Humana 2006 Annual Report Download - page 91

Download and view the complete annual report

Please find page 91 of the 2006 Humana annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

|

|

Humana Inc.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

Our TRICARE contract contains risk-sharing provisions with the Department of Defense and with

subcontractors, which effectively limit profits and losses when actual claim experience varies from the targeted

medical claim amount negotiated annually. As a result of these contract provisions, the impact of changes in

estimates for prior year TRICARE medical claims payable on our results of operations is reduced substantially,

whether positive or negative.

Certain of our Medicare Advantage and Medicaid members are also under risk-sharing arrangements with

providers. Accordingly, the impact of changes in estimates for prior year medical claims payable on our results

of operations that are attributable to our Medicare and Medicaid lines of business may also be significantly

reduced, whether positive or negative.

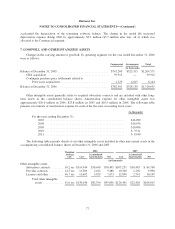

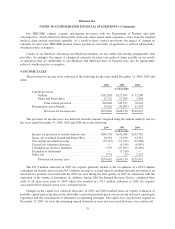

9. INCOME TAXES

The provision for income taxes consisted of the following for the years ended December 31, 2006, 2005 and

2004:

2006 2005 2004

(in thousands)

Current provision:

Federal ................................. $192,878 $127,653 $ 73,280

States and Puerto Rico ..................... 11,722 17,504 3,644

Total current provision ................. 204,600 145,157 76,924

Deferred provision (benefit) ..................... 70,062 (39,007) 52,507

Provision for income taxes .............. $274,662 $106,150 $129,431

The provision for income taxes was different from the amount computed using the federal statutory rate for

the years ended December 31, 2006, 2005 and 2004 due to the following:

2006 2005 2004

(in thousands)

Income tax provision at federal statutory rate ....... $266,730 $141,008 $139,782

States, net of federal benefit and Puerto Rico ....... 18,301 13,169 13,361

Tax exempt investment income .................. (15,713) (11,917) (12,700)

Capital loss valuation allowance ................. — (5,198) (6,855)

Contingent tax reserves (benefits) ................ 1,570 (27,365) (6,409)

Examination settlements ....................... — (3,518) —

Other, net ................................... 3,774 (29) 2,252

Provision for income taxes .................. $274,662 $106,150 $129,431

The $27.4 million reduction in 2005 tax expense primarily related to the recognition of a $22.8 million

contingent tax benefit and associated $3.1 million reversal of accrued interest resulting from the resolution of an

uncertain tax position associated with the 2000 tax year during the first quarter of 2005 in connection with the

expiration of the statute of limitations. In addition, during 2005 the Internal Revenue Service completed their

audit of all open years prior to 2003 which also resulted in a $3.5 million reduction in 2005 tax expense

associated with revisions to prior year’s estimated taxes.

Changes in the capital loss valuation allowance in 2005 and 2004 resulted from our regular evaluation of

probable capital gain realization in the allowable carryforward period given our recent and historical capital gain

experience and the consideration of alternative tax planning strategies. The capital loss carryforward expired on

December 31, 2005. As such, the remaining unused deferred tax asset and associated allowance were written off.

79