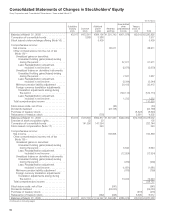

Sony 2006 Annual Report Download - page 102

Download and view the complete annual report

Please find page 102 of the 2006 Sony annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

|

|

100

other operating costs such as personnel expenses, depreciation

of fixed assets, and office rental of subsidiaries in the Financial

Services segment.

■ Advertising costs

Advertising costs are expensed when the advertisement or

commercial appears in the selected media, except for advertising

costs for acquiring new insurance policies which are deferred

and amortized as part of insurance acquisition costs.

■ Shipping and handling costs

The majority of shipping and handling, warehousing and internal

transfer costs for finished goods are included in selling, general

and administrative expenses. An exception to this is in the

Pictures segment where such costs are charged to cost of sales

as they are integral part of producing and distributing the film

under SOP 00-2, “Accounting by Producers or Distributors of

Films”. All other costs related to Sony’s distribution network are

included in cost of sales, including inbound freight charges,

purchasing and receiving costs, inspection costs and warehous-

ing costs for raw materials and in-process inventory. Amounts

paid by customers for shipping and handling costs are included

in net sales.

■ Income taxes

The provision for income taxes is computed based on the pretax

income included in the consolidated statements of income. The

asset and liability approach is used to recognize deferred tax

assets and liabilities for the expected future tax consequences

of temporary differences between the carrying amounts and the

tax bases of assets and liabilities. Sony records valuation

allowances to reduce deferred tax assets to the amount that

management believes is more likely than not to be realized. In

assessing the likelihood of realization, Sony considers all

currently available evidence for future years, both positive and

negative, supplemented by information of historical results for

each tax jurisdiction.

■ Net income per share

Prior to December 1, 2005, Sony calculated and presented per

share data separately for Sony’s common stock and for the

subsidiary tracking stock by the “two-class” method based on

FAS No. 128. As the holders of the subsidiary tracking stock

had the right to participate in earnings, together with common

stockholders, under this method, basic net income per share

(“EPS”) for each class of stock was calculated based on the

earnings allocated to each class of stock for the applicable

period, divided by the weighted-average number of outstanding

shares in each class during the applicable period.

The earnings allocated to the subsidiary tracking stock were

determined based on the subsidiary tracking stock holders’

economic interest in the targeted subsidiary’s earnings available

for dividends. As defined by Sony Corporation’s articles of

incorporation, the amount distributable to the subsidiary tracking

stock holders was based on the declared dividends of the

targeted subsidiary, which might only be declared from the

amounts available for dividends of the targeted subsidiary.

The targeted subsidiary’s earnings available for dividends were,

as stipulated by the Japanese Commercial Code, not including

those of the targeted subsidiary’s subsidiaries. If the targeted

subsidiary had accumulated losses, a change in accumulated

losses was also allocated to the subsidiary tracking stock.

The subsidiary tracking stock holders’ economic interest was

calculated as the number of the subsidiary tracking stock

outstanding divided by the number of the targeted subsidiary’s

common stock outstanding subject to multiplying by the

Standard Ratio (tracking stock : subsidiary’s common stock=

1:100, as defined in the articles of incorporation). The earnings

allocated to the common stock were calculated by subtracting

the earnings allocated to the subsidiary tracking stock from

Sony’s net income for the period.

On October 26, 2005, the Board of Directors of Sony

Corporation decided to terminate all shares of subsidiary tracking

stock and convert such shares to shares of Sony common

stock at a conversion rate of 1.114 share of Sony common

stock per share of subsidiary tracking stock. All shares of

subsidiary tracking stock were converted to shares of Sony

common stock on December 1, 2005. As a result of the

conversion, for the fiscal year ended March 31, 2006, Sony

calculated per share data separately for Sony’s common stock

and for the subsidiary tracking stock by the “two-class” method

based on FAS No. 128, but did not present per share data for

the subsidiary tracking stock. The earnings allocated to common

stock for the fiscal year ended March 31, 2006 were calculated

by subtracting the earnings allocated to the subsidiary tracking

stock for the eight months ended November 30, 2005.

The computation of diluted net income per common stock

reflects the maximum possible dilution from conversion, exer-

cise, or contingent issuance of securities including the conver-

sion of Co-Cos regardless of whether the conditions to exercise

the conversion rights have been met.

(3) Recent pronouncements:

■ Accounting for stock-based compensation

In December 2004, the FASB issued FAS No. 123 (revised 2004),

“Share-Based Payment” (“FAS No. 123(R)”). This statement

requires the use of the fair value based method of accounting

for employee stock-based compensation and eliminates the