Bank of America 2003 Annual Report Download - page 54

Download and view the complete annual report

Please find page 54 of the 2003 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61

|

|

104 BANK OF AMERICA 2003

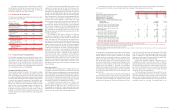

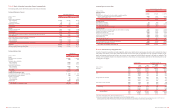

For 2003, 2002 and 2001, net periodic postretirement benefit cost

included the following components:

(Dollars in millions)

2003 2002 2001

Components of net

periodic postretirement

benefit cost (income)

Service cost

$9 $11 $11

Interest cost

68 67 65

Expected return on plan assets

(15) (17) (21)

Amortization of transition obligation

32 32 32

Amortization of prior service cost

464

Recognized net actuarial loss

89 40 20

Net periodic postretirement

benefit cost

$187 $139 $111

Weighted average assumptions

used to determine net cost

for years ended December 31

Discount rate

6.75% 7.25% 7.25%

Expected return on plan assets

8.50 8.50 10.00

Net periodic postretirement health and life expense was determined

using the “projected unit credit” actuarial method. Gains and losses

for all benefits except postretirement health care are recognized in

accordance with the standard amortization provisions of the applica-

ble accounting standards. For the Postretirement Health Care Plans,

50 percent of the unrecognized gain or loss at the beginning of the

fiscal year (or at subsequent remeasurement) is recognized on a level

basis during the year.

Assumed health care cost trend rates affect the postretirement

benefit obligation and benefit cost reported for the Postretirement

Health Care Plans. The assumed health care cost trend rates used

to measure the expected cost of benefits covered by the

Postretirement Health Care Plans was 10 percent for 2004, reducing

in steps to 5 percent in 2007 and later years. A one-percentage-point

increase in assumed health care cost trend rates would have

increased the service and interest costs and the benefit obligation by

$4 million and $52 million, respectively, in 2003, $5 million and $61

million, respectively, in 2002, and $6 million and $52 million, respec-

tively, in 2001. A one-percentage-point decrease in assumed health

care cost trend rates would have lowered the service and interest

costs and the benefit obligation by $3 million and $48 million,

respectively, in 2003, $4 million and $52 million, respectively, in

2002 and $4 million and $45 million, respectively, in 2001.

Plan Assets

The Pension Plan has been established as a retirement vehicle for

participants and a trust has been established to secure benefits

promised under the Pension Plan. The Corporation’s policy is to

invest the trust assets in a prudent manner for the exclusive purpose

of providing benefits to participants and defraying reasonable

expenses of administration. The Corporation’s investment strategy is

designed to provide a total return that, over the long-term, increases

the ratio of assets to liabilities. The strategy attempts to maximize

the investment return on assets at a level of risk deemed appropri-

ate by the Corporation while complying with ERISA and any subse-

quent applicable regulations and laws. The investment strategy

utilizes asset allocation as a principal determinant for establishing

the risk/reward profile of the assets. Asset allocation ranges are

established, periodically reviewed, and adjusted as funding levels and

liability characteristics change. Active and passive investment man-

agers are employed to help enhance the risk/return profile of the

assets. An additional aspect of the investment strategy used to min-

imize risk (part of the asset allocation plan) includes matching the

equity exposure of participant-selected earnings measures. For

example, the common stock of the Corporation invested in the trust

is maintained as an offset to the exposure related to participants

who selected to receive an earnings measure based on the return

performance of common stock of the Corporation.

The Expected Return on Asset Assumption (EROA assumption)

was developed through analysis of historical market returns, historical

asset class volatility and correlations, current market conditions, antic-

ipated future asset allocations, the fund’s past experience, and expec-

tations on potential future market returns. The EROA assumption

BANK OF AMERICA 2003 105

return on plan assets will be 8.50 percent for 2004. The expected return on plan assets is calculated using the calculated market-related value

for the Pension Plan and the fair value for the Postretirement Health and Life Plans. The asset valuation method for the Pension Plan recog-

nizes 60 percent of the market gains or losses in the first year, with the remaining 40 percent spread equally over the next four years.

