Humana 2004 Annual Report Download - page 89

Download and view the complete annual report

Please find page 89 of the 2004 Humana annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

|

|

Humana Inc.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

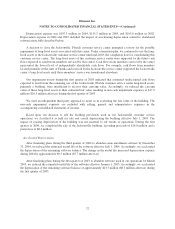

At December 31, 2004, we had no commercial paper borrowings outstanding.

Other Borrowings

Other borrowings of $4.3 million at December 31, 2004 represent financing for the renovation of a building,

bear interest at 2% per annum, are collateralized by the building, and are payable in various installments through

2014.

Shelf Registration

Our universal shelf registration with the Securities and Exchange Commission allows us to register debt or

equity securities, from time to time, with the amount, price and terms to be determined at the time of the sale.

After the issuance of our $300 million, 6.30% senior notes in August 2003, we have up to $300 million

remaining from a total of $600 million under the universal shelf registration. The universal shelf registration

allows us to use the net proceeds from any future sales of our securities for our operations and for other general

corporate purposes, including repayment or refinancing of borrowings, working capital, capital expenditures,

investments, acquisitions, or the repurchase of our outstanding securities.

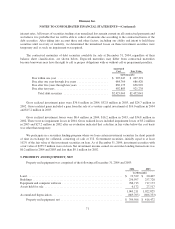

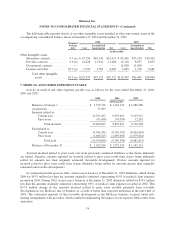

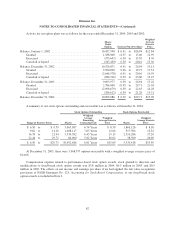

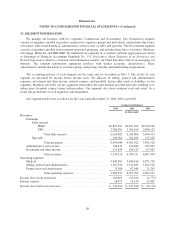

10. PROFESSIONAL LIABILITY RISKS

Activity in the reserve for professional liability risks was as follows for the years ended December 31, 2004,

2003 and 2002:

2004 2003 2002

(in thousands)

Gross reserve at January 1 ........................................ $242,516 $ 262,763 $ 301,518

Less recoverables from insurance .............................. (95,008) (142,595) (186,973)

Net reserve at January 1.......................................... 147,508 120,168 114,545

Incurred related to:

Current year ............................................... 53,525 48,778 39,332

Prior years ................................................ (688) — (15,868)

Total incurred ................................................. 52,837 48,778 23,464

Paid related to:

Current year ............................................... (659) (1,356) (659)

Prior years ................................................ (20,615) (20,082) (17,182)

Total paid ..................................................... (21,274) (21,438) (17,841)

Net reserve at December 31....................................... 179,071 147,508 120,168

Plus recoverables from insurance .............................. 52,423 95,008 142,595

Gross reserve at December 31 ..................................... $231,494 $ 242,516 $ 262,763

While our total net estimate of incurred claims for prior years did not change significantly during either

2004 or 2003, the individual components of this liability did fluctuate. Favorable development associated with

our professional and general liability exposures was offset by the need for additional reserves for our director and

officer errors and omissions risks. Changes in estimates of incurred claims for prior years recognized in the year

ended December 31, 2002 were attributable to favorable loss development, primarily related to professional and

general liability exposures. Since January 1, 2002, we have reduced the amount of coverage purchased from third

party insurance carriers, causing an increase in the provision for professional liability risks and a decrease in the

estimated recoverables from insurance. The total cost associated with our professional liabilities, including the

79