Humana 2006 Annual Report Download - page 64

Download and view the complete annual report

Please find page 64 of the 2006 Humana annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

|

|

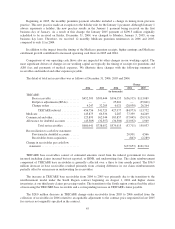

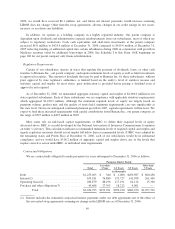

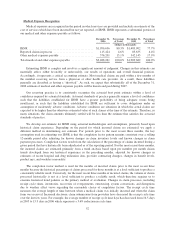

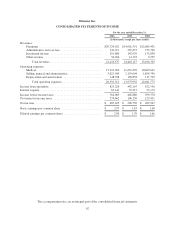

Medical Expense Recognition

Medical expenses are recognized in the period in which services are provided and include an estimate of the

cost of services which have been incurred but not yet reported, or IBNR. IBNR represents a substantial portion of

our medical and other expenses payable as follows:

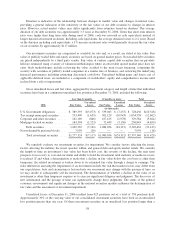

December 31,

2006

Percentage

of Total

December 31,

2005

Percentage

of Total

(dollars in thousands)

IBNR ............................................ $1,996,636 80.3% $1,483,902 77.7%

Reported claims in process ........................... 115,424 4.6% 83,635 4.4%

Other medical expenses payable ....................... 376,201 15.1% 342,145 17.9%

Total medical and other expenses payable ............... $2,488,261 100.0% $1,909,682 100.0%

Estimating IBNR is complex and involves a significant amount of judgment. Changes in this estimate can

materially affect, either favorably or unfavorably, our results of operations and overall financial position.

Accordingly, it represents a critical accounting estimate. Most medical claims are paid within a few months of

the member receiving service from a physician or other health care provider. As a result, these liabilities

generally are described as having a “short-tail”. As such, we expect that substantially all of the December 31,

2006 estimate of medical and other expenses payable will be known and paid during 2007.

Our reserving practice is to consistently recognize the actuarial best point estimate within a level of

confidence required by actuarial standards. Actuarial standards of practice generally require a level of confidence

such that the liabilities established for IBNR have a greater probability of being adequate versus being

insufficient, or such that the liabilities established for IBNR are sufficient to cover obligations under an

assumption of moderately adverse conditions. Adverse conditions are situations in which the actual claims are

expected to be higher than the otherwise estimated value of such claims at the time of the estimate. Therefore, in

many situations, the claim amounts ultimately settled will be less than the estimate that satisfies the actuarial

standards of practice.

We develop our estimate for IBNR using actuarial methodologies and assumptions, primarily based upon

historical claim experience. Depending on the period for which incurred claims are estimated, we apply a

different method in determining our estimate. For periods prior to the most recent three months, the key

assumption used in estimating our IBNR is that the completion factor pattern remains consistent over a rolling

12-month period after adjusting for known changes in claim inventory levels and known changes in claim

payment processes. Completion factors result from the calculation of the percentage of claims incurred during a

given period that have historically been adjudicated as of the reporting period. For the most recent three months,

the incurred claims are estimated primarily from a trend analysis based upon per member per month claims

trends developed from our historical experience in the preceding months, adjusted for known changes in

estimates of recent hospital and drug utilization data, provider contracting changes, changes in benefit levels,

product mix, and weekday seasonality.

The completion factor method is used for the months of incurred claims prior to the most recent three

months because the historical percentage of claims processed for those months is at a level sufficient to produce a

consistently reliable result. Conversely, for the most recent three months of incurred claims, the volume of claims

processed historically is not at a level sufficient to produce a reliable result, which therefore requires us to

examine historical trend patterns as the primary method of evaluation. Changes in claim processes, including

receipt cycle times, inventories, recoveries of overpayments, outsourcing, system conversions, and disruptions

due to weather affect views regarding the reasonable choice of completion factors. The receipt cycle time

measures the average length of time between when a medical claim was initially incurred and when the claim

form was received. Increased electronic claim submissions from providers have decreased the receipt cycle time

over the last few years. For example, the average number of receipt cycle time days has decreased from 16.5 days

in 2005 to 15.9 days in 2006 which represents a 3.6% reduction in cycle time.

52