Humana 2006 Annual Report Download - page 81

Download and view the complete annual report

Please find page 81 of the 2006 Humana annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

|

|

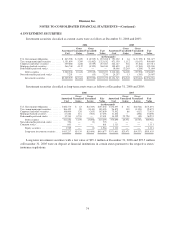

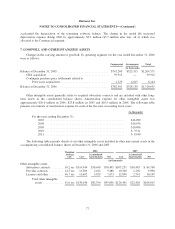

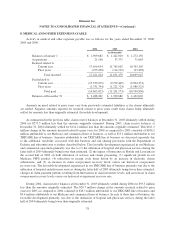

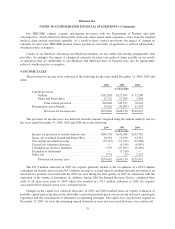

Humana Inc.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

Other Revenue

Other revenues primarily relate to an in-house mail order pharmacy operation. These revenues are

recognized in connection with the shipment of the prescriptions.

Policy Acquisition Costs

Policy acquisition costs are those costs that vary with and primarily are related to the acquisition of new and

renewal business. Such costs include broker commissions, costs of policy issuance and underwriting, and other

costs we incur to acquire new business or renew existing business. We expense policy acquisition costs related to

our employer-group prepaid health services policies as incurred in accordance with the Health Care

Organization Audit and Accounting Guide. These short-duration employer-group prepaid health services policies

typically have a one-year term and may be cancelled upon 30 days notice by the employer group.

Our health and life policies sold to individuals, when aggregated as a block of policies, are expected to

remain in force for an extended period beyond one year because, by law, these contracts are guaranteed

renewable. Accordingly, we account for these policies as long-duration insurance products under the provisions

of SFAS No. 60, Accounting and Reporting by Insurance Enterprises, or SFAS 60.As a result, we defer policy

acquisition costs and amortize them over the estimated life of the policies in proportion to premiums earned.

Deferred acquisition costs are regularly reviewed to determine if they are recoverable from future income.

Long-Lived Assets

Property and equipment is recorded at cost. Gains and losses on sales or disposals of property and

equipment are included in administrative expense. Certain costs related to the development or purchase of

internal-use software are capitalized in accordance with AICPA Statement of Position 98-1, Accounting for the

Costs of Computer Software Developed or Obtained for Internal Use. Depreciation is computed using the

straight-line method over estimated useful lives ranging from 3 to 10 years for equipment, 3 to 7 years for

computer software, and 20 to 40 years for buildings. Improvements to leased facilities are depreciated over the

shorter of the remaining lease term or the anticipated life of the improvement.

We periodically review long-lived assets, including property and equipment and other intangible assets, for

impairment whenever adverse events or changes in circumstances indicate the carrying value of the asset may not

be recoverable. Losses are recognized for a long-lived asset to be held and used in our operations when the

undiscounted future cash flows expected to result from the use of the asset are less than its carrying value. We

recognize an impairment loss based on the excess of the carrying value over the fair value of the asset. A long-

lived asset held for sale is reported at the lower of the carrying amount or fair value less costs to sell.

Depreciation expense is not recognized on assets held for sale. Losses are recognized for a long-lived asset to be

abandoned when the asset ceases to be used. In addition, we periodically review the estimated lives of all long-

lived assets for reasonableness.

Goodwill and Other Intangible Assets

Goodwill represents the unamortized excess of cost over the fair value of the net tangible and other

intangible assets acquired. SFAS No. 142, Goodwill and Other Intangible Assets, or SFAS 142, requires that we

not amortize goodwill to earnings, but instead requires that we test at least annually for impairment at a level of

reporting referred to as the reporting unit and more frequently if adverse events or changes in circumstances

indicate that the asset may be impaired. A reporting unit is one level below our Commercial and Government

segments. The Commercial segment’s two reporting units consist of medical (fully and self insured) and

69