Humana 2004 Annual Report Download - page 118

Download and view the complete annual report

Please find page 118 of the 2004 Humana annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124

|

|

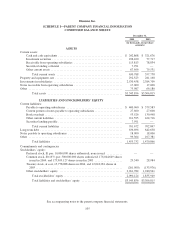

Humana Inc.

SCHEDULE I—PARENT COMPANY FINANCIAL INFORMATION

NOTES TO CONDENSED FINANCIAL STATEMENTS

1. BASIS OF PRESENTATION

Parent company financial information has been derived from our consolidated financial statements and

excludes the accounts of all operating subsidiaries. This information should be read in conjunction with our

consolidated financial statements.

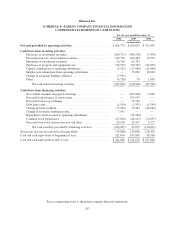

2. TRANSACTIONS WITH SUBSIDIARIES

Management Fee

Through intercompany service agreements approved, if required, by state regulatory authorities, Humana

Inc., our parent company, charges a management fee for reimbursement of certain centralized services provided

to its subsidiaries including information systems, disbursement, investment and cash administration, marketing,

legal, finance, and medical and executive management oversight.

Dividends

Cash dividends received from subsidiaries and included as a component of net cash provided by operating

activities were $126.0 million in 2004, $131.0 million in 2003 and $198.0 million in 2002.

Guarantee

Through indemnity agreements approved by state regulatory authorities, certain of our regulated

subsidiaries generally are guaranteed by our parent company in the event of insolvency for; (1), member

coverage for which premium payment has been made prior to insolvency; (2), benefits for members then

hospitalized until discharged; and (3), payment to providers for services rendered prior to insolvency. Our parent

has also guaranteed the obligations of our TRICARE subsidiaries.

Notes Receivables from Operating Subsidiaries

We funded certain subsidiaries with surplus note agreements. These notes are generally non-interest bearing

and may not be entered into or repaid without the prior approval of the applicable Departments of Insurance.

Notes Payable to Operating Subsidiaries

We borrowed funds from certain subsidiaries with notes generally collateralized by real estate. These notes,

which have various payment and maturity terms, bear interest ranging from 3.33% to 6.65% and are payable

between 2005 and 2009. We recorded interest expense of $1.7 million, $3.9 million and $4.2 million related to

these notes for the years ended December 31, 2004, 2003 and 2002, respectively.

3. REGULATORY REQUIREMENTS

Certain of our subsidiaries operate in states that regulate the payment of dividends, loans, or other cash

transfers to Humana Inc., our parent company, require minimum levels of equity, as well as limit investments to

approved securities. The amount of dividends that may be paid to Humana Inc. by these subsidiaries, without

prior approval by state regulatory authorities, is limited based on the entity’s level of statutory income and

statutory capital and surplus. In most states, prior notification is provided before paying a dividend even if

approval is not required.

As of December 31, 2004, we maintained aggregate statutory capital and surplus of $1,185.5 million in our

state regulated health insurance subsidiaries. Each of these subsidiaries was in compliance with applicable

statutory requirements which aggregated $717.2 million. Although the minimum required levels of equity are

largely based on premium volume, product mix, and the quality of assets held, minimum requirements can vary

significantly at the state level. Certain states rely on risk-based capital requirements, or RBC, to define the

required levels of equity. RBC is a model developed by the National Association of Insurance Commissioners to

monitor an entity’s solvency. This calculation indicates recommended minimum levels of required capital and

surplus and signals regulatory measures should actual surplus fall below these recommended levels. If RBC were

adopted by all states at December 31, 2004, each of our subsidiaries would be in compliance and we would have

$405.6 million of aggregate capital and surplus above any of the levels that require corrective action under RBC.

108