Humana 2004 Annual Report Download - page 86

Download and view the complete annual report

Please find page 86 of the 2004 Humana annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

|

|

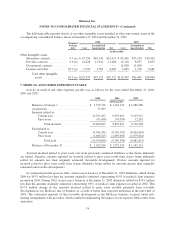

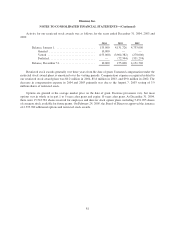

Humana Inc.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

Changes in the capital loss valuation allowance resulted from our regular evaluation of probable capital gain

realization in the allowable carryforward period given our recent and historical capital gain experience and the

consideration of alternative tax planning strategies. During 2002, the Internal Revenue Service completed their

audit of all open years prior to 2000 which resulted in an adjustment to the estimated accrual for income taxes.

Deferred income tax balances reflect the impact of temporary differences between the tax bases of assets or

liabilities and their reported amounts in our consolidated financial statements, and are stated at enacted tax rates

expected to be in effect when the reported amounts are actually recovered or settled. Principal components of our

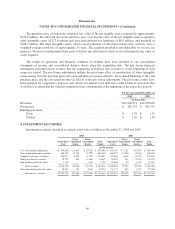

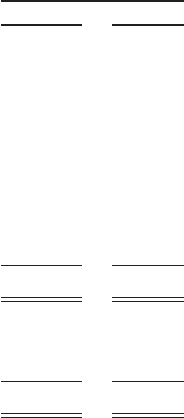

net deferred tax balances at December 31, 2004 and 2003 were as follows:

Assets (Liabilities)

2004 2003

(in thousands)

Investment securities .................................... $ (10,522) $(10,765)

Depreciable property and intangible assets ................... (110,369) (80,255)

Medical and other expenses payable ........................ (2,538) 6,161

Unearned revenues ...................................... 8,858 25,619

Professional liability risks ................................ 13,193 12,386

Compensation, severance, and other accruals ................. 45,047 42,720

Net operating loss carryforwards ........................... 13,970 16,303

Capital loss carryforward ................................. 22,078 30,868

Valuation allowance—capital loss carryforward ............... (20,123) (26,978)

Total net deferred income tax (liabilities) assets ....... $ (40,406) $ 16,059

Amounts recognized in the consolidated balance sheets:

Other current assets ................................. $ 19,428 $ 56,527

Other long-term liabilities ............................ (59,834) (40,468)

Total net deferred income tax (liabilities) assets ....... $ (40,406) $ 16,059

At December 31, 2004, we had approximately $35.9 million of net operating losses to carryforward related

to prior acquisitions. These net operating loss carryforwards, if unused to offset future taxable income, will

expire in 2005 through 2019.

At December 31, 2004, we had approximately $56.8 million of capital losses to carryforward, primarily

related to the sale of our workers’ compensation business in 2000. These capital loss carryforwards, if unused to

offset future capital gains, will expire in 2005. Accordingly, a valuation allowance has been established for the

amount of related deferred tax assets that more likely than not will not be realized.

Based on our historical record of producing taxable income and estimates of future capital gains and

profitability, we have concluded that future operating income and capital gains will be sufficient to give rise to

tax expense and capital gains to recover all deferred tax assets, net of the valuation allowance.

76