Bank of America 2003 Annual Report Download - page 29

Download and view the complete annual report

Please find page 29 of the 2003 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

|

|

54 BANK OF AMERICA 2003 BANK OF AMERICA 2003 55

Consistent with our strategy of managing interest rate sensitivity, the

notional amount of our net received fixed interest rate swap position

decreased $33.6 billion to $21.2 billion at December 31, 2003 com-

pared to December 31, 2002 to mitigate changes in value of other

financial instruments. The net option position increased $36.6 billion

to $85.0 billion at December 31, 2003 compared to December 31,

2002 to offset interest rate risk in other portfolios. This increase

occurred throughout 2003.

Mortgage Banking Risk Management

Mortgage production activities create unique interest rate and pre-

payment risk. Interest rate risk occurs between the loan commitment

date (pipeline) and the date the loan is sold to the secondary mar-

ket. To mitigate interest rate risk, we enter into various financial

instruments including interest rate swaps, forward delivery contracts,

Eurodollar futures and option contracts. The notional amount of such

contracts was $13.1 billion at December 31, 2003 with associated

net unrealized losses of $42 million. At December 31, 2002, the

notional amount of such contracts was $25.3 billion with associated

net unrealized losses of $224 million. Of these net unrealized

losses, $27 million and $140 million, respectively, were recorded in

accumulated OCI. These unrealized losses at December 31, 2003

and 2002 were offset by economic gains in the warehouse that will

be recognized upon delivery to the secondary market.

Prepayment risk represents the loss in value associated with a

high rate loan paying off in a low rate environment and the loss of

servicing value when loans prepay. We mitigate prepayment risk using

various financial instruments including purchased options and

swaps. The notional amounts of such contracts at December 31,

2003 and 2002 were $64.2 billion and $53.1 billion, respectively.

The related unrealized loss was $328 million at December 31, 2003

compared to an unrealized gain of $955 million at December 31,

2002. These amounts are included in the Derivatives table in Note 6

of the consolidated financial statements. See Note 1 of the consoli-

dated financial statements for additional discussion of these finan-

cial instruments in the mortgage banking assets section.

Operational Risk Management

Operational risk is the potential for loss resulting from events involv-

ing people, processes, technology, external events, execution, legal,

compliance and regulatory matters, and reputation. Successful oper-

ational risk management is particularly important to a diversified

financial services company like ours because of the very nature, vol-

ume and complexity of our various businesses.

In keeping with our management governance structure, the lines

of business are responsible for all the risks within the business

including operational risks. Such risks are managed through corpo-

rate-wide or line of business specific policies and procedures, con-

trols and monitoring tools. Examples of these include personnel

management practices, data reconciliation processes, fraud man-

agement units, transaction processing monitoring and analysis, busi-

ness recovery planning, and new product introduction processes.

The Corporate Operational Risk Executive and the Compliance

Risk Executive, reporting to the Chief Risk Officer, provide oversight

to facilitate the consistency of effective policies, “best industry prac-

tices”, controls and monitoring tools for managing and assessing

operational risks across the company. These executives also work

with the business segment executives and their risk counterparts to

implement appropriate policies, processes and assessments at the

line of business level. Compliance and operational risk awareness is

also driven across the company through training and strategic com-

munication efforts.

Operational risks fall into two major classifications, business

specific and corporate-wide risks affecting all business lines. At the

business segment level, there are Business Segment Risk Executives

that are responsible for oversight of all operational risks in the busi-

ness segments they support. In their management of these specific

risks, they utilize corporate-wide operational risk policies, processes

and assessments. For business specific risks, operational and com-

pliance risk management work with the business segments to drive

consistency in policies, processes, assessments and use of “best

industry practices.”

With respect to corporate-wide risks, such as information secu-

rity, business recovery, legal and compliance, operational and com-

pliance risk management assess the risks, develop a consolidated

corporate view and communicate that view to the line of business

level. To help assess and manage corporate-wide risks, we also uti-

lize specialized support groups, such as Legal, Information Security,

Business Recovery, Supply Chain Management, Finance, and

Technology and Operations. These groups assist the lines of busi-

ness in the development and implementation of risk management

practices specific to the needs of the individual businesses.

Operational and compliance risk management, working in con-

junction with senior business segment executives, have developed

key tools to help manage, monitor and summarize operational risk.

One such tool the businesses and executive management utilize is a

corporate-wide quarterly self-assessment process, which helps to

identify and evaluate the status of risk issues, including mitigation

plans, if appropriate. The goal of this process, which originates at the

line of business level, is to continuously assess changing market and

business conditions. The self-assessment process also assists in

identifying emerging operational risk issues and determining how

they should be managed – at the line of business or corporate level.

The risks identified in this process are also integrated into our quar-

terly financial forecasting process. In addition to the self-assessment

process, key operational risk indicators have been developed and are

used to help identify trends and issues on both a corporate and a line

of business level.

