Humana 2004 Annual Report Download - page 23

Download and view the complete annual report

Please find page 23 of the 2004 Humana annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

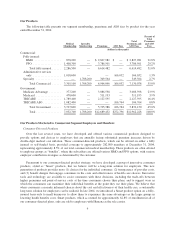

|

|

brokers and agents on other bases. These include commission bonuses based on sales that attain certain levels or

involve particular products. We also pay additional commission based on aggregate volumes of sales involving

multiple customers.

At December 31, 2004, we employed approximately 600 sales representatives, who are each paid a salary

and/or per member commission, to market our Medicare Advantage and Medicaid products in the continental

United States. We also employed approximately 350 telemarketing representatives who assisted in the marketing

of Medicare Advantage and Medicaid products by making appointments for sales representatives with

prospective members.

Risk Management

Through the use of internally developed underwriting criteria, we determine the risk we are willing to

assume and the amount of premium to charge for our commercial products. In most instances, employer and

other groups must meet our underwriting standards in order to qualify to contract with us for coverage. Small

group reform laws in some states have imposed regulations which provide for guaranteed issue of certain health

insurance products and prescribe certain limitations on the variation in rates charged based upon assessment of

health conditions.

Underwriting techniques are not employed in connection with Medicare Advantage products because CMS

regulations require us to accept all eligible Medicare applicants regardless of their health or prior medical history.

We also are not permitted to employ underwriting criteria for the Medicaid product, but rather we follow CMS

and state requirements.

Competition

The health benefits industry is highly competitive and contracts for the sale of commercial products are

generally bid or renewed annually. The number of plans participating in the Medicare Advantage program is

likely to increase due to higher payments from the government, the establishment of regional Medicare

Advantage plans, and the introduction of new Medicare PPO plans. Additionally, the impact of the new Medicare

bidding process, replacing the Adjusted Community Rate (ACR) process in 2006, is uncertain. Our competitors

vary by local market and include other managed care companies, national insurance companies, and other HMOs

and PPOs, including HMOs and PPOs owned by Blue Cross/Blue Shield plans. Many of our competitors have

larger memberships and/or greater financial resources than our health plans in the markets in which we compete.

Our ability to sell our products and to retain customers is, or may be, influenced by such factors as benefits,

pricing, contract terms, number and quality of participating physicians and other providers, utilization review,

claims processing, administrative efficiency, relationships with agents, quality of customer service, and

accreditation results.

Government Regulation

Government regulation of health care products and services is a changing area of law that varies from

jurisdiction to jurisdiction. Regulatory agencies generally have broad discretion to issue regulations and interpret

and enforce laws and rules. The passing of the Medicare Modernization Act of 2004 represents the most

sweeping changes to Medicare since the BBA. Changes in applicable laws and regulations are continually being

considered, and the interpretation of existing laws and rules also may change periodically. These regulatory

revisions could affect our operations and financial results. Also, it may become increasingly difficult to control

medical costs if federal and state bodies continue to consider and enact significant and sometimes onerous

managed care laws and regulations.

Enforcement of health care fraud and abuse laws has become a top priority for the nation’s law enforcement

entities. The funding of such law enforcement efforts has increased dramatically in the past few years and is

13