General Motors 2014 Annual Report Download - page 83

Download and view the complete annual report

Please find page 83 of the 2014 General Motors annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

|

|

GENERAL MOTORS COMPANY AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS — (Continued)

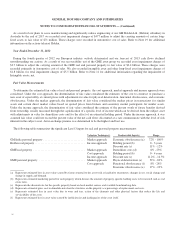

The following table summarizes the amortized cost and the fair value of investments classified as available-for-sale by contractual

maturity at December 31, 2014 (dollars in millions):

Amortized Cost Fair Value

Due in one year or less ................................................................ $ 14,461 $ 14,461

Due after one year through five years .................................................... 1,951 1,950

Total contractual maturities of available-for-sale securities ................................... $ 16,412 $ 16,411

Peugeot S.A.

In December 2013 we sold our seven percent investment in PSA common stock for $339 million, net of disposal costs and we

recorded a net gain of $152 million in Interest income and other non-operating income, net.

At December 31, 2012 we determined that the carrying amount of our investment in PSA common stock was impaired and that the

impairment was other-than-temporary. As a result we transferred the total unrealized losses from Accumulated other comprehensive

loss to Interest income and other non-operating income, net resulting in an impairment charge of $220 million.

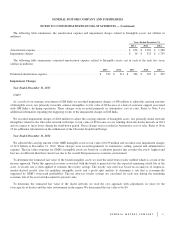

Note 5. GM Financial Receivables, net

The following table summarizes the components of consumer and commercial finance receivables, net (dollars in millions):

December 31, 2014 December 31, 2013

Consumer Commercial Total Consumer Commercial Total

Pre-acquisition finance receivables, outstanding

amount ..................................... $ 508 $ — $ 508 $ 1,294 $ — $ 1,294

Pre-acquisition finance receivables, carrying amount . . $ 459 $ — $ 459 $ 1,174 $ — $ 1,174

Post-acquisition finance receivables, net of fees ...... 25,164 7,606 32,770 21,956 6,050 28,006

Finance receivables ............................. 25,623 7,606 33,229 23,130 6,050 29,180

Less: allowance for loan losses .................... (655) (40) (695) (497) (51) (548)

GM Financial receivables, net .................... $ 24,968 $ 7,566 $ 32,534 $ 22,633 $ 5,999 $ 28,632

Fair value of GM Financial receivables, net .......... $ 33,106 $ 28,668

Allowance for loan losses classified as current at December 31, 2014 and 2013 were $529 million and $427 million.

GM Financial determines the fair value of consumer finance receivables using observable and unobservable inputs within a cash

flow model. The inputs reflect assumptions regarding expected prepayments, deferrals, delinquencies, recoveries and charge-offs of

the loans within the portfolio. The cash flow model produces an estimated amortization schedule of the finance receivables which is

the basis for the calculation of the series of cash flows that derive the fair value of the portfolio. The series of cash flows are

calculated and discounted using a weighted-average cost of capital (WACC) or current interest rates. The WACC uses unobservable

debt and equity percentages, an unobservable cost of equity and an observable cost of debt based on companies with a similar credit

rating and maturity profile as the portfolio. Macroeconomic factors could affect the credit performance of the portfolio and therefore

could potentially affect the assumptions used in GM Financial’s cash flow model. A substantial majority of commercial finance

receivables have variable interest rates and maturities of one year or less. Therefore, the carrying amount is considered to be a

reasonable estimate of fair value.

83