General Motors 2014 Annual Report Download - page 55

Download and view the complete annual report

Please find page 55 of the 2014 General Motors annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

|

|

GENERAL MOTORS COMPANY AND SUBSIDIARIES

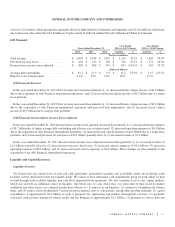

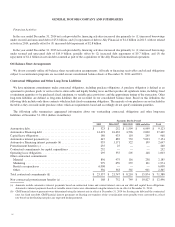

(c) Amounts include other postretirement employee benefits (OPEB) payments under the current U.S. contractual labor agreements through 2015

and Canada labor agreements through 2016. These agreements are generally renegotiated in the year of expiration. Amounts do not include

pension funding obligations, which are discussed under the caption “Critical Accounting Estimates — Pensions.”

(d) Amounts do not include future cash payments for long-term purchase obligations and other accrued expenditures (unless specifically listed in

the table above) which were recorded in Accounts payable or Accrued liabilities at December 31, 2014.

(e) Amounts include all expected future payments for both current and expected future service at December 31, 2014 for OPEB obligations for

salaried employees and hourly OPEB obligations extending beyond the current North American union contract agreements. Amounts do not

include pension funding obligations, which are discussed under the caption “Critical Accounting Estimates — Pensions.”

The table above does not reflect product warranty and related liabilities of $9.6 billion and unrecognized tax benefits of $1.9 billion

due to the uncertainty regarding the future cash outflows associated with these amounts.

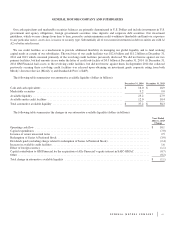

Critical Accounting Estimates

Accounting estimates are an integral part of the consolidated financial statements. These estimates require the use of judgments and

assumptions that affect the reported amounts of assets and liabilities, the disclosure of contingent assets and liabilities at the date of

the financial statements and the reported amounts of revenues and expenses in the periods presented. We believe that the accounting

estimates employed are appropriate and the resulting balances are reasonable; however, due to the inherent uncertainties in making

estimates actual results could differ from the original estimates, requiring adjustments to these balances in future periods. Refer to

Note 2 to our consolidated financial statements for our significant accounting policies related to our critical accounting estimates.

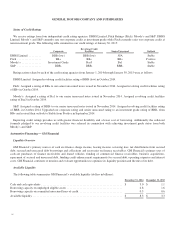

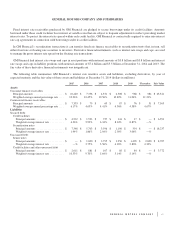

Pensions

Our defined benefit pension plans are accounted for on an actuarial basis, which requires the selection of various assumptions,

including an expected long-term rate of return on plan assets, a discount rate, mortality rates of participants and expectation of

mortality improvement. The expected long-term rate of return on U.S. plan assets that is utilized in determining pension expense is

derived from periodic studies, which include a review of asset allocation strategies, anticipated future long- term performance of

individual asset classes, risks using standard deviations and correlations of returns among the asset classes that comprise the plans’

asset mix. While the studies give appropriate consideration to recent plan performance and historical returns, the assumptions are

primarily long-term, prospective rates of return.

In December 2014 an investment policy study was completed for the U.S. pension plans. The study resulted in new target asset

allocations being approved for the U.S. pension plans with resulting changes to the expected long-term rate of return on assets. The

weighted-average long-term rate of return on assets decreased from 6.5% at December 31, 2013 to 6.4% at December 31, 2014.

Another key assumption in determining net pension expense is the assumed discount rate used to discount plan obligations. We

estimate this rate for U.S. plans using a cash flow matching approach, which uses projected cash flows matched to spot rates along a

high quality corporate yield curve to determine the present value of cash flows to calculate a single equivalent discount rate.

Mortality assumptions for participants in our U.S. pension plans incorporate future mortality improvements from tables published

by the Society of Actuaries (SOA). We periodically review the mortality experience of our U.S. pension plans’ participants against

these assumptions. In the three months ended December 31, 2014 the SOA issued new mortality and mortality improvement tables

that raise life expectancies and thereby indicate the amount of estimated aggregate benefit payments to our U.S. pension plans’

participants is increasing. We have incorporated the new SOA mortality and mortality improvement tables into our December 31,

2014 measurement of our U.S. pension plans’ benefit obligations. The change in these assumptions had the effect of increasing the

December 31, 2014 U.S. pension plans’ obligations by $2.2 billion.

Significant differences in actual experience or significant changes in assumptions may materially affect the pension obligations.

The effects of actual results differing from assumptions and the changing of assumptions are included in unamortized net actuarial

gains and losses that are subject to amortization to expense over future periods. The unamortized pre-tax actuarial gain (loss) on our

55