Humana 2004 Annual Report Download - page 22

Download and view the complete annual report

Please find page 22 of the 2004 Humana annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

|

|

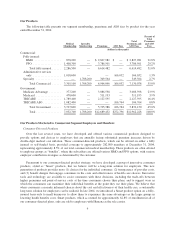

Health Plan Employer Data Information Sets, or HEDIS, which is used by employers, government purchasers

and the National Committee for Quality Assurance, or NCQA, to evaluate HMOs based on various criteria,

including effectiveness of care and member satisfaction.

Physicians participating in our HMO networks must satisfy specific criteria, including licensing, patient

access, office standards, after-hours coverage, and other factors. Most participating hospitals also meet

accreditation criteria established by CMS and/or the Joint Commission on Accreditation of Healthcare

Organizations, or JCAHO.

Recredentialing of participating providers occurs every two to three years, depending on applicable state

laws. Recredentialing of participating physicians includes verification of their medical license; review of their

malpractice liability claims history; review of their board certification, if applicable; and review of any

complaints, including member appeals and grievances. Committees, composed of a peer group of physicians,

review the applications of physicians being considered for credentialing and recredentialing.

We request accreditation for certain of our HMO plans from NCQA and the American Accreditation

Healthcare Commission/Utilization Review Accreditation Commission, or AAHC/URAC. Accreditation or

external review by an approved organization is mandatory in the states of Florida and Kansas for licensure as an

HMO. Accreditation specific to the utilization review process also is required in the state of Georgia for licensure

as an HMO or PPO. Certain commercial businesses, like those impacted by third-party labor agreements or those

where a request is made by the employer, may require or prefer accredited health plans.

NCQA performs reviews of standards for quality improvement, credentialing, utilization management, and

member rights and responsibilities. We continue to maintain accreditation in select markets through NCQA.

AAHC/URAC performs reviews for utilization management standards and for health plan and health

network standards in quality management, credentialing, rights and responsibilities, and network management.

We continue to maintain URAC accreditation in select markets and certain operations.

Humana has pursued ISO 9001:2000 over the past two years for the Clinical Innovation Center. ISO is the

international standards organization, which has developed an international commercial set of certifications as to

quality and process, called ISO 9001:2000. At this time, the following clinical programs have received ISO

9001:2000 registration: transplant management, centralized clinical operations providing personal nurse services,

pharmacy management, and disease management.

Sales and Marketing

Individuals become members of our commercial HMOs and PPOs through their employers or other groups

which typically offer employees or members a selection of health insurance products, pay for all or part of the

premiums, and make payroll deductions for any premiums payable by the employees. We attempt to become an

employer’s or group’s exclusive source of health insurance benefits by offering a variety of HMO, PPO, and

specialty products that provide cost-effective quality health care coverage consistent with the needs and

expectations of the employees or members. Since June 2002, we also offer commercial health insurance products

to individuals.

We use various methods to market our commercial, Medicare Advantage, and Medicaid products, including

television, radio, the Internet, telemarketing, and direct mailings. At December 31, 2004, we used approximately

37,400 licensed independent brokers and agents and approximately 400 licensed employees to sell our

commercial products. Many of our employer group customers are represented by insurance brokers and

consultants who assist these groups in the design and purchase of health care products. We generally pay brokers

a commission based on premiums, with commissions varying by market and premium volume. In addition to

commission based directly on premium volume for sales to particular customers, we also have programs that pay

12