Humana 2006 Annual Report Download - page 104

Download and view the complete annual report

Please find page 104 of the 2006 Humana annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

|

|

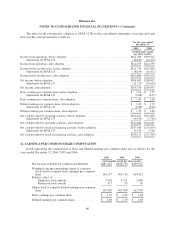

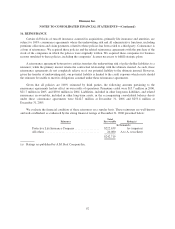

Humana Inc.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

16. REINSURANCE

Certain old blocks of run-off insurance assumed in acquisitions, primarily life insurance and annuities, are

subject to 100% coinsurance agreements where the underwriting risk and all administrative functions, including

premium collections and claim payments, related to these policies has been ceded to a third-party. Coinsurance is

a form of reinsurance. We acquired these policies and the related reinsurance agreements with the purchase of the

stock of the companies in which the policies were originally written. We acquired these companies for business

reasons unrelated to these policies, including the companies’ licenses necessary to fulfill strategic plans.

A reinsurance agreement between two entities transfers the underwriting risk of policyholder liabilities to a

reinsurer; while the primary insurer retains the contractual relationship with the ultimate insured. As such, these

reinsurance agreements do not completely relieve us of our potential liability to the ultimate insured. However,

given the transfer of underwriting risk, our potential liability is limited to the credit exposure which exists should

the reinsurer be unable to meet its obligations assumed under these reinsurance agreements.

Given that all policies are 100% reinsured by third parties, the following amounts pertaining to the

reinsurance agreements had no effect on our results of operations. Premiums ceded were $15.7 million in 2006,

$21.7 million in 2005, and $30.0 million in 2004. Liabilities, included in other long-term liabilities, and related

reinsurance recoverables, included in other long-term assets, in the accompanying consolidated balance sheets

under these coinsurance agreements were $242.7 million at December 31, 2006 and $253.4 million at

December 31, 2005.

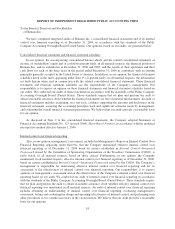

We evaluate the financial condition of these reinsurers on a regular basis. These reinsurers are well-known

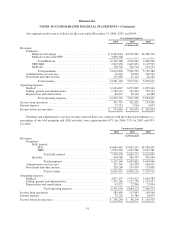

and well-established, as evidenced by the strong financial ratings at December 31, 2006 presented below:

Reinsurer

Total

Recoverable Rating(a)

(in thousands)

Protective Life Insurance Company ................. $222,639 A+ (superior)

All others ..................................... 20,080 A to A- (excellent)

$242,719

(a) Ratings are published by A.M. Best Company Inc.

92