Bank of America 2003 Annual Report Download - page 16

Download and view the complete annual report

Please find page 16 of the 2003 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

|

|

BANK OF AMERICA 2003 29

Supplemental Financial Data

In managing our business, we use certain performance measures

and ratios not defined in accounting principles generally accepted in

the United States (GAAP), including financial information on an oper-

ating basis and shareholder value added (SVA). We also calculate

certain measures, such as net interest income, core net interest

income, net interest yield and the efficiency ratio, on a fully taxable-

equivalent basis. Other companies may define or calculate supple-

mental financial data differently. See Table 2 for supplemental

financial data and corresponding reconciliations to GAAP financial

measures for the five most recent years.

Supplemental financial data presented on an operating basis is

a basis of presentation not defined by GAAP that excludes exit, and

merger and restructuring charges. Table 2 includes earnings, earn-

ings per common share (EPS), SVA, return on average assets, return

on average equity, efficiency ratio and dividend payout ratio presented

on an operating basis. We believe that the exclusion of the exit, and

merger and restructuring charges, which represent events outside of

our normal operations, provides a meaningful period-to-period com-

parison and is more reflective of normalized operations.

SVA is a key measure of performance not defined by GAAP,that

is used in managing our growth strategy orientation and strengthen-

ing our focus on generating long-term growth and shareholder value.

SVA is used in measuring the performance of our different business

units and is an integral component for allocating resources. Each

business segment has a goal for growth in SVA reflecting the individ-

ual segment’s business and customer strategy. Investment resources

and initiatives are aligned with these SVA growth goals during the

planning and forecasting process. Investment, relationship and prof-

itability models all have SVA as a key measure to support the imple-

mentation of SVA growth goals. SVA is defined as cash basis

earnings on an operating basis less a charge for the use of capital.

Cash basis earnings is defined as net income adjusted to exclude

amortization of intangibles. The charge for the use of capital is cal-

culated by multiplying 11 percent (management’s estimate of the

shareholders’ minimum required rate of return on capital invested) by

average total common shareholders’ equity at the corporate level and

by average allocated equity at the business segment level. Equity is

allocated to the business segments using a risk-adjusted methodol-

ogy for each segment’s credit, market and operational risks. The

nature of these risks is discussed further beginning on page 44. SVA

increased 49 percent to $5.6 billion for 2003 compared to 2002, due

to both the $1.6 billion increase in cash basis earnings and the $491

million effect of the decrease in the capital charge, which was driven

by a reduction in management’s estimate of the rate used to calcu-

late the charge for the use of capital from 12 percent to 11 percent

in 2003. For additional discussion of SVA, see Business Segment

Operations beginning on page 32.

We review net interest income on a fully taxable-equivalent

basis, which is a performance measure used by management in oper-

ating the business that we believe provides investors with a more

accurate picture of the interest margin for comparative purposes. In

this presentation, net interest income is adjusted to reflect tax-

exempt interest income on an equivalent before-tax basis. For pur-

poses of this calculation, we use the federal statutory tax rate of 35

percent. This measure ensures comparability of net interest income

arising from both taxable and tax-exempt sources. Net interest

income on a fully taxable-equivalent basis is also used in the calcu-

lation of the efficiency ratio and the net interest yield. The efficiency

ratio, which is calculated by dividing noninterest expense by total rev-

enue, measures how much it costs to produce one dollar of revenue.

Net interest income on a fully taxable-equivalent basis is also used

in our business segment reporting.

Additionally, we review “core net interest income,” which adjusts

reported net interest income on a fully taxable-equivalent basis for the

impact of Global Corporate and Inve stme nt Banking trading-related

activities and loans that we originated and sold into revolving credit

card and commercial securitizations. Noninterest income, rather than

net interest income and provision for credit losses, is recorded for

assets that have been securitized as we are compensated for servic-

ing the securitized assets and record servicing income and gains or

losses on securitizations, where appropriate. We evaluate our trading

results by combining trading-related net interest income with trading

account profits, as discussed in the Global Corporate and Inve stme nt

Banking business segment section beginning on page 36, as trading

strategies are evaluated based on total revenue.

Core net interest income increased $147 million in 2003. This

increase was driven by higher ALM portfolio levels, consumer loan lev-

els, higher mortgage warehouse and core deposit funding levels.

These increases were partially offset by the impact of lower interest

rates and reductions in the large corporate, foreign and exited con-

sumer loan portfolios.

Core average earning assets increased $24.7 billion in 2003,

driven by the $29.9 billion increase in residential mortgages related

to ALM activities during the year and the $6.8 billion increase in credit

card outstandings, which includes $2.6 billion of new advances under

previously securitized balances that are recorded on our balance

sheet, after the revolving period of the securitization, partially offset by

the $16.0 billion decrease in the overall commercial loan portfolio.

The core net interest yield decreased 19 bps in 2003, mainly due

to the results of our ALM process partially offset by consumer loan

growth, primarily credit cards, that was experienced throughout the year.

