Humana 2006 Annual Report Download - page 44

Download and view the complete annual report

Please find page 44 of the 2006 Humana annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

|

|

premium, ASO fee, and plan benefit levels that are commensurate with our medical and administrative costs.

Medical costs are subject to a high rate of inflation due to many forces, including new higher priced technologies

and medical procedures, increasing capacity and supply of medical services, new prescription drugs and

therapies, an aging population, lifestyle challenges including obesity and smoking, the tort liability system, and

government regulations.

Our industry relies on two key statistics to measure performance. MER, which is computed by taking total

medical expenses as a percentage of premium revenues, represents a statistic used to measure underwriting

profitability. The SG&A expense ratio, which is computed by taking total selling, general and administrative

expenses as a percentage of premium revenues and administrative services fees, represents a statistic used to

measure administrative spending efficiency.

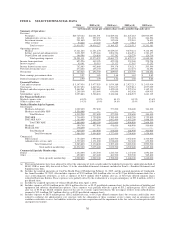

Government Segment

Our strategy and commitment to the expanded Medicare programs, including new product choices and

pharmacy benefits for seniors, led to substantial growth during 2006. Medicare Advantage membership increased

to 1,002,600 members at December 31, 2006, up 79.7% from 557,800 members at December 31, 2005, primarily

due to sales of our PFFS product. Our new Medicare stand-alone PDP products added 3,536,600 members during

2006. Medicare premium revenues more than doubled to $11.5 billion during 2006 primarily as a result of this

membership growth.

Pretax earnings in the Government segment of $513.8 million in 2006 were 62% higher than 2005. This

increase resulted primarily from the membership and associated revenue growth in our Medicare Advantage

plans, partially offset by results for the new Medicare stand-alone PDP offerings. Our Complete stand-alone PDP

offering, one of three stand-alone PDP offerings representing 12% of our stand-alone PDP membership, operated

at a loss with a MER of 116% in 2006. The reason for the operating loss primarily related to the product’s design,

including covering brand name prescription drugs in the coverage gap. The coverage gap represents the stage of

coverage where the member would be responsible for the cost under a standard plan. The Complete stand-alone

PDP offering was re-designed for 2007.

In addition, the new stand-alone PDP benefit designs impacted our quarterly earnings pattern. These benefit

designs result in coverage that varies as a member’s cumulative out-of-pocket costs pass through successive

stages of a member’s plan period as specified under the standard plan defined by CMS. These plan designs

generally result in us sharing a greater portion of the responsibility for total pharmacy costs in the early stages of

a member’s plan period and less in the later stages for the plans which comprise the majority of our membership.

This generally produces results that improve as the year progresses. For example, during 2006 our Standard and

Enhanced stand-alone PDP offerings resulted in an MER of 97.7% during the first quarter, improving to 74.7%

during the fourth quarter.

Commercial Segment

Commercial segment medical membership increased 113,000 members, or 3.6% from December 31, 2005

to 3,283,800 at December 31, 2006 as a result of the May 1, 2006 CHA acquisition which added 88,400 members

and higher ASO, individual and consumer-choice membership, partially offset by a decline in our fully insured

group membership. ASO membership at December 31, 2006 was up 31% from December 31, 2005. Individual

membership increased 15% and consumer-choice membership increased 13% during 2006. These three areas,

together with our small group business, now represent more than 84% of our Commercial medical membership.

Other Highlights

• Year over year comparisons have been impacted by litigation and Hurricane Katrina expenses in 2005

that did not recur in 2006, as more fully discussed in the next section.

32