Toyota 2011 Annual Report Download - page 65

Download and view the complete annual report

Please find page 65 of the 2011 Toyota annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

|

|

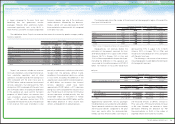

Lending Commitments

Contractual Obligations and Commitments

Off-Balance-Sheet Arrangements

0822

Financial Section and

Investor Information

Business and

Performance Review

Special FeatureMessage/Vision

Management and

Corporate Information

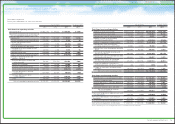

Toyota’s financial services operations issue credit

cards to customers. As customary for credit card

businesses, Toyota maintains credit facilities with

holders of credit cards issued by Toyota. These

facilities are used upon each holder’s requests up

to the limits established on an individual holder’s

basis. Although loans made to customers through

these facilities are not secured, for the purposes

of minimizing credit risks and of appropriately

establishing credit limits for each individual credit

card holder, Toyota employs its own risk manage-

ment policy which includes an analysis of

information provided by financial institutions in

alliance with Toyota. Toyota periodically reviews

and revises, as appropriate, these credit limits.

Outstanding credit facilities with credit card

holders were ¥261.7 billion as of March 31, 2011.

Toyota’s financial services operations maintain

credit facilities with dealers. These credit facilities

may be used for business acquisitions, facilities

refurbishment, real estate purchases, and working

capital requirements. These loans are typically

collateralized with liens on real estate, vehicle

inventory, and/or other dealership assets, as

appropriate. Toyota obtains a personal guarantee

from the dealer or corporate guarantee from the

dealership when deemed prudent. Although the

loans are typically collateralized or guaranteed, the

value of the underlying collateral or guarantees

may not be sufficient to cover Toyota’s exposure

under such agreements. Toyota prices the credit

facilities according to the risks assumed in entering

into the credit facility. Toyota’s financial services

operations also provide financing to various

multi-franchise dealer organizations, referred to as

dealer groups, often as part of a lending consortium,

for wholesale inventory financing, business

acquisitions, facilities refurbishment, real estate

purchases, and working capital requirements.

Toyota’s outstanding credit facilities with dealers

totaled ¥1,590.6 billion as of March 31, 2011.

Credit Facilities with Credit Card Holders

Credit Facilities with Dealers

Management's Discussion and Analysis of Financial Condition and Results of Operations

For information regarding debt obligations, capital

lease obligations, operating lease obligations and

other obligations, including amounts maturing in

each of the next five years, see notes 13, 22 and 23

to the consolidated financial statements. In addition,

as part of Toyota’s normal business practices,

Toyota enters into long-term arrangements with

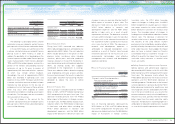

Toyota enters into certain guarantee contracts

with its dealers to guarantee customers’ payments

of their installment payables that arise from

installment contracts between customers and

Toyota dealers, as and when requested by Toyota

dealers. Guarantee periods are set to match the

maturity of installment payments, and as of March

31, 2011, ranged from one month to 35 years.

However, they are generally shorter than the

access funds from external sources in large

amounts and at relatively low costs. Toyota’s

ability to maintain its high credit ratings is subject

to a number of factors, some of which are not

within Toyota’s control. These factors include

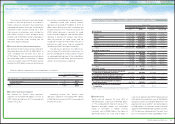

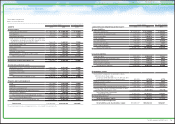

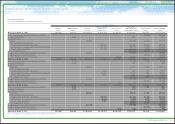

The following tables summarize Toyota’s contractual obligations and commercial commitments as of

March 31, 2011.

suppliers for purchases of certain raw materials,

components and services. These arrangements

may contain fixed/minimum quantity purchase

requirements. Toyota enters into such arrange-

ments to facilitate an adequate supply of these

materials and services.

useful lives of products sold. Toyota is required to

execute its guarantee primarily when customers

are unable to make required payments.

The maximum potential amount of future

payments as of March 31, 2011 is ¥1,662.2 billion.

Liabilities for these guarantees of ¥20.4 billion

have been provided as of March 31, 2011. Under

these guarantee contracts, Toyota is entitled to

recover any amounts paid by it from the customers

whose obligations it guaranteed.

general economic conditions in Japan and the

other major markets in which Toyota does

business, as well as Toyota’s successful

implementation of its business strategy.

Yen in millions

Payments Due by Period

Total

Less than

1 year

1 to 3

years

3 to 5

years

5 years

and after

Contractual Obligations:

Short-term borrowings (note 13)

Loans ¥ 1,140,066 ¥1,140,066 ¥ — ¥ — ¥ —

Commercial paper 2,038,943 2,038,943 — — —

Long-term debt* (note 13) 9,200,130 2,768,544 3,368,754 1,995,139 1,067,693

Capital lease obligations (note 13) 21,917 4,283 4,751 2,977 9,906

Non-cancelable operating lease obligations

(note 22) 44,179 9,198 13,126 8,709 13,146

Commitments for the purchase of property,

plant and other assets (note 23) 83,506 37,304 25,513 6,262 14,427

Total ¥12,528,741 ¥5,998,338 ¥3,412,144 ¥2,013,087 ¥1,105,172

* “Long-term debt” represents future principal payments.

Toyota uses its securitization program as part of

its funding through special purpose entities for its

financial services operations. Toyota is consid-

ered the primary beneficiary of these special

purpose entities and therefore consolidates them.

Toyota has not entered into any off-balance sheet

securitization transactions during fiscal 2011.

Guarantees

65TOYOTA ANNUAL REPORT 2011