003 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

|

|

Liquidity Risk Management

Liquidity Risk

Liquidity is the ongoing ability to accommodate liability maturities and

deposit withdrawals, fund asset growth and meet contractual obliga-

tions through unconstrained access to funding at reasonable market

rates. Liquidity management involves maintaining ample and diverse

funding capacity, liquid assets and other sources of cash to accom-

modate fluctuations in asset and liability levels due to changes in our

business operations or unanticipated events.

We manage liquidity at two primary levels. The first level is the

liquidity of the parent company, which is the holding company that

owns the banking and nonbanking subsidiaries. The second level is

the liquidity of the banking subsidiaries. The management of liquidity

at both levels is essential because the parent company and banking

subsidiaries each have different funding needs and sources, and each

are subject to certain regulatory guidelines and requirements.

Through its subcommittee ALCO, the Finance Committee is responsi-

ble for establishing our liquidity policy as well as approving operating

and contingency procedures and monitoring liquidity on an ongoing

basis. Corporate Treasury is responsible for planning and executing

our funding activities and strategy.

A primary objective of liquidity risk management is to provide a

planning mechanism for unanticipated changes in the demand or need

of liquidity created by customer behavior or capital market conditions.

In order to achieve this objective, liquidity management and business

unit activities are managed consistent with a strategy of funding sta-

bility, flexibility and diversity. We emphasize maximizing and preserving

customer deposits and other customer-based funding sources.

Deposit rates and levels are monitored, and trends and significant

changes are reported to the Finance Committee. Deposit marketing

strategies are reviewed for consistency with our liquidity policy objec-

tives. Asset securitizations also enhance funding diversity and stability

and are considered an additional source of contingency funding.

We develop and maintain contingency funding plans that sepa-

rately address the parent company and banking subsidiaries’ liquidity.

These plans evaluate market-based funding capacity under various

levels of market conditions and specify actions and procedures to be

implemented under liquidity stress. Further, these plans address

alternative sources of liquidity, measure the overall ability to fund our

operations, and define roles and responsibilities for effectively man-

aging liquidity through a problem period.

Our borrowing costs and ability to raise funds are directly

impacted by our credit ratings and changes thereto. The credit ratings

of Bank of America Corporation and Bank of America, National

Association (Bank of America, N.A.) are reflected in the table below.

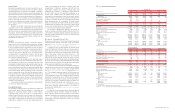

Table 5

Credit Ratings

December 31, 2003

Bank of America Corporation Bank of America, N.A.

Senior Subordinated Commercial Short- Long-

Debt Debt Paper term term

Moody’s

Aa2 Aa3 P-1 P-1 Aa1

S&P

A+ A A-1 A-1+ AA-

Fitch, Inc. AA AA- F1+ F1+ AA+

Primary sources of funding for the parent company include dividends

received from its banking and nonbanking subsidiaries and proceeds

from the issuance of senior and subordinated debt, commercial

paper and equity. Primary uses of funds for the parent company

include repayment of maturing debt and commercial paper, share

repurchases, dividends paid to shareholders, and subsidiary funding

through capital or debt.

Parent company liquidity is maintained at levels sufficient to fund

holding company and nonbank affiliate operations during various stress

scenarios in which access to normal funding sources is disrupted. The

primary measure used in assessing the parent company’s liquidity is

“Time to Required Funding” in a stress environment. This measure

assumes that the parent company is unable to generate funds from

debt or equity issuance, receives no dividend income from subsidiaries,

and no longer pays dividends to shareholders. Projected liquidity

demands are met with available liquidity until the liquidity is exhausted.

Under this scenario, the amount of time which elapses before the cur-

rent liquid assets are exhausted is considered the “Time to Required

Funding”. ALCO approves the target range set for this metric and mon-

itors adherence to the target. In order to remain in the target range, we

use the “Time to Required Funding” measurement to determine the

timing and extent of future debt issuances and other actions.

Primary sources of funding for the banking subsidiaries include

customer deposits, wholesale funding and asset securitizations,

sales and repurchase obligations. Primary uses of funds for the bank-

ing subsidiaries include repayment of maturing obligations and

growth in the ALM and core asset portfolios, including loan demand.

ALCO regularly reviews the funding plan for the banking sub-

sidiaries and focuses on maintaining prudent levels of wholesale bor-

rowing. Also for the banking subsidiaries, expected wholesale

borrowing capacity over a 12-month horizon compared to current out-

standings is evaluated using a variety of business environments.

These environments have differing earnings performance, customer

relationship and ratings scenarios. Funding exposure related to our

role as liquidity provider to certain off-balance sheet financing entities

is also measured under a stress scenario. In this measurement, rat-

ings are downgraded such that the off-balance sheet financing enti-

ties are not able to issue commercial paper and backup facilities that

we provide are drawn upon. In addition, potential draws on credit facil-

ities to issuers with ratings below a certain level are analyzed to

assess potential funding exposure.

Our primary business activities allow us to obtain funds from

our customers in many ways and require us to provide funds to our

customers in many different forms. A key element of our success is

the ability to balance the cash provided from our deposit base and

the capital markets against cash used in our activities.

One ratio used to monitor trends is the “loan to domestic

deposit” (LTD) ratio. The LTD ratio reflects the percent of loans that

could be funded by domestic deposits. A ratio below 100 percent

would indicate that market-based funding would not be needed to

fund new loans; conversely, a ratio above 100 percent would indicate

that market-based funds would be needed to fund new loans. The

ratio was 98 percent for 2003 compared to 97 percent for 2002. For

further discussion see Deposit and Other Funding Sources below.

