Humana 2004 Annual Report Download - page 78

Download and view the complete annual report

Please find page 78 of the 2004 Humana annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

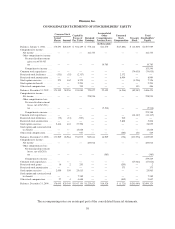

|

|

Humana Inc.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

in any SPE transactions. The adoption of FIN 46 or FIN 46-R did not have a material impact on our financial

position, results of operations, or cash flows.

In December 2004, the FASB issued Statement No. 123R, Share-Based Payment, or Statement 123R, which

requires companies to expense the fair value of employee stock options and other forms of stock-based

compensation. This requirement represents a significant change because fixed-based stock option awards, a

predominate form of stock compensation for us, were not recognized as compensation expense under APB 25.

Statement 123R requires the cost of the award, as determined on the date of grant at fair value, be recognized

over the period during which an employee is required to provide service in exchange for the award (usually the

vesting period). The grant-date fair value of the award will be estimated using option-pricing models. We are

required to adopt Statement 123R no later than July 1, 2005 under one of three transition methods, including a

prospective, retrospective and combination approach. We previously disclosed on page 67 the effect of expensing

stock options under a fair value approach using the Black-Scholes pricing model for 2004, 2003 and 2002. We

currently are evaluating all of the provisions of Statement 123R and the expected effect on us including, among

other items, reviewing compensation strategies related to stock-based awards, selecting an option pricing model

and determining the transition method.

In March 2004, the FASB issued EITF Issue No. 03-1, or EITF 03-1, The Meaning of Other-Than-

Temporary Impairment and its Application to Certain Investments. EITF 03-1 includes new guidance for

evaluating and recording impairment losses on certain debt and equity investments when the fair value of the

investment security is less than its carrying value. In September 2004, the FASB delayed the previously

scheduled third quarter 2004 effective date until the issuance of additional implementation guidance, expected in

2005. Upon issuance of a final standard, we will evaluate the impact on our consolidated financial position and

results of operations.

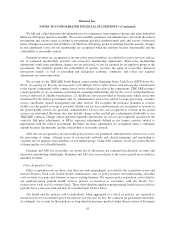

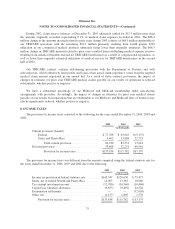

3. ACQUISITIONS

On February 16, 2005, we acquired CarePlus Health Plans of Florida, or CarePlus, as well as its affiliated 10

medical centers and pharmacy company. CarePlus provides Medicare Advantage HMO plans and benefits to

Medicare eligible members in Miami-Dade, Broward and Palm Beach counties. This acquisition enhances our

Medicare market position in South Florida. We paid approximately $450 million in cash including estimated

transaction costs, subject to a balance sheet settlement process with a nine month claims run-out period. We

currently are in the process of allocating the purchase price to the net tangible and intangible assets.

On April 1, 2004, we acquired Ochsner Health Plan, or Ochsner, from the Ochsner Clinic Foundation.

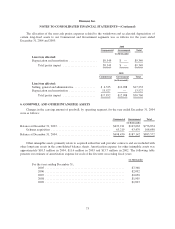

Ochsner is a Louisiana health benefits company offering network-based managed care plans to employer-groups

and Medicare eligible members. This acquisition enabled us to enter a new market with significant market share

which should facilitate new sales opportunities in this and surrounding markets, including Houston, Texas.

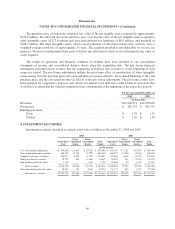

We paid $157.1 million in cash, including transaction costs. The fair value of the tangible assets (liabilities)

as of the acquisition date are as follows:

(in thousands)

Cash and cash equivalents ......................................... $15,270

Investment securities ............................................. 84,527

Premiums receivable and other current assets .......................... 20,616

Property and equipment and other assets .............................. 6,847

Medical and other expenses payable ................................. (71,063)

Other current liabilities ........................................... (21,604)

Other liabilities ................................................. (82)

Net tangible assets acquired .................................... $34,511

68