Bank of America 2003 Annual Report Download - page 26

Download and view the complete annual report

Please find page 26 of the 2003 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

|

|

recorded on our balance sheet after the revolving period of the securi-

tization, which has the effect of increasing loans on our balance sheet,

increasing net interest income and increasing charge-offs, with a cor-

responding reduction in noninterest income. Major factors driving the

remaining increase were continued seasoning of outstandings from

new credit card growth over the past two years and economic condi-

tions including higher bankruptcy filings. We expect the trend related to

the impact of the growth of seasoned credit card portfolio to continue.

As a matter of corporate practice, we do not discuss specific

client relationships; however, we have made an exception for two

names due to the publicity and interest surrounding them: Enron

Corporation and its related entities (Enron), and Parmalat. At

December 31, 2003 and 2002, our credit exposure related to Enron

was $102 million and $185 million respectively, of which $81 million

and $150 million was secured. Nonperforming loans related to Enron

were $78 million and $159 million at December 31, 2003 and 2002,

respectively. During 2003 and 2002, we charged off $58 million and

$48 million, respectively, related to Enron. Our credit exposure

related to Parmalat was $274 million and $617 million at December

31, 2003 and 2002, respectively, of which $123 million and $290

million was supported by credit insurance or collateralized by cash.

Our exposure at December 31, 2003 included both loans and deriv-

atives. Direct loans and letters of credit totaling $244 million con-

sisted of loans of $105 million that were supported by credit

insurance and $121 million that were not cash collateralized or credit

insured with specific reserves of $66 million, and undrawn letters of

credit collateralized by cash of $18 million. In addition, our exposure

also included derivatives of $30 million. Nonperforming loans related

to Parmalat were $226 million at December 31, 2003. There were no

nonperforming loans related to Parmalat at December 31, 2002. In

the fourth quarter of 2003, we exercised our contractual rights under

the credit agreements to repay $167 million of loans collateralized by

cash and retained $18 million of cash collateral that secured

undrawn letters of credit. We charged off $114 million of direct loans

that were not cash collateralized or credit insured. In addition, we

marked down the value of our derivatives by 75 percent, or $92 mil-

lion, resulting in the balance of $30 million at December 31, 2003.

Included in Other Assets are loans held for sale and leveraged

lease partnership interests of $8.4 billion and $332 million,

respectively, at December 31, 2003 and $13.8 billion and $387

million, respectively, at December 31, 2002. Included in these bal-

ances are nonperforming loans held for sale and leveraged lease

partnership interests of $199 million and $3 million, respectively,

at December 31, 2003 and $118 million and $2 million, respectively,

at December 31, 2002.

Allowance for Credit Losses

Loans and Le ase s

The allowance for loan and lease losses is allocated to each product

type based on specific and formula components, as well as a general

component. See Note 1 of the consolidated financial statements for

additional discussion on our allowance for credit losses.

The specific component of the allowance for loan and lease

losses covers those commercial loans that are nonperforming or

impaired. An allowance is established when the discounted cash

flows (or collateral value or observable market price) is lower than the

carrying value of that loan. For purposes of computing the specific loss

component of the allowance, larger impaired loans are evaluated

individually and smaller impaired loans are evaluated as a pool using

historical loss experience for the respective product type and risk

rating of the loan.

The formula component of the allocated allowance covers per-

forming commercial loans and leases, and consumer loans. The

allowance for commercial loans is established by product type by ana-

lyzing historical loss experience, by internal risk rating, current eco-

nomic conditions and performance trends within each portfolio

segment. The formula component allowance for consumer loans is

based on aggregated portfolio segment evaluations generally by prod-

uct type. Loss forecast models are utilized for consumer products that

consider a variety of factors including, but not limited to, historical loss

experience, estimated defaults or foreclosures based on portfolio

trends, delinquencies, economic trends and credit scores.

The general component of the allowance for loan and lease

losses is maintained to cover uncertainties that affect our estimate

of probable losses. These uncertainties include the imprecision

inherent in the forecasting methodologies, as well as domestic and

global economic uncertainty, large single name defaults or event risk.

We assess these components, among other current events and con-

ditions, to determine the overall level of the general component. The

relationship of the general component to the total allowance for

credit losses may fluctuate from period to period. We evaluate the

adequacy of the allowance for loan and lease losses based on the

combined total of specific, formula and general components.

We monitor differences between estimated and actual incurred

loan and lease losses. This monitoring process includes periodic

assessments by senior management of loan and lease portfolios and

the models used to estimate incurred losses in those portfolios.

Additions to the allowance for loan and lease losses are made

by charges to the provision. Credit exposures (excluding derivatives)

deemed to be uncollectible are charged against the allowance for

loan and lease losses. Recoveries of previously charged off amounts

are credited to the allowance for loan and lease losses.

Unfunde d Le nding Commitme nts

In addition to the allowance for loan and lease losses, we also com-

pute an estimate of probable losses related to unfunded lending

commitments, such as letters of credit and binding unfunded loan

commitments. This computation is similar to the methodology utilized

in calculating the allowance for commercial loans and leases with

specific, formula and general components, adjusted for the probabil-

ity of drawdown. The reserve for unfunded lending commitments is

included in accrued expenses and other liabilities on the

Consolidated Balance Sheet.

We monitor differences between estimated and actual incurred

credit losses. This monitoring process includes periodic assess-

ments by senior management of credit portfolios and the models

used to estimate incurred losses in those portfolios.

