Bank of America 2003 Annual Report Download - page 24

Download and view the complete annual report

Please find page 24 of the 2003 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

|

|

The capital treatment of Trust Securities is currently under review

by the FRB due to the issuing trust companies being deconsolidated

under FIN 46. Depending on the capital treatment resolution, Trust

Securities may no longer qualify for Tier 1 Capital treatment,

but instead would qualify for Tier 2 Capital. On July 2, 2003, the FRB

issued a Supervision and Regulation Letter (the Letter) requiring that

bank holding companies continue to follow the current instructions

for reporting Trust Securities in its regulatory reports. Accordingly, we

will continue to report Trust Securities in Tier 1 Capital until further

notice from the FRB. On September 2, 2003, the FRB and other

regulatory agencies, issued the Interim Final Capital Rule for

Consolidated Asset-backed Commercial Paper Program Assets (the

Interim Rule). The Interim Rule allows companies to exclude from

risk-weighted assets, the newly consolidated assets of asset-backed

commercial paper programs required by FIN 46, when calculating Tier 1

and Total Risk-based Capital ratios through March 31, 2004. As of

December 31, 2003, in accordance with FIN 46, as originally issued,

we consolidated approximately $4.3 billion of assets of multi-seller

asset-backed commercial paper conduits. See Notes 1 and 9 of the

consolidated financial statements for additional information on FIN 46.

Credit Risk Management

Credit risk is the risk of loss arising from a customer or counter-

party’s inability to meet its obligation and exists in our outstanding

loans and leases, trading account assets, derivative assets and

unfunded lending commitments that include loan commitments,

letters of credit and financial guarantees. We define the credit exposure

to a client as the amount representing the maximum loss potential

arising from all these product classifications, except for derivative

positions where we use the current mark-to-market values of the

counterparty component to represent credit exposure without giving

consideration to future mark-to-market changes. Our commercial and

consumer credit extension and review procedures take into account

credit exposures that are both funded and unfunded. For additional

information on derivatives and credit extension commitments, see

Notes 6 and 13 of the consolidated financial statements.

We manage credit risk based on the risk profile of the borrower,

repayment source and the nature of underlying collateral given

current events and conditions. At a macro level, we segregate our

loans in two major groups: commercial and consumer.

Commercial Portfolio Credit Risk Management

Commercial credit risk management begins with an assessment of

the credit risk profile of an individual borrower (or counterparty)

based on an analysis of the borrower’s financial position in conjunc-

tion with current industry, economic and macro geopolitical trends. As

part of the overall credit risk assessment of a borrower, each com-

mercial credit exposure or transaction is assigned a risk rating and is

subject to approval based on defined credit approval standards.

Subsequent to loan origination, risk ratings are adjusted on an ongo-

ing basis, if necessary, to reflect changes in the obligor’s financial

condition, cash flow or ongoing financial viability. We use risk rating

aggregations to measure and evaluate concentrations within portfolios.

Risk ratings are also a factor in determining the level of assigned

economic capital and the allowance for credit losses. In making

decisions regarding credit, we consider risk rating, collateral, country,

industry and single name concentration limits while also balancing

the total client relationship and SVA.

Both our lines of business and Risk Management personnel use

a variety of tools to continuously monitor a borrower/counterparty’s

ability to perform under its obligations. Adjustments in credit exposures

are made as a result of this ongoing analysis and review. Additionally,

we utilize syndication of exposure to other entities, loan sales, credit

derivatives and collateralized loan obligations (CLOs) to manage the

size of the loan portfolio. These activities play an important role in

reducing credit exposures for risk mitigation purposes or where it has

been determined that credit risk concentrations are undesirable.

Banc of America Strategic Solutions, Inc. (SSI) is a majority-

owned consolidated subsidiary of Bank of America, N.A., a wholly-

owned subsidiary of the Corporation, that manages problem asset

resolution and the coordination of exit strategies, if applicable, includ-

ing bulk sales, collateralized debt obligations and other resolutions of

domestic commercial distressed assets. For additional discussion,

see “Problem Loan Management” on page 50.

Consumer Portfolio Credit Risk Management

Credit risk management for consumer credit begins with initial under-

writing and occurs throughout a borrower’s credit cycle. Statistical

techniques are used to establish product pricing, risk appetite, oper-

ating processes and metrics to balance risks and rewards appropri-

ately. Consumer exposure is grouped by product and other attributes

for purposes of evaluating credit risk. Statistical models are built

using detailed behavioral information from external sources such as

credit bureaus as well as internal historical experience. These models

form the foundation of our consumer credit risk management process

and are used in determining approve/decline credit decisions, col-

lections management procedures, portfolio management decisions,

adequacy of the allowance for loan and lease losses, and economic

capital allocation for credit risk.

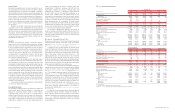

Table 10

Outstanding Loans and Leases

December 31

2003 2002

(Dollars in millions)

Amount Percent Amount Percent

Commercial – domestic

$96,644 26.0% $105,053 30.6%

Commercial – foreign

15,293 4.1 19,912 5.8

Commercial real estate

– domestic

19,043 5.1 19,910 5.8

Commercial real estate

– foreign

324 0.1 295 0.1

Total commercial

131,304 35.3 145,170 42.3

Residential mortgage

140,513 37.8 108,197 31.6

Home equity lines

23,859 6.4 23,236 6.8

Direct/Indirect consumer

33,415 9.0 31,068 9.1

Consumer finance

5,589 1.5 8,384 2.4

Credit card

34,814 9.4 24,729 7.2

Foreign consumer

1,969 0.6 1,971 0.6

Total consumer

240,159 64.7 197,585 57.7

Total(1)

$371,463 100.0% $342,755 100.0%

(1) Includes lease financings of $11,376 and $14,332 at December 31, 2003 and 2002, respectively.

