Toyota 2011 Annual Report Download - page 77

Download and view the complete annual report

Please find page 77 of the 2011 Toyota annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

|

|

0822

Financial Section and

Investor Information

Business and

Performance Review

Special FeatureMessage/Vision

Management and

Corporate Information

Notes to Consolidated Financial Statements

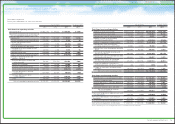

compliance with terms and conditions of the

underlying loan agreement and other subjective

factors related to the financial stability of the

borrower are considered when determining

whether a loan is impaired. Impaired finance

receivables include certain nonaccrual receivables

for which a specific reserve has been assessed.

Impaired receivables are excluded from the loan

risk pool used to determine general reserves.

All classes of wholesale and other dealer loan

receivables portfolio segment are placed on

nonaccrual status when full payment of principal

or interest is in doubt, principal or interest is 90

days or more contractually past due, whichever

occurs first. Collateral dependent loans are

placed on nonaccrual status if collateral is

insufficient to cover principal and interest. Interest

accrued but not collected at the date a receivable

is placed on nonaccrual status is reversed against

interest income. In addition, the amortization of

net deferred fees is suspended.

Interest income on nonaccrual receivables is

recognized only to the extent it is received in cash.

Accounts are restored to accrual status only when

interest and principal payments are brought

current and future payments are reasonably

assured. Receivable balances are written-off

against the allowance for credit losses when it is

probable that a loss has been realized. Retail

receivables class and finance lease receivables

class are not placed mainly on nonaccrual status

when principal or interest is 90 days or more past

due. However, these receivables are written-off

against the allowance for credit losses when

payments due are no longer expected to be

received or the account is 120 days contractually

past due, whichever occurs first.

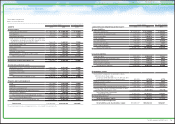

As of March 31, 2010, finance receivables on

nonaccrual status were ¥26,599 million.

As of March 31, 2010, finance receivables

past due over 90 days and still accruing were

¥38,150 million.

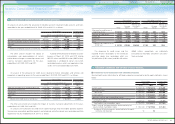

As of March 31, 2011, finance receivables

past due over 90 days and still accruing were as

follows:

As of March 31, 2011, finance receivables on

nonaccrual status were as follows:

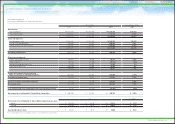

Allowance for credit losses is established to cover

probable losses on finance receivables and

vehicles and equipment on operating leases,

resulting from the inability of customers to make

required payments.

Provision for credit losses is included in selling,

general and administrative expenses. The

allowance for credit losses is based on a

systematic, ongoing review and evaluation

performed as part of the credit-risk evaluation

process, historical loss experience, the size and

composition of the portfolios, current economic

Allowance for credit losses

Allowance for residual value losses

Yen in millions

U.S. dollars in millions

March 31, March 31,

2011 2011

Retail ¥ 2,633 $ 32

Finance leases 1,136 14

Wholesale 6,722 81

Real estate 14,437 173

Working capital 272

3

¥25,200 $303

Yen in millions

U.S. dollars in millions

March 31, March 31,

2011 2011

Retail ¥23,734 $285

Finance leases

4,484

54

¥28,218 $339

events and conditions, the estimated fair value

and adequacy of collateral and other pertinent

factors. Vehicles and equipment on operating

leases are not within the scope of accounting

guidance governing the disclosure of portfolio

segments.

Toyota calculates allowance for credit losses to

cover probable losses on retail receivables by

applying reserve rates to such receivables.

Reserve rates are calculated mainly by historical

loss experience, current economic events and

conditions and other pertinent factors.

Toyota calculates allowance for credit losses to

cover probable losses on finance lease receivables

by applying reserve rates to such receivables.

Reserve rates are calculated mainly by historical

loss experience, current economic events and

conditions and other pertinent factors such as

used car markets.

Toyota calculates allowance for credit losses to

cover probable losses on wholesale and other

dealer loan receivables by applying reserve rates

to such receivables. Reserve rates are calculated

mainly by financial conditions of the dealers, terms

of collateral setting, current economic events and

conditions and other pertinent factors.

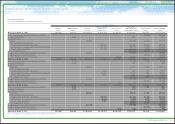

Toyota establishes specific reserves to cover

the estimated losses on individually impaired

receivables within the wholesale and other dealer

loan receivables portfolio segment. Specific

reserves on impaired receivables are determined

by the present value of expected future cash flows

or the fair value of collateral when it is probable

Retail receivables portfolio segment

Finance lease receivables portfolio segment

Wholesale and other dealer loan receivables

portfolio segment

that such receivables will be unable to be fully

collected. The fair value of the underlying collateral

is used if the receivable is collateral-dependent.

The receivable is determined collateral-dependent

if the repayment of the loan is expected to be

provided by the underlying collateral. For the

receivables in which the fair value of the underlying

collateral was in excess of the outstanding

balance, no allowance was provided.

Specific reserves on impaired receivables

within the wholesale and other dealer loan

receivables portfolio segment are recorded by an

increase to the allowance for credit losses based

on the related measurement of impairment.

Related collateral, if recoverable, is repossessed

and sold and the account balance is written-off.

Any shortfall between proceeds received and

the carrying cost of repossessed collateral is

charged to the allowance. Recoveries are reversed

from the allowance for credit losses.

Toyota is exposed to risk of loss on the disposition

of off-lease vehicles to the extent that sales

proceeds are not sufficient to cover the carrying

value of the leased asset at lease termination.

Toyota maintains an allowance to cover probable

estimated losses related to unguaranteed residual

values on its owned portfolio. The allowance is

evaluated considering projected vehicle return

rates and projected loss severity. Factors

considered in the determination of projected return

rates and loss severity include historical and

market information on used vehicle sales, trends

in lease returns and new car markets, and general

economic conditions. Management evaluates the

foregoing factors, develops several potential loss

scenarios, and reviews allowance levels to

determine whether reserves are considered

adequate to cover the probable range of losses.

77

TOYOTA ANNUAL REPORT 2011