Bank of America 2003 Annual Report Download - page 20

Download and view the complete annual report

Please find page 20 of the 2003 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

|

|

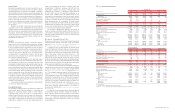

Total revenue increased $256 million, or 11 percent, in 2003

and net income increased 79 percent, due to lower provision for

credit losses of $317 million and an increase in equity investment

gains of $199 million. SVA increased by $287 million, or 354 per-

cent, as the increase in net income was partially offset by the impact

of an increase in capital levels. The increase in capital levels was

driven by additional goodwill recorded in mid-2002 representing final

contingent consideration in connection with the acquisition of the

remaining 50 percent of Marsico. All conditions related to this con-

tingent consideration have been met.

Client Assets

December 31

(Dollars in billions)

2003 2002

Assets under management

$335.7 $310.3

Client brokerage assets

88.8 90.9

Assets in custody

49.9 46.6

Total client assets

$474.4 $447.8

Assets under management, which consist largely of mutual funds,

equities and bonds, generate fees based on a percentage of their

market value. Compared to a year ago, assets under management

increased $25.4 billion, or eight percent, due to a $33.7 billion, or 41

percent, increase in equities, led by improved market valuations and

sales in assets advised by Marsico, offset by a decline of $13.2 bil-

lion, or eight percent, in money market assets. Client brokerage

assets, a source of commission revenue, decreased $2.1 billion, or

two percent. Client brokerage assets consist largely of investments

in bonds, annuities, money market mutual funds and equities. Assets

in custody increased $3.3 billion, or seven percent, and represent

trust assets administered for customers. Trust assets encompass a

broad range of asset types including real estate, private company

ownership interest, personal property and investments.

Net interest income remained relatively flat as growth in

deposits and increased loan spreads were offset by lower loan bal-

ances and the net results of ALM activities. Average loans and leases

decreased $773 million, or three percent, in 2003. Average deposits

increased $1.1 billion, or nine percent, in 2003.

Significant Noninterest Income Components

(Dollars in millions)

2003 2002

Asset management fees(1)

$1,160 $1,087

Brokerage income

420 435

Total investment and brokerage services

$1,580 $1,522

(1) Includes personal and institutional asset management fees, mutual fund fees and fees earned

on assets in custody.

Noninterest income increased $254 million, or 16 percent, in 2003

due to an increase in equity investment gains of $199 million related

to gains from securities sold that were received in satisfaction of

debt that had been restructured and charged off in prior periods and

higher asset management fees.

Provision for credit losses decreased $317 million, primarily due

to one large charge-off recorded in 2002.

Noninterest expense increased $120 million, or eight percent,

due to a $50 million allocation of the charge related to issues sur-

rounding our mutual fund practices, previously announced in the third

quarter of 2003 and increased expenses associated with the addi-

tion of financial advisors.

Global Corporate and Investment Banking

Our Global Corporate and Inve stme nt Banking strategy is to align our

resources with sectors where we can deliver value added financial

advisory solutions to our issuer and investor clients. As we broaden

and deepen our relationships with our strategic and priority clients, we

expect to build leading market shares that should provide our share-

holders sustainable revenue and SVA growth. Global Corporate and

Inve stme nt Banking provides a broad range of financial services to

domestic and international corporations, financial institutions, and

government entities. Clients are supported through offices in 30

countries in four distinct geographic regions: U.S. and Canada; Asia;

Europe, Middle East and Africa; and Latin America. Products and

services provided include loan origination, merger and acquisition

advisory, debt and equity underwriting and trading, cash manage-

ment, derivatives, foreign exchange, leasing, leveraged finance, struc-

tured finance and trade services.

Global Corporate and Inve stme nt Banking offers clients a

comprehensive range of global capabilities through three subseg-

ments: Global Inve stme nt Banking, Global Cre dit Products and Global

Tre asury Se rvice s.

Global Inve stme nt Banking includes our investment banking

activities and risk management products. Global Inve stme nt Banking

underwrites and makes markets for its clients in equity and equity-

linked securities, high-grade and high-yield corporate debt securities,

commercial paper, and mortgage-backed and asset-backed securities

as well as provides correspondent clearing services for other securi-

ties broker/dealers and prime-brokerage services. It also provides

debt and equity securities research, loan syndications, mergers and

acquisitions advisory services and private placements.

In addition, Global Inve stme nt Banking provides risk management

solutions for our global customer base using interest rate, equity,

credit and commodity derivatives, foreign exchange, fixed income and

mortgage-related products. In support of these activities, the busi-

nesses may take positions in these products and capitalize on mar-

ket-making activities. The Global Inve stme nt Banking business is a

primary dealer in the U.S. as well as in several international locations.

Global Cre dit Products provides credit and lending services for

our clients with our corporate industry-focused portfolios, which also

includes leasing. Global Cre dit Products is also responsible for

actively managing loan and counterparty risk in our large corporate

portfolio using available risk mitigation techniques, including credit

default swaps.

Global Tre asury Se rvice s provides the technology, strategies and

integrated solutions to help financial institutions, government agen-

cies and our corporate clients manage their operational cash flows

on a local, regional, national and global level.

