Nike 2010 Annual Report Download - page 73

Download and view the complete annual report

Please find page 73 of the 2010 Nike annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

|

|

Table of Contents NIKE, INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS — (Continued)

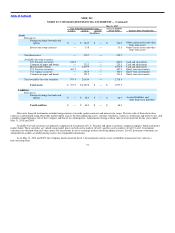

Note 6 — Fair Value Measurements

The Company measures certain financial assets and liabilities at fair value on a recurring basis, including derivatives and available−for−sale

securities. Fair value is a market−based measurement that should be determined based on the assumptions that market participants would use in pricing an

asset or liability. As a basis for considering such assumptions, the Company uses a three−level hierarchy established by the FASB which prioritizes fair

value measurements based on the types of inputs used for the various valuation techniques (market approach, income approach, and cost approach).

The levels of hierarchy are described below:

• Level 1: Observable inputs such as quoted prices in active markets for identical assets or liabilities.

• Level 2: Inputs other than quoted prices that are observable for the asset or liability, either directly or indirectly; these include quoted prices for

similar assets or liabilities in active markets and quoted prices for identical or similar assets or liabilities in markets that are not active.

• Level 3: Unobservable inputs in which there is little or no market data available, which require the reporting entity to develop its own

assumptions.

The Company’s assessment of the significance of a particular input to the fair value measurement in its entirety requires judgment and considers

factors specific to the asset or liability. Financial assets and liabilities are classified in their entirety based on the most stringent level of input that is

significant to the fair value measurement.

70