Bank of America 2003 Annual Report Download - page 28

Download and view the complete annual report

Please find page 28 of the 2003 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

|

|

To e valuate risk in our trading activities, we focus on the actual and

potential volatility of individual positions as well as portfolios. At a

portfolio and corporate level, we use Value-at-Risk (VAR) modeling

and stress testing. VAR is a key statistic used to measure and man-

age market risk. Trader limits and VAR are used to manage day-to-day

risks and are subject to testing where we compare expected per-

formance to actual performance. This testing provides us a view of

our models’ predictive accuracy. All limit excesses are communicated

to senior management for review.

A VAR model estimates a range of hypothetical scenarios within

which the next day’s profit or loss is expected. These estimates are

impacted by the nature of the positions in the portfolio and the cor-

relation within the portfolio. Within any VAR model, there are signifi-

cant and numerous assumptions that will differ from company to

company. Our VAR model assumes a 99 percent confidence level.

During the fourth quarter of 2002, we completed an enhancement of

our methodology used in the VAR risk aggregation calculation. This

approach utilizes historical market conditions over the last three

years to derive estimates of trading risk and provides the ability to

aggregate trading risk across different businesses. Historically, we

used a mathematical method to allocate risk across different trading

businesses that did not assume the benefit of diversification across

markets. This change resulted in a lower VAR calculation starting in

the fourth quarter 2002.

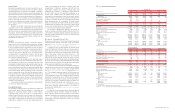

The reduction in average VAR for 2003 was primarily due to the

2002 methodology enhancements and the $5 million decline in real

estate/mortgages, partially offset by increases in equities of $11

million. The increase in equities was mainly due to the increased eco-

nomic risk from customer-facilitated business that was held in inven-

tory throughout the first three quarters of 2003 and sold during the

fourth quarter 2003. The large increase in the interest rate and total

trading portfolio high VAR was due to activities on one day during the

period. The next highest VAR for interest rates and total trading port-

folio was $47.4 million and $61.2 million, respectively, during 2003.

Stress Te sting

Because the very nature of a VAR model suggests results can exceed

our estimates, we “stress test” our portfolio. Stress testing esti-

mates the value change in our trading portfolio due to abnormal mar-

ket movements. Various stress scenarios are run regularly against

the trading portfolio to verify that, even under extreme market moves,

we will preserve our capital; to determine the effects of significant

historical events; and to determine the effects of specific, extreme

hypothetical, but plausible events. The results of the stress scenar-

ios are calculated daily and reported to senior management as part

of the regular reporting process. The results of certain specific,

extreme hypothetical scenarios are presented to ALCO.

In addition, each business has established risk concentration

limits with the goal of ensuring the amount of risk taken within each

business is consistent with the risk appetite for that business. Each

business is independently monitored to assure adherence to

approved risk measures, limits and controls. The primary risk mitiga-

tion tool involves monitoring exposures relative to concentration, bal-

ance sheet, notional and derivative limits.

Interest Rate Risk Management

Interest rate risk represents the most significant market risk expo-

sure to our nontrading financial instruments. Our overall goal is to

manage interest rate sensitivity so that movements in interest rates

do not adversely affect net interest income. Interest rate risk is

measured as the potential volatility to our net interest income caused

by changes in market interest rates. Client facing activities, primarily

lending and deposit-taking, create interest rate sensitive positions on

our balance sheet. Interest rate risk from these activities as well as

the impact of ever-changing market conditions, is mitigated using the

ALM process.

Sensitivity simulations are used to estimate the impact on net

interest income of numerous interest rate scenarios, balance sheet

trends and strategies. These simulations estimate levels of short-term

Statistically this means that losses will exceed VAR, on average, one

out of 100 trading days, or two to three times a year. Actual losses

exceeded VAR twice in 2003, did not exceed VAR in 2002 and

exceeded VAR once in 2001.