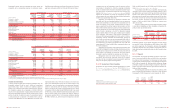

Qualified Nonqualified Postretirement

Pension Plan(1) Pension Plans(1) Health and Life Plans(1)

(Dollars in millions)

2003 2002 2003 2002 2003 2002

Change in fair value of plan assets

(Primarily listed stocks, fixed income and real estate)

Fair value, January 1

$7,518 $8,264 $– $– $181 $194

Actual return on plan assets

1,671 (722) ––25 (13)

Company contributions(2)

400 700 47 39 13 84

Plan participant contributions

––––62 49

Benefits paid

(614) (724) (47) (39) (125) (133)

Fair value, December 31

$8,975 $7,518 $– $– $156 $181

Change in projected benefit obligation

Projected benefit obligation, January 1

$7,627 $7,606 $652 $529 $1,058 $944

Service cost

187 199 25 27 911

Interest cost

514 540 45 44 68 67

Plan participant contributions

––––62 49

Plan amendments

–6–(4) (36) 8

Actuarial loss

714 –37 108 91 112

Effect of curtailments

–––(15) ––

Effect of special termination benefits

–––2––

Benefits paid

(614) (724) (47) (39) (125) (133)

Projected benefit obligation, December 31

$8,428 $7,627 $712 $652 $1,127 $1,058

Funded status, December 31

Accumulated benefit obligation (ABO)

$8,028 $7,264 $628 $573 n/a n/a

Overfunded (unfunded) status of ABO

947 254 (628) (573) n/a n/a

Provision for future salaries

400 363 84 79 n/a n/a

Projected benefit obligation (PBO)

8,428 7,627 712 652 1,127 1,058

Overfunded (unfunded) status of PBO

$547 $(109) $(712) $(652) $(971) $(877)

Unrecognized net actuarial loss

2,153 2,422 195 168 139 147

Unrecognized transition obligation

–––1291 323

Unrecognized prior service cost

364 419 18 21 646

Prepaid (accrued) benefit cost

$3,064 $2,732 $(499) $(462) $(535) $(361)

Weighted average assumptions, December 31

Discount rate

6.25% 6.75% 6.25% 6.75% 6.25% 6.75%

Expected return on plan assets

8.50 8.50 8.50 n/a 8.50 8.50

Rate of compensation increase

4.00 4.00 4.00 4.00 n/a n/a

n/a = not applicable

(1) The measurement date for the Qualified Pension Plan, Nonqualified Pension Plans and Postretirement Health and Life Plans was December 31 of each year reported.

(2) The Corporation’s best estimate of its contributions to be made to the Qualified Pension Plan, Nonqualified Pension Plans and Postretirement Health and Life Plans in 2004 is $0, $64 and $23, respectively.

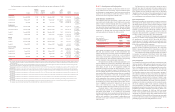

Amounts recognized in the consolidated financial statements at December 31, 2003 and 2002 are as follows:

Qualified Nonqualified Postretirement

Pension Plan Pension Plans Health and Life Plans

(Dollars in millions)

2003 2002 2003 2002 2003 2002

Prepaid benefit cost

$3,064 $2,732 $– $– $– $–

Accrued benefit cost

––(499) (462) (535) (361)

Additional minimum liability

––(129) (111) ––

Intangible asset

––18 22 ––

Accumulated other comprehensive income

––111 89 ––

Net amount recognized at end of year

$3,064 $2,732 $(499) $(462) $(535) $(361)

Net periodic pension benefit cost for 2003, 2002 and 2001 included the following components:

Qualified Pension Plan Nonqualified Pension Plans

(Dollars in millions) 2003 2002 2001 2003 2002 2001

Components of net periodic pension benefit cost (income)

Service cost

$187 $199 $ 202 $25 $27

$22

Interest cost

514 540 560 45 44

40

Expected return on plan assets

(735) (746) (876) ––

–

Amortization of transition asset

––(2) ––

–

Amortization of prior service cost

55 55 54 310

11

Recognized net actuarial loss

47 –– 11 11

7

Recognized loss due to settlements and curtailments

––– –26

6

Net periodic pension benefit cost (income)

$68 $48$(62) $84 $118

$86

Weighted average assumptions used to

determine net cost for years ended December 31

Discount rate

6.75% 7.25% 7.25% 6.75% 7.25%

7.25%

Expected return on plan assets

8.50 8.50 10.00 n/a n/a n/a

Rate of compensation increase

4.00 4.00 4.00 4.00 4.00

4.00

n/a = not applicable