Sony 2006 Annual Report Download - page 113

Download and view the complete annual report

Please find page 113 of the 2006 Sony annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

|

|

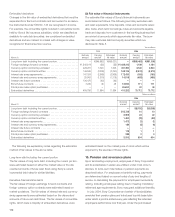

111

exchange forward contracts, foreign currency option contracts

and interest rate and currency swap agreements.

Changes in the fair value of derivatives designated as cash

flow hedges are initially recorded in other comprehensive income

and reclassified into earnings when the hedged transaction

affects earnings. For the fiscal years ended March 31, 2004 and

2006, these cash flow hedges were fully effective. For the fiscal

year ended March 31, 2005, the amount of ineffectiveness of

these cash flow hedges that was reflected in earnings was not

material. In addition, there were no amounts excluded from the

assessment of hedge effectiveness of cash flow hedges. At

March 31, 2006, amounts related to derivatives qualifying as

cash flow hedges amounted to a net reduction of equity of

¥2,049 million ($18 million). Within the next twelve months,

¥1,453 million ($12 million) is expected to be reclassified from

equity into earnings as loss. For the fiscal year ended March 31,

2006, there were no forecasted transactions that failed to occur

which resulted in the discontinuance of cash flow hedges.

Derivatives not designated as hedges

The derivatives not designated as hedges under FAS No. 133

include foreign exchange forward contracts, foreign currency

option contracts, interest rate and currency swap agreements,

interest rate and bond future contracts, stock price index option

contracts, convertible rights included in convertible bonds and

other derivatives.

Changes in the fair value of derivatives not designated as

hedges are recognized in income.

A description of the purpose and classification of the

derivative financial instruments held by Sony is as follows:

Foreign exchange forward contracts and foreign currency option

contracts

Sony enters into foreign exchange forward contracts and pur-

chased and written foreign currency option contracts primarily to

fix the cash flows from intercompany accounts receivable and

payable and forecasted transactions denominated in functional

currencies (Japanese yen, U.S. dollars and euros) of Sony’s

major operating units. The majority of written foreign currency

option contracts are a part of range forward contract arrange-

ments and expire in the same month with the corresponding

purchased foreign currency option contracts.

Sony also enters into foreign exchange forward contracts,

which effectively fix the cash flows from foreign currency denomi-

nated debt. Accordingly, these derivatives have been designated

as cash flow hedges in accordance with FAS No. 133.

Foreign exchange forward contracts and foreign currency option

contracts that do not qualify as hedges are marked-to-market with

changes in value recognized in other income and expenses.

Foreign exchange forward contracts and foreign currency

option contracts held by certain subsidiaries in the Financial

Services segment are marked-to-market with changes in value

recognized in financial service revenue.

Interest rate and currency swap agreements

Sony enters into interest rate and currency swap agreements,

which are used for reducing the risk arising from the changes in

the fair value of fixed rate debt and available-for-sale debt

securities. For example, Sony enters into interest rate and

currency swap agreements, which effectively swap foreign

currency denominated fixed rate debt for functional currency

denominated variable rate debt. These derivatives are consid-

ered to be a hedge against changes in the fair value of Sony’s

foreign denominated fixed-rate obligations. Accordingly, these

derivatives have been designated as fair value hedges in

accordance with FAS No. 133.

Sony also enters into interest rate and currency swap

agreements that are used for reducing the risk arising from

the changes in anticipated cash flow of variable rate debt and

foreign currency denominated debt. For example, Sony enters

into interest rate and currency swap agreements, which effec-

tively swap foreign currency denominated variable rate debt for

functional currency denominated fixed rate debt. These deriva-

tives are considered to be a hedge against changes in the

anticipated cash flow of Sony’s foreign denominated variable rate

obligations. Accordingly, these derivatives have been designated

as cash flow hedges in accordance with FAS No. 133.

Certain subsidiaries in the Financial Services segment have

interest rate swap agreements as part of their portfolio invest-

ments, which are marked-to-market with changes in value

recognized in financial service revenue. Interest rate and cur-

rency swap agreements held by certain subsidiaries in the

Financial Services segment are also marked-to-market with

changes in value recognized in financial service revenue.

Any other interest rate and currency swap agreements that

do not qualify as hedges, which are used for reducing the risk

arising from changes of variable rate debt, are marked-to-market

with changes in value recognized in other income and expenses.

Interest rate and bond future contracts

Certain subsidiaries in the Financial Services segment have

interest rate and bond future contracts as part of their portfolio

investments, which are marked-to-market with changes in value

recognized in financial service revenue.

Stock price index option contracts

Certain subsidiaries in the Financial Services segment have

stock price index option contracts as part of their portfolio

investments, which are marked-to-market with changes in value

recognized in financial service revenue.