Bank of America 2003 Annual Report Download - page 57

Download and view the complete annual report

Please find page 57 of the 2003 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61

|

|

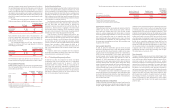

During 2002, the Corporation reached a tax settlement agreement

with the Internal Revenue Service (IRS). This agreement resolved

issues for numerous tax returns of the Corporation and various pred-

ecessor companies and finalized all federal income tax liabilities

through 1999. As a result of the settlement, reductions in income tax

expense of $84 million in 2003 and $488 million in 2002 were

recorded resulting from refunds received and reductions in previously

accrued taxes.

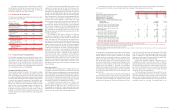

Significant components of the Corporation’s deferred tax liabili-

ties and assets at December 31, 2003 and 2002 were as follows:

December 31

(Dollars in millions)

2003 2002

Deferred tax liabilities

Equipment lease financing

$5,321 $5,767

Intangibles

955 535

Investments

905 700

State taxes

281 310

Depreciation

246 229

Employee retirement benefits

191 250

Deferred gains and losses

189 149

Securities valuation

–350

Available-for-sale debt securities

–266

Other

560 511

Gross deferred tax liabilities

8,648 9,067

Deferred tax assets

Allowance for credit losses

2,421 2,661

Securities valuation

1,876 –

Accrued expenses

421 412

Employee benefits

174 77

Net operating loss carryforwards

129 315

Loan fees and expenses

85 99

Available-for-sale debt securities

46 –

Other

280 212

Gross deferred tax assets

5,432 3,776

Valuation allowance

(120) (114)

Gross deferred tax assets,

net of valuation allowance

5,312 3,662

Net deferred tax liabilities

$3,336 $5,405

The valuation allowance included in the Corporation’s deferred tax

assets at December 31, 2003 and 2002 represented net operating

loss carryforwards for which it is more likely than not that realization

will not occur and expire in 2004 to 2009. The net change in the val-

uation allowance for deferred tax assets resulted from net operating

losses being generated by foreign subsidiaries in 2003 where real-

ization is not expected to occur.

At December 31, 2003 and 2002, federal income taxes had not

been provided on $871 million and $770 million, respectively, of

undistributed earnings of foreign subsidiaries, earned prior to 1987

and after 1997, that have been reinvested for an indefinite period of

time. If the earnings were distributed, an additional $185 million and

$171 million of tax expense, net of credits for foreign taxes paid on

such earnings and for the related foreign withholding taxes, would

result in 2003 and 2002, respectively.

Note 19 Fair Value of Financial Instruments

SFAS No. 107, “Disclosures About Fair Value of Financial

Instruments” (SFAS 107), requires the disclosure of the estimated

fair value of financial instruments. The fair value of a financial instru-

ment is the amount at which the instrument could be exchanged in a

current transaction between willing parties, other than in a forced or

liquidation sale. Quoted market prices, if available, are utilized as

estimates of the fair values of financial instruments. Since no quoted

market prices exist for certain of the Corporation’s financial instru-

ments, the fair values of such instruments have been derived based

on management’s assumptions, the estimated amount and timing of

future cash flows and estimated discount rates. The estimation meth-

ods for individual classifications of financial instruments are

described more fully below. Different assumptions could significantly

affect these estimates. Accordingly, the net realizable values could

be materially different from the estimates presented below. In addi-

tion, the estimates are only indicative of the value of individual finan-

cial instruments and should not be considered an indication of the

fair value of the combined Corporation.

The provisions of SFAS 107 do not require the disclosure of the

fair value of lease financing arrangements and nonfinancial instru-

ments, including intangible assets such as goodwill, franchise, and

credit card and trust relationships.

Short-Term Financial Instruments

The carrying value of short-term financial instruments, including cash

and cash equivalents, time deposits placed, federal funds sold and

purchased, resale and repurchase agreements, commercial paper

and other short-term investments and borrowings, approximates the

fair value of these instruments. These financial instruments generally

expose the Corporation to limited credit risk and have no stated

maturities or have short-term maturities and carry interest rates that

approximate market.

Financial Instruments Traded in the Secondary Market

Held-to-maturity debt securities, available-for-sale debt and mar-

ketable equity securities, trading account instruments and long-term

debt traded actively in the secondary market have been valued using

quoted market prices. The fair values of securities and trading

account instruments are reported in Notes 4 and 5 of the consoli-

dated financial statements.

