Nike 2010 Annual Report Download - page 36

Download and view the complete annual report

Please find page 36 of the 2010 Nike annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

|

|

Table of Contents

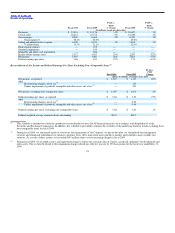

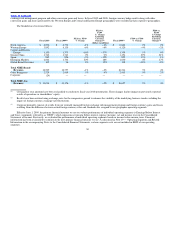

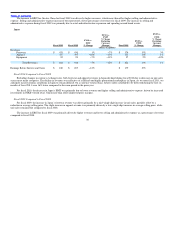

throughout the geography. Excluding changes in currency exchange rates, futures orders scheduled for delivery during the first six months of fiscal 2011

were 11% higher compared to the same period in the prior year, driven by strong growth across most markets and product categories.

Excluding changes in currency exchange rates, the decrease in footwear revenue during fiscal 2010 was primarily the result of low single−digit

decreases in both average selling price and unit sales. The decrease in average selling price was attributable to higher customer discounts provided to

manage inventory levels, while the reduction in unit sales was due to lower sales for most NIKE Brand product categories.

The year−over−year decrease in apparel revenue was primarily driven by a high single−digit decline in unit sales combined with a mid single−digit

decrease in average selling price. The decrease in unit sales was due to lower sales for most NIKE Brand product categories, while the decrease in average

selling price was a result of higher discounts provided to retailers to manage their inventory levels.

For fiscal 2010, EBIT for Western Europe declined at a faster rate than revenues, as the increase in selling and administrative expense as a percentage

of revenues more than offset the improvements in gross margin percentage. The increase in selling administrative expense was primarily driven by a higher

level of both demand creation spending around the 2010 World Cup and operating overhead expense as a result of investments in NIKE−owned retail and

higher performance−based compensation. The gross margin improvement in fiscal 2010 was primarily attributable to higher in−line product margins, a

smaller proportion of close−out sales and reduced inventory obsolescence expense as a result of our leaner inventory positions.

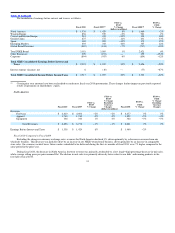

Fiscal 2009 Compared to Fiscal 2008

Excluding changes in currency exchange rates, a number of markets within the geography experienced lower revenues, reflecting a more difficult

retail environment. Revenues for the Southern European markets, including Spain, Italy and France declined, while the U.K. & Ireland remained flat

compared to the same period in the prior year.

The increase in footwear revenue was attributable to a low single−digit growth in unit sales. The growth in unit sales was driven primarily by higher

demand for kids and NIKE Brand sportswear products. Average selling price per pair remained flat compared to the prior year.

The decrease in apparel revenue was primarily driven by lower average selling prices resulting from a higher mix of close−out sales and higher levels

of discounts provided to retailers to manage inventory levels, which more than offset a low−single−digit increase in unit sales.

The year−over−year increase in EBIT for the Western Europe geography during fiscal 2009 was primarily driven by a higher gross margin

percentage, partially offset by slightly higher selling and administrative expense as a percentage of revenues. The gross margin improvement in fiscal 2009

was primarily attributable to improved year−over−year standard currency rates which more than offset higher warehousing costs and discounts on in−line

products. The increase in selling and administrative expense as a percentage of revenues was mainly driven by retail expansion across the geography.

33