Bank of America 2003 Annual Report Download - page 41

Download and view the complete annual report

Please find page 41 of the 2003 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

|

|

disclosure requirements of SFAS No. 123, “Accounting for Stock-

Based Compensation,” (SFAS 123) to require prominent disclosures

in both annual and interim financial statements about the method of

accounting for stock-based employee compensation and the effect of

the method used on reported results. The Corporation adopted the

fair value-based method of accounting for stock-based employee

compensation costs as of January 1, 2003. In accordance with SFAS

148, the Corporation has elected to use the prospective method of

adoption. All stock options granted under plans before the adoption

date will continue to be accounted for under Accounting Principles

Board (APB) Opinion No. 25, “Accounting for Stock Issued to

Employees,” (APB 25) unless these stock options are modified or

settled subsequent to adoption. SFAS 148 was effective for all stock

option awards granted in 2003 and thereafter. Under APB 25, the

Corporation accounted for stock options using the intrinsic value

method and no compensation expense was recognized, as the grant

price was equal to the strike price. Under the fair value method, stock

option compensation expense is measured on the date of grant using

an option-pricing model. The option-pricing model is based on certain

assumptions and changes to those assumptions may result in differ-

ent fair value estimates.

In accordance with SFAS 148, the Corporation provides disclo-

sures as if the Corporation had adopted the fair value-based method

of measuring all outstanding employee stock options in 2003, 2002

and 2001 as indicated in the following table. The prospective method

of accounting for stock options that the Corporation has elected to

follow, as allowed by SFAS 148, recognizes the impact of only newly

issued employee stock options. The following table presents the

effect on net income and earnings per common share had the fair

value-based method been applied to all outstanding and unvested

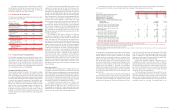

awards for the years ended December 31, 2003, 2002 and 2001.

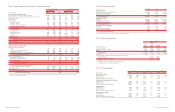

(Dollars in millions,

Year Ended December 31

except per share data)

2003 2002 2001

Net income

$10,810 $9,249 $ 6,792

Stock-based employee

compensation expense

recognized during period,

net of related tax effects

78 ––

Stock-based employee

compensation expense

determined under fair

value-based method,

net of related tax effects(1)

(225) (413) (351)

Pro forma net income

$10,663 $8,836 $ 6,441

As reported

Earnings per common share

$7.27 $6.08 $ 4.26

Diluted earnings per

common share

7.13 5.91 4.18

Pro forma

Earnings per common share

7.18 5.81 4.04

Diluted earnings per

common share

7.05 5.64 3.96

(1) Includes all awards granted, modified or settled for which the fair value was required to be

measured under SFAS 123, except restricted stock. Restricted stock expense, included in

net income, for the years ended December 31, 2003, 2002 and 2001 was $276, $250 and

$182, respectively.

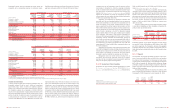

In determining the pro forma disclosures in the previous table, the

fair value of options granted was estimated on the date of grant using

the Black-Scholes option-pricing model and assumptions appropriate

to each plan. The Black-Scholes model was developed to estimate

the fair value of traded options, which have different characteristics

than employee stock options, and changes to the subjective assump-

tions used in the model can result in materially different fair value

estimates. The weighted average grant date fair values of the options

granted during 2003, 2002 and 2001 were based on the assump-

tions below. See Note 17 of the consolidated financial statements for

further discussion.

Compensation expense under the fair value-based method is recog-

nized over the vesting period of the related stock options.

Accordingly, the pro forma results of applying SFAS 123 in 2003,

2002 and 2001 may not be indicative of future amounts.

FASB Interpretation No. 45, “Guarantor’s Accounting and

Disclosure Requirements for Guarantees,” (FIN 45) was issued in

November 2002. FIN 45 requires that a liability be recognized at the

inception of certain guarantees for the fair value of the obligation, includ-

ing the ongoing obligation to stand ready to perform over the term of the

guarantee. Guarantees, as defined in FIN 45, include contracts that con-

tingently require the Corporation to make payments to a guaranteed

party based on changes in an underlying that is related to an asset,

liability or equity security of the guaranteed party, performance guaran-

tees, indemnification agreements or indirect guarantees of indebted-

ness of others. The accounting provisions of FIN 45 were effective for

certain guarantees issued or modified after December 31, 2002. The

adoption of FIN 45 did not have a material impact on the Corporation’s

results of operations or financial condition. In addition, FIN 45 requires

certain additional disclosures that are located in Notes 9 and 13 of the

consolidated financial statements.

BANK OF AMERICA 2003 7978 BANK OF AMERICA 2003

Bank of America Corporation and its subsidiaries (the Corporation)

through its banking and nonbanking subsidiaries, provide a diverse

range of financial services and products throughout the United States

and in selected international markets. At December 31, 2003, the

Corporation operated its banking activities primarily under two char-

ters: Bank of America, National Association (Bank of America, N.A.)

and Bank of America, N.A. (USA).