There are numerous assumptions and estimates associated

with modeling, and actual results could differ. In addition to reviewing

our underlying model assumptions with senior management, we mit-

igate the uncertainties related to these assumptions and estimates

through close monitoring and by updating the assumptions and esti-

mates on an ongoing basis. If the results of our analysis indicate

higher than expected levels of risk, proactive measures are taken to

adjust risk levels.

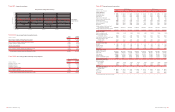

Table 18 presents average, high and low daily VAR for both 2003

and 2002.

financial instruments, securities, loans, deposits, borrowings and

derivative instruments. In addition, these simulations incorporate

assumptions about balance sheet dynamics such as loan and deposit

growth and pricing, changes in funding mix, and asset and liability

repricing and maturity characteristics. In addition to net interest

income sensitivity simulations, market value sensitivity measures are

also utilized.

The Balance Sheet Management group maintains a net interest

income forecast utilizing different rate scenarios, including a most

likely scenario, which is designed around an economic forecast that

is meant to estimate our expectation of the most likely path of rates

for the upcoming horizon. The Balance Sheet Management group con-

stantly updates the net interest income forecast for changing

assumptions and differing outlooks based on economic trends and

market conditions.

The Balance Sheet Management group reviews the impact on

net interest income of parallel and nonparallel shifts in the yield

curve over different horizons. The overall interest rate risk position

and strategies are reviewed on an ongoing basis with ALCO. At

December 31, 2003, we were positioned to benefit from rising long-

term interest rates, with short-term interest rates being stable.

Table 19 provides our estimated net interest income at risk over

the subsequent year from December 31, 2003 and 2002, resulting

from a 100 bp gradual (over 12 months) increase or decrease in inter-

est rates from the forward curve calculated as of December 31, 2003

and 2002, respectively. Beginning in the third quarter 2003, these

shocks were applied to the forward interest rate curve implied by the

financial markets. Previously, these shocks were applied to current

interest rates held stable. This change more closely aligns these risk

measures with management’s view of this risk. The prior period has

been restated to conform to the current methodology.

Table 19

Estimated Net Interest Income at Risk

-100 bp +100 bp

December 31, 2003

1.2% (1.1)%

December 31, 2002

0.5% 1.4%

As part of the ALM process, we use securities, residential mortgages,

and interest rate and foreign exchange derivatives in managing interest

rate sensitivity.

Se curitie s

The securities portfolio is integral to our ALM process. The decision

to purchase or sell securities is based upon the current assessment

of economic and financial conditions, including the interest rate envi-

ronment, liquidity and regulatory requirements, and the relative mix of

cash and derivative positions. In 2003 and 2002, we purchased

securities of $195.9 billion and $146.0 billion, respectively, sold

$171.5 billion and $137.1 billion, respectively and received pay-

downs of $27.2 billion and $25.0 billion, respectively. Not included in

the purchases above were $65.2 billion of forward purchase con-

tracts of both mortgage-backed securities and mortgage loans at

December 31, 2003 settling from January 2004 to February 2004

with an average yield of 5.79 percent, and $3.5 billion of forward pur-

chase contracts of both mortgage-backed securities and mortgage

loans at December 31, 2002 settling in January 2003 with an aver-

age yield of 5.91 percent. These forward purchase contracts,

included in Table 20, were accounted for as derivatives and their net-

of-tax unrealized gains and losses were included in accumulated

other comprehensive income (OCI). The pre-tax unrealized gain on

these forward purchase contracts at December 31, 2003 and 2002

was $1.9 billion and $58 million, respectively. There were also $8.0

billion of forward sale contracts of mortgage-backed securities at

December 31, 2003 settling in February 2004 with an average yield

of 6.14 percent, and $19.7 billion of forward sale contracts of mort-

gage-backed securities at December 31, 2002 settling in January and

February 2003 with an average yield of 6.05 percent. These forward

sale contracts, included in Table 20, were accounted for as deriva-

tives and their net-of-tax unrealized gains and losses were included

in accumulated OCI. The pre-tax unrealized gain on these forward

sale contracts at December 31, 2003 was $22 million compared to

a pre-tax unrealized loss of $189 million at December 31, 2002.