Derivative Financial Instruments

All derivatives are recognized on the balance sheet at fair value, tak-

ing into consideration the effects of legally enforceable master net-

ting agreements that allow the Corporation to settle positive and

negative positions with the same counterparty on a net basis. For

exchange-traded contracts, fair value is based on quoted market

prices. For non-exchange-traded contracts, fair value is based on

dealer quotes, pricing models or quoted prices for instruments with

similar characteristics. The fair value of the Corporation’s derivative

assets and liabilities is presented in Note 6 of the consolidated finan-

cial statements.

Loans

Fair values were estimated for groups of similar loans based upon

type of loan and maturity. The fair value of loans was determined by

discounting estimated cash flows using interest rates approximating

the Corporation’s current origination rates for similar loans and

adjusted to reflect the inherent credit risk. Where quoted market

prices were available, primarily for certain residential mortgage loans

and commercial loans, such market prices were utilized as estimates

for fair values.

Substantially all of the foreign loans reprice within relatively

short timeframes. Accordingly, for foreign loans, the net carrying val-

ues were assumed to approximate their fair values.

Mortgage Banking Assets

The Certificates are carried at estimated fair value based on an

option-adjusted spread model that requires several key components

including, but not limited to, proprietary prepayment models and term

structure modeling via Monte Carlo simulation.

Deposits

The fair value for deposits with stated maturities was calculated by

discounting contractual cash flows using current market rates for

instruments with similar maturities. The carrying value of foreign time

deposits approximates fair value. For deposits with no stated matu-

rities, the carrying amount was considered to approximate fair value

and does not take into account the significant value of the cost

advantage and stability of the Corporation’s long-term relationships

with depositors.

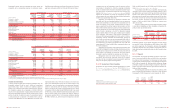

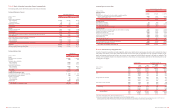

The book and fair values of certain financial instruments at

December 31, 2003 and 2002 were as follows:

December 31

2003 2002

Book Fair Book Fair

(Dollars in millions)

Value Value Value Value

Financial assets

Loans

$353,924 $357,770 $322,065 $330,306

Financial liabilities

Deposits

414,113 414,379 386,458 387,166

Long-term debt(1)

75,343 79,442 61,145 64,935

Trust preferred securities(1)

––6,031 6,263

(1) Long-term debt includes long-term debt related to Trust Securities in 2003.

Note 20 Business Segment Information

The Corporation reports the results of its operations through four

business segments: Consume r and Comme rcial Banking, Asse t

Manage me nt, Global Corporate and Inve stme nt Banking and Equity

Inve stme nts. Certain operating segments have been aggregated into

a single business segment.

Consume r and Comme rcial Banking provides a diversified range

of products and services to individuals and small businesses through

multiple delivery channels. The segment also includes commercial

lending and treasury management services primarily to middle mar-

ket companies with annual revenue between $10 million and $500

million. Asse t Manage me nt offers investment, fiduciary and compre-

hensive banking and credit expertise; asset management services to

institutional clients, high-net-worth individuals and retail customers;

and investment, securities and financial planning services to affluent

and high-net-worth individuals. Glo bal Co rporate and Inve stme nt

Banking provides capital raising solutions, advisory services, deriva-

tives capabilities, equity and debt sales and trading for our corporate,

commercial and institutional clients as well as traditional bank

deposit and loan products, cash management and payment services

to large corporations and institutional clients. Equity Inve stme nts

includes Principal Inve sting,which is comprised of a diversified port-

folio of investments in privately-held and publicly-traded companies at

all stages, from start-up to buyout.

Corporate Othe r consists primarily of certain amounts associ-

ated with the ALM process and certain consumer finance and com-

mercial lending businesses that are being liquidated. Beginning in

the first quarter of 2003, net interest income from certain results

associated with the ALM process was allocated directly to the busi-

ness units. Prior periods have been restated to reflect this change in

methodology. In addition, compensation expense related to stock-

based employee compensation plans is included in Corporate Othe r.

Total revenue includes net interest income on a fully taxable-

equivalent basis and noninterest income. The net interest income of

the business segments includes the results of a funds transfer pric-

ing process that matches assets and liabilities with similar interest

rate sensitivity and maturity characteristics. Net interest income also

reflects an allocation of net interest income generated by assets and

liabilities used in the Corporation’s ALM process.

Segments are allocated provision for credit losses based on

charge-offs and changes in their profile balances and credit risk port-

folio. This adjustment was based on an estimate of the related seg-

ment’s contribution to the improvement in credit quality experienced

by the Corporation.

Certain expenses not directly attributable to a specific business

segment are allocated to the segments based on pre-determined

means. The most significant of these expenses include data pro-

cessing and item processing costs. Data processing costs are allo-

cated to the segments based on equipment usage. Additionally, item

processing costs are allocated to the segments based on the volume

of items processed for each segment.

110 BANK OF AMERICA 2003 BANK OF AMERICA 2003 111