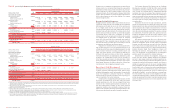

Table 20

Asset and Liability Management Interest Rate and Foreign Exchange Contracts

December 31, 2003

Average

(Dollars in millions, average

Fair Expected Maturity Estimated

estimated duration in years)

Value Total 2004 2005 2006 2007 2008 Thereafter Duration

Open interest rate contracts

Total receive fixed swaps(1)

$(1,204) 5.45

Notional amount

$156,772 $ – $ 4,580 $ 4,363 $36,348 $36,199 $75,282

Weighted average receive rate

3.78% –% 3.61% 5.22% 3.18% 3.00% 4.38%

Total pay fixed swaps(1)

(2,103) 5.41

Notional amount

$135,578 $ 81 $ 3,688 $ 14,581 $39,254 $13,650 $64,324

Weighted average pay rate

4.01% 6.04% 2.13% 2.93% 3.34% 3.78% 4.82%

Basis swaps

38

Notional amount

$16,356 $ 9,000 $ 500 $ 4,400 $ 45 $ 590 $ 1,821

Total swaps

(3,269)

Option products(2)

1,582

Net notional amount(3)

$84,965 $ 1,267 $50,000 $ 3,000 $ – $30,000 $ 698

Futures and forward rate contracts(4)

1,908

Net notional amount(3)

$106,156 $86,156 $20,000 $ – $ – $ – $ –

Total open interest rate contracts

221

Closed interest rate contracts(5,6)

839

Net interest rate contract position

1,060

Open foreign exchange contracts

1,129

Notional amount

$7,364 $ 100 $ 488 $ 468 $ (379) $ 1,560 $ 5,127

Total ALM contracts

$2,189

December 31, 2002

Average

(Dollars in millions, average

Fair Expected Maturity Estimated

estimated duration in years)

Value Total 2003 2004 2005 2006 2007 Thereafter Duration

Open interest rate contracts

Total receive fixed swaps(1)

$4,449 4.89

Notional amount

$116,520 $ 3,132 $ 3,157 $ 5,719 $14,078 $16,213 $74,221

Weighted average receive rate

4.29% 1.76% 3.17% 4.66% 4.50% 3.90% 4.46%

Total pay fixed swaps(1)

(1,825) 4.07

Notional amount

$61,680 $10,083 $ 5,694 $ 7,993 $15,068 $ 6,735 $16,107

Weighted average pay rate

3.60% 1.64% 2.46% 3.90% 3.17% 3.62% 5.48%

Basis swaps

(3)

Notional amount

$15,700 $ – $ 9,000 $ 500 $ 4,400 $ – $ 1,800

Total swaps

2,621

Option products(2)

650

Net notional amount(3)

$48,374 $ 1,000 $ 6,767 $40,000 $ – $ – $ 607

Futures and forward rate contracts(4)

(88)

Net notional amount(3)

$8,850 $(6,150) $15,000

Total open interest rate contracts

3,183

Closed interest rate contracts(5,6)

955

Net interest rate contract position

4,138

Open foreign exchange contracts

313

Notional amount

$4,672 $ 78 $ 648 $ 102 $ 1,581 $ 96 $ 2,167

Total ALM contracts

$4,451

(1) At December 31, 2003, $14.2 billion of the receive fixed swap notional and $114.5 billion of the pay fixed swap notional represented forward starting swaps that will not be effective until their respective

contractual start dates. At December 31, 2002, $39.0 billion of the receive fixed swap notional and $22.4 billion of the pay fixed swap notional represented forward starting swaps that will not be effective

until their respective contractual start dates.

(2) Option products include caps, floors and exchange-traded options on index futures contracts. These strategies may include option collars or spread strategies, which involve the buying and selling

of options on the same underlying security or interest rate index.

(3) Reflects the net of long and short positions.

(4) Futures and forward rate contracts include Eurodollar futures, U.S. Treasury futures and forward purchase and sale contracts. Included are $69.8 billion of forward purchase contracts and

$8.0 billion of forward sale contracts of mortgage-backed securities and mortgage loans, at December 31, 2003, as discussed on page 53. At December 31, 2002 the forward purchase and sale

contracts of mortgage-backed securities and mortgage loans amounted to $3.5 billion and $19.7 billion, respectively.

(5) Represents the unamortized net realized deferred gains associated with closed contracts. As a result, no notional amount is reflected for expected maturity.

(6) The $839 million and $955 million deferred gains on closed interest rate contracts primarily consisted of gains on closed ALM swaps. Of these unamortized net realized deferred gains, $238 million

gain was included in accumulated OCI and $601 million gain was included as a basis adjustment of long-term debt at December 31, 2003. As of December 31, 2002, $234 million was included in

accumulated OCI and the remainder was a basis adjustment of long-term debt.