Additions to the reserve for unfunded lending commitments are

made by changes to the provision for unfunded lending commit-

ments. Credit exposures (excluding derivatives) deemed to be uncol-

lectible are charged against the reserve.

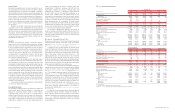

Table 16 presents a rollforward of the allowance for credit losses.

Table 16

Allowance for Credit Losses

(Dollars in millions)

2003 2002

Allowance for loan and lease

losses, January 1

$6,358 $6,278

Loans and leases charged off

Commercial – domestic

(989) (1,793)

Commercial – foreign

(408) (566)

Commercial real estate – domestic

(46) (45)

Total commercial

(1,443) (2,404)

Residential mortgage

(64) (56)

Home equity lines

(38) (40)

Direct/Indirect consumer

(322) (355)

Consumer finance

(280) (333)

Credit card

(1,657) (1,210)

Other consumer domestic

(57) (57)

Foreign consumer

(6) (5)

Total consumer

(2,424) (2,056)

Total loans and leases charged off

(3,867) (4,460)

Recoveries of loans and leases previously

charged off

Commercial – domestic

232 322

Commercial – foreign

102 45

Commercial real estate – domestic

58

Total commercial

339 375

Residential mortgage

24 14

Home equity lines

26 14

Direct/Indirect consumer

141 145

Consumer finance

68 78

Credit card

143 116

Other consumer domestic

19 21

Foreign consumer

1–

Total consumer

422 388

Total recoveries of loans and leases

previously charged off

761 763

Net charge-offs

(3,106) (3,697)

Provision for loan and lease losses

2,916 3,801

Other, net

(5) (24)

Allowance for loan and lease losses,

December 31

$6,163 $6,358

Reserve for unfunded lending commitments,

January 1

$493 $597

Provision for unfunded lending commitments

(77) (104)

Reserve for unfunded lending commitments,

December 31

$416 $493

Total

$6,579 $6,851

Loans and leases outstanding at December 31

$371,463 $342,755

Allowance for loan and lease losses as a

percentage of loans and leases outstanding

at December 31

1.66% 1.85%

Average loans and leases outstanding during

the year

$356,148 $336,819

Net charge-offs as a percentage of average

outstanding loans and leases during the year

0.87% 1.10%

Allowance for loan and lease losses as a

percentage of nonperforming loans at

December 31

215 126

Ratio of allowance for loan and lease losses

at December 31 to net charge-offs

1.98 1.72

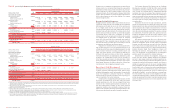

For reporting purposes, we allocate the allowance across products;

however, the allowance is available to absorb all credit losses without

restriction. Table 17 presents our allocation by product type.

Table 17

Allocation of the Allowance for Credit Losses

by Product Type

December 31

2003 2002

(Dollars in millions)

Amount Percent Amount Percent

Allowance for loan

and lease losses

Commercial – domestic

$1,420 21.6% $2,231 32.5%

Commercial – foreign

619 9.4 855 12.5

Commercial real estate

– domestic

404 6.2 430 6.3

Commercial real estate

– foreign

90.1 90.1

Total commercial(1)

2,452 37.3 3,525 51.4

Residential mortgage

149 2.3 108 1.6

Home equity lines

61 0.9 49 0.7

Direct/Indirect consumer

340 5.2 361 5.3

Consumer finance

376 5.7 323 4.7

Credit card

1,602 24.3 1,031 15.1

Foreign consumer

80.1 90.1

Total consumer

2,536 38.5 1,881 27.5

General

1,175 17.9 952 13.9

Allowance for loan

and lease losses

$6,163 93.7% $6,358 92.8%

Reserve for unfunded lending

commitments

Commercial – domestic

$80 1.2% $160 2.3%

Commercial – foreign

60 0.9 32 0.5

Commercial real estate

50.1 90.1

Total commercial

145 2.2 201 2.9

General

271 4.1 292 4.3

Reserve for unfunded

lending commitments

$416 6.3% $493 7.2%

Total

$6,579 100.0% $6,851 100.0%

(1) Includes commercial impaired loans of $391 and $919 at December 31, 2003 and 2002,

respectively.

During the third quarter of 2003, we updated historic loss rate factors

used in estimating the allowance for credit losses to incorporate

more current information.

The allowance for total commercial loan and lease losses

declined $1.1 billion to $2.5 billion as a result of improvement in

credit quality, reflected by the $8.7 billion and $2.1 billion decreases

in commercial criticized exposure and commercial nonperforming

assets; and a $13.9 billion reduction in commercial loans and leases

between December 31, 2003 and December 31, 2002. Specific

reserves on commercial impaired loans decreased $528 million, or

57 percent, in 2003, reflecting a decrease in our investment in

specific loans considered impaired of $1.9 billion to $2.1 billion at

December 31, 2003. The reduction in the levels of impaired loans

and the respective reserves resulted from the overall improvements

in commercial credit quality, loan sales, paydowns and payoffs largely

due to increased refinancings in the capital markets, and net charge-

offs. The allowance for loan and lease losses in the consumer port-

folio increased $655 million from December 31, 2002 due to

portfolio growth, new advances on previously securitized consumer

credit balances, continued seasoning of outstandings from new

consumer credit card growth and economic conditions including

48 BANK OF AMERICA 2003 BANK OF AMERICA 2003 49