Bank of America 2003 Annual Report Download - page 8

Download and view the complete annual report

Please find page 8 of the 2003 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

|

|

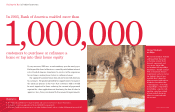

Raising the Bar in Product Innovation

in convenience and speed wouldn’t do

the job for our customers.

We needed to reinvent the mortgage

experience. Seizing the opportunity to

innovate, we created a whole new deliv-

ery process that can eliminate most of

the paperwork and cut waiting time

from days, and sometimes even weeks,

to just minutes. As a result, Bank of

America in 2003 made mortgage loans

and home equity loans to more than

1 million families.

For customers with qualified credit

histories and existing relationships with

the bank, we found ways to eliminate

fully 80% of the paperwork traditionally

associated with mortgage applications,

while remaining within acceptable risk

parameters. More than half of our mort-

gage customers in 2003 used the new,

faster process.

Having cut paperwork, we improved

customer access to our mortgage prod-

ucts and reduced waiting time with an

innovative use of Web-enabled technol-

ogy that we call LoanSolutions.® The

LoanSolutions platform allows Bank of

America associates in our banking

centers to provide a mortgage loan

decision to their customers on the

spot, within minutes, eliminating the

time, uncertainty and cost of obtaining

approval from a central office. This

means customers apply for mortgages

in the same place they are accustomed

to doing the rest of their banking, they

get the type of mortgage that best suits

their particular needs and circum-

stances, and they obtain an answer

right away. In fact, nearly 60% of our

customers who applied for mortgage

financing through LoanSolutions in

2003 received on-the-spot approval.

Because it allows us to sell mort-

gage products in our banking centers,

LoanSolutions expands our ability to

get more mortgage loans to more fam-

ilies in all our communities. It also

enables our associates to assess their

customers’ banking needs and offer

them additional products and services.

Although it might be a while before

we see a mortgage market as robust as

that of 2003, the product and process

improvements we’ve already made will

continue to benefit our customers and

keep us competitive in any interest-

rate environment.

Future enhancements will allow

customers to track their mortgage

loans throughout the fulfillment

process, in real time, from their home

or office computers, in much the same

way many of us track package deliver-

ies today. We’re also looking at ways to

adapt some of the advantages we

designed into our streamlined mort-

gage process so that our customers

can utilize them in applying for and

using credit and debit cards.

12 BANK OF AMERICA 2003 BANK OF AMERICA 2003 13

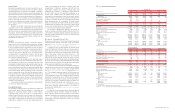

7.2 million

3.24 million

5.7 million

4.7 million

GROWING ACTIVE USERS OF ONLINE BANKING

New Features Bring Added Convenience

The innovative Mini Visa® Credit Card, introduced in 2002, had continued success

in 2003 with the addition of the check card feature. Designed to hang on a key chain,

much like a grocery discount card, the Mini Card is always at hand. It eliminates

the need to pull out a wallet, reach into a handbag, or even carry them. It’s a great

solution for bicyclists, beachgoers, parents carrying infants and anyone who wants

a convenient way to pay. Accounts that have the Mini Card are being used for

purchases more often and carry higher balances.

With Bill-pay

In 2003, active users of our online

banking service passed the 7 million

mark, more than any other bank. And

organizations ranging from Global Finance

magazine to Jupiter Research and Nielsen

ranked our Web site best-in-class.

Our efforts to improve customer

satisfaction resulted in higher growth.

We discovered in 2003 that many

customers who chose to sign up for

online banking were not completing the

enrollment process. Research told us why.

In addressing our customers’ concerns

about security, we had designed online

enrollment to rely on account numbers

and other identifiers. While these

identifiers were less personally sensitive,

they were not always readily available

when customers were at their computers.

As it turned out, customers were

leaving their computers to search for

those identifiers. Often, they never

returned to complete their enrollments.

Interviews revealed that in addition

to security, customers value a simple

enrollment process.

Based on this research, we switched

to identifiers that most consumers have

memorized, and we upgraded our security

procedures while simplifying the process

from five screens to one. As a result, the

enrollment success rate increased 23%,

totalling 100,000 completed enrollments

per month. We also saw our costs go

down because customers didn’t need to

call for help as often.

Then we took the next step and

simplified the online bill payment process,

reducing the number of screen fields by

half, which helped to increase use of the

service by 84% in 2003.

The Best Online

Banking Site Gets

Even Better

1.77 million

2.44 million

December, 2003

June, 2003

December, 2002