28 BANK OF AMERICA 2003

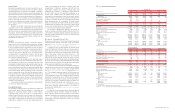

Table 2

Supplemental Financial Data and Reconciliations to GAAP Financial Measures

(Dollars in millions, except per share information) 2003 2002 2001 2000 1999

Operating basis(1,2)

Operating earnings

$10,810 $9,249 $ 8,042 $ 7,863 $ 8,240

Operating earnings per common share

7.27 6.08 5.04 4.77 4.77

Diluted operating earnings per common share

7.13 5.91 4.95 4.72 4.68

Shareholder value added

5,621 3,760 3,087 3,081 3,544

Return on average assets

1.41% 1.40% 1.24% 1.17% 1.34%

Return on average common shareholders’ equity

21.99 19.44 16.53 16.70 17.70

Efficiency ratio (fully taxable-equivalent basis)

52.23 52.55 55.47 54.38 55.30

Dividend payout ratio

39.58 40.07 45.13 43.04 38.77

Net interest income

Fully taxable-equivalent basis data

Net interest income

$22,107 $21,511 $ 20,633 $ 18,671 $ 18,342

Total revenue

38,529 35,082 34,981 33,253 32,521

Net interest yield

3.36% 3.75% 3.68% 3.20% 3.45%

Efficiency ratio

52.23 52.55 59.20 56.03 56.92

Core basis data

Core net interest income

$20,205 $20,058 $ 19,719 $ 18,546 $ 18,583

Core average earning assets

478,815 454,157 468,317 506,898 472,329

Core net interest yield

4.22% 4.41% 4.21% 3.66% 3.93%

Reconciliation of net income to operating earnings

Net income

$10,810 $9,249 $ 6,792 $ 7,517 $ 7,882

Exit charges

––1,700 – –

Merger and restructuring charges

–––550 525

Related income tax benefit

––(450) (204) (167)

Operating earnings

$10,810 $9,249 $ 8,042 $ 7,863 $ 8,240

Reconciliation of EPS to operating EPS

Earnings per common share

$7.27 $6.08 $ 4.26 $ 4.56 $ 4.56

Exit charges, net of tax benefit

––0.78 – –

Merger and restructuring charges, net of tax benefit

–––0.21 0.21

Operating earnings per common share

$7.27 $6.08 $ 5.04 $ 4.77 $ 4.77

Reconciliation of diluted EPS to diluted operating EPS

Diluted earnings per common share

$7.13 $5.91 $ 4.18 $ 4.52 $ 4.48

Exit charges, net of tax benefit

––0.77 – –

Merger and restructuring charges, net of tax benefit

–––0.20 0.20

Diluted operating earnings per common share

$7.13 $5.91 $ 4.95 $ 4.72 $ 4.68

Reconciliation of net income to shareholder value added

Net income

$10,810 $9,249 $ 6,792 $ 7,517 $ 7,882

Amortization of intangibles

217 218 878 864 888

Exit charges, net of tax benefit

––1,250 – –

Merger and restructuring charges, net of tax benefit

–––346 358

Cash basis earnings on an operating basis

11,027 9,467 8,920 8,727 9,128

Capital charge

(5,406) (5,707) (5,833) (5,646) (5,584)

Shareholder value added

$5,621 $3,760 $ 3,087 $ 3,081 $ 3,544

Reconciliation of return on average assets to operating

return on average assets

Return on average assets

1.41% 1.40% 1.05% 1.12% 1.28%

Effect of exit charges, net of tax benefit

––0.19 – –

Effect of merger and restructuring charges, net of tax benefit

–––0.05 0.06

Operating return on average assets

1.41% 1.40% 1.24% 1.17% 1.34%

Reconciliation of return on average common shareholders’ equity

to operating return on average common shareholders’ equity

Return on average common shareholders’ equity

21.99% 19.44% 13.96% 15.96% 16.93%

Effect of exit charges, net of tax benefit

––2.57 – –

Effect of merger and restructuring charges, net of tax benefit

–––0.74 0.77

Operating return on average common shareholders’ equity

21.99% 19.44% 16.53% 16.70% 17.70%

Reconciliation of efficiency ratio to operating efficiency ratio

(fully taxable-equivalent basis)

Efficiency ratio

52.23% 52.55% 59.20% 56.03% 56.92%

Effect of exit charges, net of tax benefit

––(3.73) – –

Effect of merger and restructuring charges, net of tax benefit

–––(1.65) (1.62)

Operating efficiency ratio

52.23% 52.55% 55.47% 54.38% 55.30%

Reconciliation of dividend payout ratio to operating dividend payout ratio

Dividend payout ratio

39.58% 40.07% 53.44% 45.02% 40.54%

Effect of exit charges, net of tax benefit

––(8.31) – –

Effect of merger and restructuring charges, net of tax benefit

–––(1.98) (1.77)

Operating dividend payout ratio

39.58% 40.07% 45.13% 43.04% 38.77%

(1) Operating basis excludes exit, and merger and restructuring charges. Exit charges in 2001 represented provision for credit losses of $395 and noninterest expense of $1,305, both of which were related

to the exit of certain consumer finance businesses. Merger and restructuring charges were $550 and $525 in 2000 and 1999, respectively.

(2) As a result of the adoption of SFAS 142 on January 1, 2002, we no longer amortize goodwill. Goodwill amortization expense was $662, $635 and $635 in 2001, 2000 and 1999, respectively.