Concentrations of Credit Risk

Portfolio credit risk is evaluated with a goal that concentrations of

credit exposure do not result in undesirable levels of risk. We review

and measure concentrations of credit exposure by industry, product,

geography and customer relationship. Risk due to borrower concentra-

tions is more prevalent in the commercial portfolio. We also review and

measure commercial real estate loans by geographic location and prop-

erty type. Additionally, within our international portfolio, we also evalu-

ate borrowings by region and by country. Tables 11 and 12, Table

X

on

page 63 and Table

XI

on page 64 summarize these concentrations.

From the perspective of portfolio risk management, customer

concentration management is most relevant in Global Corporate and

Inve stme nt Banking. Within Global Corporate and Inve stme nt Banking,

concentrations continue to be addressed through the underwriting

and ongoing monitoring processes, the established strategy of

“originate to distribute” and partly through the purchase of credit pro-

tection through credit derivatives. We utilize various risk mitigation

tools to hedge our economic risk to certain credit counterparties,

including credit default swaps and CLOs in which a layer of loss is

sold to third parties. However, this gives rise to earnings volatility as

a consequence of accounting asymmetry as we mark to market our

credit default swaps through trading account profits and CLOs as

required by SFAS 133, while the loans are recorded at historical cost

less an allowance for credit losses or, if held for sale, the lower of

cost or market.

As previously discussed, the improvement in credit quality con-

tributed to a $731 million, or 61 percent, decrease in provision for

credit losses reported in Global Corporate and Inve stme nt Banking.

However, the credit portfolio hedges lost $330 million in value for

2003 compared to an increase in value of $84 million for 2002 as a

result of narrowing credit spreads due to improved credit quality in

the large corporate sector. At December 31, 2003 and 2002, the

notional amount of these credit derivatives was $14.8 billion and

$16.7 billion, respectively.

During 2003, we entered into several transactions whereby we

purchased credit protection on a portion of our residential mortgage

loan portfolio from unaffiliated parties. These transactions are

designed to aid us as part of our ALM overall risk management strat-

egy. At December 31, 2003, approximately $63.4 billion of residen-

tial mortgage loans were covered by the purchased credit protection.

Our regulatory risk-weighted assets were reduced as a result of this

transaction because we had effectively transferred a degree of credit

risk on these loans to unaffiliated parties. These transactions had

the effect of reducing our risk-weighted assets by $18.6 billion and

resulted in a 26 bp increase in our Tier 1 Risk-based Capital ratio at

December 31, 2003.

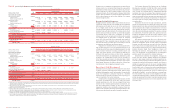

Table 11 shows utilized commercial credit exposure by signi-

ficant industry based on Standard and Poor’s industry classifications

and includes commercial loans and leases, commercial letters of

credit, SBLCs and financial guarantees as well as the mark-to-market

exposure for derivatives. As depicted in the table, we believe that

utilized commercial credit exposure is well-diversified across a range

of industries.

Table 11

Utilized Commercial Credit Exposure by Significant Industry

December 31

(Dollars in millions)

2003 2002

Banks

$25,088 $20,889

Real estate

22,228 22,463

Diversified financials

20,427 21,818

Retailing

15,152 13,560

Education and government

13,919 10,196

Leisure and sports, hotels and restaurants

10,099 10,970

Transportation

9,355 9,941

Food, beverage and tobacco

9,134 9,692

Materials

8,860 11,256

Consumer durables and apparel

8,313 8,078

Capital goods

8,244 9,863

Commercial services and supplies

7,206 7,674

Health care equipment and services

7,064 6,729

Utilities

5,012 8,109

Media

4,701 7,675

Energy

4,348 4,770

Other(1)

33,744 36,285

Total

$212,894 $219,968

(1) At December 31, 2003 and 2002, Other included amounts for Individuals and Trusts of credit

exposure outstanding of $14,307 and $13,481, respectively, representing 6.7 percent and 6.1

percent of total commercial credit exposure, respectively. The remaining balance in Other

included credit exposure to religious and social organizations, insurance, telecommunications

services, technology hardware and equipment, and food and staples retailing.

An additional measure of the risk diversification is the distribution of

loans by loan size. Table

IX

on page 63 presents the non-real estate

outstanding commercial loans and leases by significant industry.

Over 99 percent of the non-real estate outstanding commercial loans

and leases were less than $50 million, representing 89 percent of

the total outstanding amount of non-real estate commercial loans

and leases. We believe that the non-real estate commercial loan and

lease portfolio is well-diversified across a range of industries.

Table

X

on page 63 presents outstanding commercial real estate

loans by geographic region and by property type. The amounts pre-

sented in Table

X

do not include outstanding loans and leases that

were made on the general creditworthiness of the borrower, for which

real estate was obtained as security and for which the ultimate repay-

ment of the credit is not dependent on the sale, lease, rental or refi-

nancing of the real estate. Accordingly, the outstandings presented

do not include commercial loans secured by owner-occupied real

estate. Over 99 percent of the commercial real estate loans out-

standing in Table

X

were less than $50 million, representing 96 per-

cent of the total outstanding amount of commercial real estate loans.

We believe the commercial real estate loan portfolio is well-diversi-

fied in terms of both geographic region and property type.

44 BANK OF AMERICA 2003 BANK OF AMERICA 2003 45