We originate loans both for retention on our balance sheet and

for distribution. As part of our “originate to distribute” strategy, com-

mercial loan originations are distributed through syndication struc-

tures, and residential mortgages originated by the mortgage group

are frequently distributed in the secondary market. In connection with

our balance sheet management activities, we may retain mortgage

loans originated as well as purchase and sell loans based on our

assessment of market conditions.

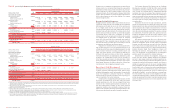

Table 6

Average Balance Sheet

(Dollars in millions)

2003 2002

Assets

Time deposits placed and other short-term

investments

$9,056 $10,038

Federal funds sold and securities purchased

under agreements to resell

78,857 45,640

Trading account assets

97,222 79,562

Debt securities

72,267 75,298

Loans and leases

356,148 336,819

Other assets

150,582 115,586

Total assets

$764,132 $662,943

Liabilities and shareholders’ equity

Domestic interest-bearing deposits

$251,307 $225,464

Foreign interest-bearing deposits

35,204 36,549

Short-term borrowings

147,580 104,153

Trading account liabilities

37,176 31,600

Long-term debt(1)

68,432 66,045

Noninterest-bearing deposits

119,722 109,466

Other liabilities

55,507 42,053

Shareholders’ equity

49,204 47,613

Total liabilities and shareholders’ equity

$764,132 $662,943

(1) Includes long-term debt related to Trust Securities.

Deposits and Other Funding Sources

Deposits are a key source of funding. Table

I

beginning on page 58

provides information on the average amounts of deposits and the

rates paid by deposit category. Average deposits increased $34.8 bil-

lion to $406.2 billion in 2003 compared to 2002 due to a $25.8 bil-

lion increase in average domestic interest-bearing deposits and a

$10.3 billion increase in average noninterest-bearing deposits, par-

tially offset by a $1.3 billion decrease in average foreign interest-

bearing deposits. We typically categorize our deposits into either core

or market-based deposits. Core deposits, which are generally cus-

tomer-based, are an important stable, low-cost funding source and

typically react more slowly to interest rate changes than market-

based deposits. Core deposits exclude negotiable CDs, public funds,

other domestic time deposits and foreign interest-bearing deposits.

Average core deposits increased $32.7 billion to $363.4 billion, a

10 percent increase from a year ago. The increase was due to the

growth in money market deposits of $17.1 billion, noninterest-bear-

ing deposits of $10.3 billion, savings of $2.8 billion, and consumer

CDs and IRAs of $2.6 billion due to an emphasis on total relationship

balances and customer preference for stable investments in uncer-

tain economic times. Market-based deposit funding increased

$2.0 billion to $42.8 billion in 2003. The increase was due to a $3.4

billion increase in negotiable CDs, public funds and other domestic

time deposits that was offset by a $1.3 billion decrease in foreign

interest-bearing deposits. Deposits, on average, represented 53

percent and 56 percent of total sources of funds during 2003 and

2002, respectively.

Table 7 summarizes average deposits by category.

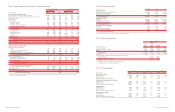

Table 7

Average Deposits

(Dollars in millions)

2003 2002

Deposits by type

Domestic interest-bearing:

Savings

$24,538 $21,691

NOW and money market accounts

148,896 131,841

Consumer CDs and IRAs

70,246 67,695

Negotiable CDs and

other time deposits

7,627 4,237

Total domestic interest-bearing

251,307 225,464

Foreign interest-bearing:

Banks located in foreign countries

13,959 15,464

Governments and official institutions

2,218 2,316

Time, savings and other

19,027 18,769

Total foreign interest-bearing

35,204 36,549

Total interest-bearing

286,511 262,013

Noninterest-bearing

119,722 109,466

Total deposits

$406,233 $371,479

Core and market-based deposits

Core deposits

$363,402 $330,693

Market-based deposits

42,831 40,786

Total deposits

$406,233 $371,479

Additional sources of funds include short-term borrowings, long-term

debt and shareholders’ equity. Average short-term borrowings, a rel-

atively low-cost source of funds, were up $43.4 billion to $147.6 bil-

lion for 2003 compared to 2002 due to increases in federal funds

purchased and securities sold under agreements to repurchase of

$34.6 billion and other short-term borrowings of $8.8 billion that

were used to fund asset growth or facilitate trading activities.

Issuances and repayments of long-term debt were $17.2 billion and

$9.3 billion, respectively, for 2003.

Obligations and Commitments

We have contractual obligations to make future payments on debt

and lease agreements. Additionally, in the normal course of busi-

ness, we enter into contractual arrangements whereby we commit to

future purchases of products or services from unaffiliated parties.

Obligations that are legally binding agreements whereby we agree to

purchase products or services with a specific minimum quantity

defined at a fixed, minimum or variable price over a specified period

of time are defined as purchase obligations. Included in purchase

obligations are vendor contracts of $3.5 billion, commitments to pur-

chase securities of $5.1 billion and commitments to purchase loans

of $8.3 billion. The most significant of our vendor contracts include

communication services, marketing and software contracts. Other

long-term liabilities include our obligations related to the Qualified

Pension Plan, Nonqualified Pension Plans and Postretirement Health

and Life Plans (the Plans). Obligations to the Plans are based on the

current and projected obligations of the Plans, performance of the

Plans’ assets and any participant contributions, if applicable. During

2003 and 2002, we contributed $460 million and $823 million,

respectively, to the Plans, and we expect to make at least $87 million

of contributions during 2004. Management believes the effect of the

Plans on liquidity is not significant to our overall financial condition.

Debt and lease obligations are more fully discussed in Note 12 of the

consolidated financial statements.

40 BANK OF AMERICA 2003 BANK OF AMERICA 2003 41