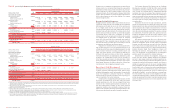

Our financial performance continues to improve as total revenue

increased $256 million, or three percent, in 2003, due to increases in

investment banking income of $188 million, miscellaneous other

income of $160 million, service charges of $63 million and invest-

ment and brokerage service fees of $58 million. Net income increased

$451 million, or 29 percent. SVA increased by $732 million, or 292

percent, as a result of lower capital, the increase in net income and a

decrease in the capital charge related to improving credit quality

including a reduction in nonperforming assets.

Net interest income remained relatively flat at $4.8 billion.

Average loans and leases declined $13.8 billion, or 22 percent, in

2003, primarily as a result of either the client selection process or

refinancing by clients in the public markets as companies restruc-

tured their capital positions coupled with the lack of demand for addi-

tional bank debt as capital expenditures or inventory financing

continued to be moderate. Average deposits increased $1.4 billion,

or two percent, in 2003, despite decreases in compensating bal-

ances by the U.S. Treasury and foreign deposits.

Noninterest income increased $228 million, or six percent, in

2003, as increases in investment banking income, service charges,

and investment and brokerage services were partially offset by a

decline in trading account profits. Active market-based trading

account profits increased by $170 million; however, this was more

than offset by credit portfolio hedges that decreased by $414 million.

Investment banking income increased $188 million, or 13 per-

cent, in 2003. We continued to maintain syndicated lending and fixed

income market share and gained in areas such as mergers and

acquisitions, and mortgage-backed securities. Although the overall

market for securities underwriting declined for equity offerings, our

continued strong market share in equity offerings resulted in a 34

percent increase in securities underwriting fees.

Investment Banking Income

(Dollars in millions)

2003 2002

Securities underwriting

$963 $721

Syndications

428 427

Advisory services

228 288

Other 50 45

Total

$1,669 $1,481

Investment and brokerage services income was $693 million and $636

million in 2003 and 2002, respectively. Service charges on accounts

were $1.2 billion for both periods.

Trading-related net interest income as well as trading account

profits in noninterest income (trading-related revenue) are presented

in the following table as they are both considered in evaluating the

overall profitability of our trading activities. Certain prior period

amounts have been reclassified among products to conform to the

current period presentation.

Trading-related Revenue

(Dollars in millions)

2003 2002

Net interest income (fully taxable-equivalent basis)

$2,214 $1,976

Trading account profits 588 832

Total trading-related revenue

$2,802 $2,808

Trading-related revenue by product

Fixed income

$1,371 $833

Interest rate (fully taxable-equivalent basis)

922 879

Foreign exchange

549 532

Equities(1)

337 386

Commodities

(47) 94

Market-based trading-related revenue

3,132 2,724

Credit portfolio hedges(2)

(330) 84

Total trading-related revenue

$2,802 $2,808

(1) Does not include commission revenue from equity transactions.

(2) Includes credit default swaps used for credit risk management.

Total trading-related revenue remained flat at $2.8 billion as the

$238 million increase in net interest income was offset by a $244

million decrease in trading account profits in 2003. This decrease in

trading account profits was principally attributable to the $414 million

decrease in revenue from credit portfolio hedges used as part of the

overall credit risk management process. For additional information on

credit portfolio hedges, see Concentrations of Credit Risk on page 45.

Market-based trading-related revenue increased by $408 million, or

15 percent, resulting from an increase of $538 million in fixed

income trading. Driving the increase in fixed income trading were

increased high-yield sales and trading activities of $283 million and

an increase of $23 million of sales and trading activities in mortgage-

backed securities. Interest rate sales and trading increased $43 mil-

lion due to general trading-related activities in the improving

economy. Offsetting this increase was a decline in commodities rev-

enue of $141 million primarily due to the adverse impact on jet fuel

prices from the SARS outbreak in the second quarter of 2003.

Equities also declined by $49 million, which was offset by an increase

of $63 million in trading commissions that was included in invest-

ment and brokerage services income. The growth in our overall trad-

ing reflects the strength of our debt sales and trading platform, which

capitalized on the tightening of credit spreads and stronger distribu-

tion capabilities in the investor market.

Continued improvements in credit quality in our large corporate

portfolio drove the $731 million, or 61 percent, decrease in provision

for credit losses. In 2003, net charge-offs of $690 million in the large

corporate portfolio were at their lowest levels in three years. Large

corporate nonperforming assets dropped $1.7 billion, or 57 percent,

in 2003, due to reduced levels of inflows of $2.3 billion, nonper-

forming loan sales of $1.4 billion, charge-offs of $841 million, and

paydowns and payoffs of $667 million.

Noninterest expense increased $372 million, or seven percent,

due to costs associated with downsizing operations in South America

and Asia and restructuring of locations within the United States of

$113 million, higher incentive compensation for market-based activi-

ties of $104 million, increased expenses from ongoing litigation and

litigation reserves of $74 million, and a $50 million allocation of the

charge related to issues surrounding our mutual fund practices.

36 BANK OF AMERICA 2003 BANK OF AMERICA 2003 37