Nike 2010 Annual Report Download - page 77

Download and view the complete annual report

Please find page 77 of the 2010 Nike annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

|

|

Table of Contents NIKE, INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS — (Continued)

As of May 31, 2010, the Company had no amounts outstanding under its commercial paper program. As of May 31, 2009, the Company had $100.0

million outstanding at a weighted average interest rate of 0.40%.

In December 2006, the Company entered into a $1 billion revolving credit facility with a group of banks. The facility matures in December 2012.

Based on the Company’s current long−term senior unsecured debt ratings of A+ and A1 from Standard and Poor’s Corporation and Moody’s Investor

Services, respectively, the interest rate charged on any outstanding borrowings would be the prevailing LIBOR plus 0.15%. The facility fee is 0.05% of the

total commitment. Under this agreement, the Company must maintain, among other things, certain minimum specified financial ratios with which the

Company was in compliance at May 31, 2010. No amounts were outstanding under this facility as of May 31, 2010 and 2009.

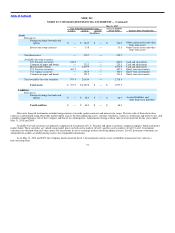

Note 8 — Long−Term Debt

Long−term debt, net of unamortized premiums and discounts and swap fair value adjustments, is comprised of the following:

May 31,

2010 2009

(In millions)

5.375% Corporate bond, payable July 8, 2009 $ — $ 25.1

5.66% Corporate bond, payable July 23, 2012 27.0 27.4

5.4% Corporate bond, payable August 7, 2012 16.1 16.2

4.7% Corporate bond, payable October 1, 2013 50.0 50.0

5.15% Corporate bond, payable October 15, 2015 112.4 111.1

4.3% Japanese Yen note, payable June 26, 2011 115.7 108.5

1.52125% Japanese Yen note, payable February 14, 2012 55.1 51.7

2.6% Japanese Yen note, maturing August 20, 2001 through November 20, 2020 53.1 54.7

2.0% Japanese Yen note, maturing August 20, 2001 through November 20, 2020 23.8 24.5

Total 453.2 469.2

Less current maturities 7.4 32.0

$445.8 $437.2

The scheduled maturity of long−term debt in each of the years ending May 31, 2011 through 2015 are $7.4 million, $178.1 million, $47.4 million,

$57.4 million and $7.4 million, at face value, respectively.

The Company’s long−term debt is recorded at adjusted cost, net of amortized premiums and discounts and interest rate swap fair value adjustments.

The fair value of long−term debt is estimated based upon quoted prices for similar instruments. The fair value of the Company’s long−term debt, including

the current portion, was approximately $453 million at May 31, 2010 and $456 million at May 31, 2009.

In fiscal years 2003 and 2004, the Company issued a total of $240 million in medium−term notes of which $190 million, at face value, were

outstanding at May 31, 2010. The outstanding notes have coupon rates that range from 4.70% to 5.66% and maturity dates ranging from July 2012 to

October 2015. For each of these notes, except the $50 million note maturing in October 2013, the Company has entered into interest rate swap agreements

whereby the Company receives fixed interest payments at the same rate as the notes and pays variable interest payments based on the six−month LIBOR

plus a spread. Each swap has the same notional amount and maturity date as the corresponding note. At May 31, 2010, the interest rates payable on these

swap agreements ranged from approximately 0.3% to 1.1%.

74