Humana 2009 Annual Report Download - page 90

Download and view the complete annual report

Please find page 90 of the 2009 Humana annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

|

|

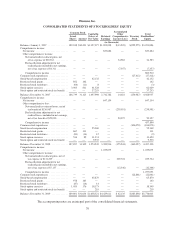

Humana Inc.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

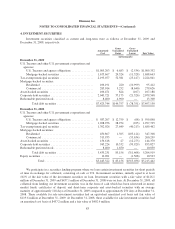

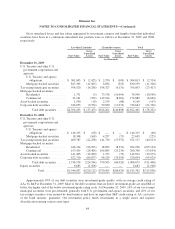

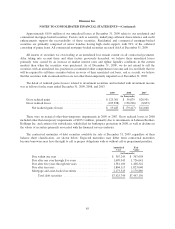

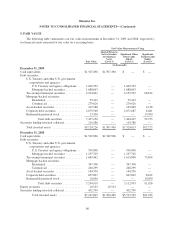

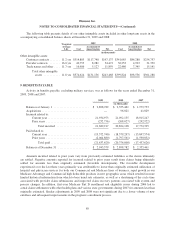

term of the assets or liabilities. Level 2 assets and liabilities include debt securities with quoted prices that

are traded less frequently than exchange-traded instruments as well as debt securities and derivative

contracts whose value is determined using a pricing model with inputs that are observable in the market or

can be derived principally from or corroborated by observable market data.

Level 3—Unobservable inputs that are supported by little or no market activity and are significant to the fair

value of the assets or liabilities. Level 3 includes assets and liabilities whose value is determined using

pricing models, discounted cash flow methodologies, or similar techniques reflecting our own assumptions

about the assumptions market participants would use as well as those requiring significant management

judgment.

Fair value of actively traded debt and equity securities are based on quoted market prices. Fair value of

other debt securities are based on quoted market prices of identical or similar securities or based on observable

inputs like interest rates using either a market or income valuation approach and are generally classified as Level

2. Fair value of privately held debt securities, including venture capital investments, as well as auction rate

securities, are estimated using a variety of valuation methodologies, including both market and income

approaches, where an observable quoted market does not exist and are generally classified as Level 3. For

privately held debt securities, such methodologies include reviewing the value ascribed to the most recent

financing, comparing the security with securities of publicly traded companies in similar lines of business, and

reviewing the underlying financial performance including estimating discounted cash flows. For auction rate

securities, such methodologies include consideration of the quality of the sector and issuer, underlying collateral,

underlying final maturity dates and liquidity.

Recently Issued Accounting Pronouncements

In June 2009, the FASB codified existing accounting standards. The FASB Accounting Standards

CodificationTM, or ASC, is the source of authoritative U.S. generally accepted accounting principles recognized

by the FASB and supersedes all existing non-SEC accounting and reporting standards. All ASC content carries

the same level of authority and anything outside of the ASC is nonauthoritative. We adopted the new guidance in

2009, which changed the way we reference accounting standards in our disclosures.

In January 2010, the FASB issued new guidance that expands and clarifies existing disclosures about fair

value measurements. Under the new guidance, we will be required to disclose information about movements of

assets among Levels 1 and 2 of the three-tier fair value hierarchy and present separately (that is on a gross basis)

information about purchases, sales, issuances, and settlements of financial instruments in the reconciliation of

fair value measurements using significant unobservable inputs (Level 3). In addition, the new guidance clarified

that we are required to provide fair value measurement disclosures for each class of financial assets and liabilities

and provide disclosures about inputs and valuation techniques for fair value measurements in either Level 2 or

Level 3. These new disclosures and clarifications are effective for us beginning with the filing of our Form 10-Q

for the three months ended March 31, 2010, except for the gross disclosures regarding purchases, sales, issuances

and settlements in the roll forward of activity in Level 3 fair value measurements. Those disclosures are effective

for us beginning with the filing of our Form 10-Q for the three months ended March 31, 2011.

Subsequent Events

We have evaluated subsequent events for recognition or disclosure through February 19, 2010, the date

these consolidated financial statements were issued.

80