Note 1 Summary of Significant Accounting Principles

Principles of Consolidation and Basis of Presentation

The consolidated financial statements include the accounts of the

Corporation and its majority-owned subsidiaries, and those variable

interest entities (VIEs) where the Corporation is the primary bene-

ficiary. All significant intercompany accounts and transactions have

been eliminated. Results of operations of companies purchased are

included from the dates of acquisition. Certain prior period amounts

have been reclassified to conform to current period classifications.

Assets held in an agency or fiduciary capacity are not included in the

consolidated financial statements. The Corporation accounts for

investments in companies that it owns a voting interest of 20 percent

to 50 percent and for which it may have significant influence over

operating and financing decisions using the equity method of

accounting. These investments are included in other assets and the

Corporation’s proportionate share of income or loss is included in

other income.

The preparation of the consolidated financial statements in con-

formity with accounting principles generally accepted in the United

States requires management to make estimates and assumptions

that affect reported amounts and disclosures. Actual results could

differ from those estimates.

Recently Issued Accounting Pronouncements

In January 2003, the Financial Accounting Standards Board (FASB)

issued FASB Interpretation No. 46 “Consolidation of Variable Interest

Entities, an interpretation of ARB No. 51” (FIN 46). FIN 46 provides a

new framework for identifying VIEs and determining when a company

should include the assets, liabilities, noncontrolling interests and

results of activities of a VIE in its consolidated financial statements.

FIN 46 was effective immediately for VIEs created after January 31,

2003. As of October 9, 2003, the FASB deferred compliance under

FIN 46 from July 1, 2003 to the first period ending after December

15, 2003 for VIEs created prior to February 1, 2003. However, the

Corporation adopted FIN 46 on July 1, 2003, as originally issued, and

consolidated the assets and liabilities related to certain of its multi-

seller asset-backed commercial paper conduits. As of December 31,

2003, the total assets and liabilities were approximately $4.3 billion.

Prior periods were not restated. Prior to FIN 46, trust preferred secu-

rities were classified as a separate liability with distributions on

these securities included in interest expense on long-term debt. Upon

adoption of FIN 46, $6.1 billion of trust preferred securities vehicles,

which were deemed to be VIEs, were deconsolidated with the result-

ing liabilities to the trust companies included as a component of long-

term debt with no change in the reporting of distributions. In

December 2003, the FASB issued FASB Interpretation No. 46

(Revised December 2003) “Consolidation of Variable Interest

Entities, an interpretation of ARB No. 51” (FIN 46R). FIN 46R is an

update of FIN 46 and contains different implementation dates based

on the types of entities subject to the standard and based on whether

a company has adopted FIN 46. The Corporation anticipates adopt-

ing FIN 46R as of March 31, 2004 and does not expect that it will

have a material impact on the Corporation’s results of operations or

financial condition. For additional information on VIEs, see Note 9 of

the consolidated financial statements.

On May 15, 2003, the FASB issued Statement of Financial

Accounting Standards (SFAS) No. 150, “Accounting for Certain Financial

Instruments with Characteristics of both Liabilities and Equity” (SFAS

150) and was effective May 31, 2003 for all new and modified financial

instruments and otherwise was effective at the beginning of the first

interim period beginning after June 15, 2003. SFAS 150 changes the

accounting for certain financial instruments that, under previous guid-

ance, issuers could account for as equity. SFAS 150 requires that those

instruments be classified as liabilities (or assets in some circum-

stances). The adoption of this rule had no impact on the Corporation’s

results of operations or financial condition.

On April 30, 2003, the FASB issued SFAS No. 149, “Amendment

of Statement 133 on Derivative Instruments and Hedging Activities”

(SFAS 149) which is effective for hedging relationships entered into

or modified after June 30, 2003. SFAS 149 amends and clarifies

financial accounting and reporting for derivative instruments, includ-

ing certain derivative instruments embedded in other contracts and

for hedging activities under SFAS 133. The adoption of this rule did

not have a material impact on the Corporation’s results of operations

or financial condition.

SFAS No. 148, “Accounting for Stock-Based Compensation –

Transition and Disclosure – an amendment of FASB Statement No.

123,” (SFAS 148) was adopted by the Corporation on January 1,

2003. SFAS 148 provides alternative methods of transition for a

voluntary change to the fair value-based method of accounting for

stock-based employee compensation. SFAS 148 also amends the

Notes to Consolidated Financial Statements

Bank of America Corporation and Subsidiaries

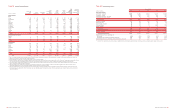

Risk-free Interest Rates Dividend Yield

2003 2002 2001 2003 2002 2001

Key Employee Stock Plan

3.82% 5.00% 5.05% 4.40% 4.76% 4.50%

Broad-based plans(1)

n/a 4.14 4.89 n/a 4.37 5.13

Expected Lives (Years) Volatility

2003 2002 2001 2003 2002 2001

Key Employee Stock Plan

77726.57% 26.86% 26.68%

Broad-based plans(1)

n/a 44 n/a 31.02 31.62

n/a = not applicable

(1) There were no options granted under broad-based plans in 2003.