During the year, we continuously monitored the interest rate risk posi-

tion of the portfolio and repositioned the securities portfolio in order

to mitigate risk and to take advantage of interest rate fluctuations.

Through sales in the securities portfolio, we realized $941 million

and $630 million in gains on sales of debt securities during 2003

and 2002, respectively.

Re side ntial Mortgage Portfolio

We repositioned the ALM mortgage loan portfolio to mitigate prepay-

ment risk resulting from the unusually low rate environment. The res-

idential mortgages, a component of our ALM strategy, grew primarily

through whole loan purchase activity. In 2003 and 2002, we pur-

chased $92.8 billion and $55.0 billion, respectively, of residential

mortgages in the wholesale market for our ALM portfolio and interest

rate risk management. Not included in the purchases above were

$4.6 billion of forward purchase commitments of mortgage loans at

December 31, 2003 settling in January 2004. These commitments,

included in Table 20, were accounted for as derivatives at December

31, 2003 under the provisions of SFAS No. 149 “Amendment of

Statement 133 on Derivative Instruments and Hedging Activities”

(SFAS 149) and their net-of-tax unrealized gains and losses were

included in accumulated OCI. The pre-tax unrealized gain on these

forward purchase commitments at December 31, 2003 was $10 mil-

lion. During 2003 and 2002, we sold $27.5 billion and $22.7 billion,

respectively, of whole mortgage loans and recognized $772 million

and $500 million, respectively, in gains on the sales included in other

noninterest income. Additionally, during the same periods we

received paydowns of $62.8 billion and $36.9 billion, respectively.

Inte re st Rate and Fore ign Exchange De rivative Contracts

Interest rate and foreign exchange derivative contracts are utilized in our

ALM process and serve as an efficient, low-cost tool to mitigate our risk.

We use derivatives to hedge or offset the changes in cash flows or mar-

ket values of our balance sheet. See Note 6 of the consolidated finan-

cial statements for additional information on our hedging activities.

Our interest rate contracts are generally nonleveraged generic

interest rate and basis swaps, options, futures and forwards. In addi-

tion, we use foreign currency contracts to mitigate the foreign

exchange risk associated with foreign-denominated assets and liabil-

ities, as well as our equity investments in foreign subsidiaries. Table

20 reflects the notional amounts, fair value, weighted average receive

fixed and pay fixed rates, expected maturity and estimated duration

of our ALM derivatives at December 31, 2003 and 2002.

52 BANK OF AMERICA 2003 BANK OF AMERICA 2003 53

Table 18

Trading Activities Market Risk

2003 2002

Average High Low Average High Low

(Dollars in millions) VAR VAR(1) VAR(1) VAR VAR(1) VAR(1)

Foreign exchange

$4.1 $7.8 $ 2.1 $3.2 $ 7.1 $ 0.5

Interest rate

27.0 65.2 15.1 28.8 40.3 17.3

Credit(2)

20.7 32.6 14.9 14.8 21.6 6.5

Real estate/mortgage(3)

14.1 41.4 3.6 19.2 61.6 2.5

Equities

19.9 53.8 6.6 8.8 18.2 4.3

Commodities

8.7 19.3 4.1 9.2 15.4 3.4

Portfolio diversification

(60.9) – – (43.9) – –

Total trading portfolio

$33.6 $91.0 $11.2 $40.1 $69.8 $19.2

(1) The high and low for the total portfolio may not equal the sum of the individual components as the highs or lows of the individual portfolios may have occurred on different trading days.

(2) Credit includes credit fixed income and credit default swaps used for credit risk management.

(3) Real estate/mortgage, which is included in the fixed income category in Table 3 includes capital market real estate and mortgage banking certificates.