Toyota 2011 Annual Report Download - page 68

Download and view the complete annual report

Please find page 68 of the 2011 Toyota annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

|

|

0822

Financial Section and

Investor Information

Business and

Performance Review

Special FeatureMessage/Vision

Management and

Corporate Information

residual value are still considered reasonable.

Factors affecting the estimated residual value at

lease maturity include, but are not limited to, new

vehicle incentive programs, new vehicle pricing,

used vehicle supply, projected vehicle return

rates, and projected loss severity. The vehicle

return rate represents the number of leased

vehicles returned at contract maturity and sold by

Toyota during the period as a percentage of the

number of lease contracts that, as of their origina-

tion dates, were scheduled to mature in the same

period. A higher rate of vehicle returns exposes

Toyota to higher potential losses incurred at lease

termination. Severity of loss is the extent to which

the end-of-term fair value of a lease is less than its

carrying value at lease end.

To the extent that sales incentives remain an

integral part of sales promotion, resale prices of

used vehicles and, correspondingly, the fair value

of Toyota’s leased vehicles could be subject to

downward pressure. The extent of the impact this

will have on the end of term residual value depends

on the significance of the incentive programs and

whether they are sustained over a number of

periods. This in turn can impact the projection of

future used vehicle values, adversely impacting

the expected residual value of the current

operating lease portfolio and increasing the

provision for residual value losses. However,

various other factors impact used vehicle values

and the projection of future residual values,

including the supply of and demand for used

vehicles, interest rates, inflation, the actual or

perceived quality, safety and reliability of vehicles,

the general economic outlook, new vehicle pricing,

projected vehicle return rates and projected loss

severity, which may offset this effect. Such factors

are highly likely to adversely affect the results of

operations for financial services due to significant

charges reducing the estimated residual value.

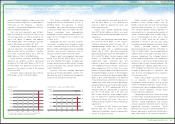

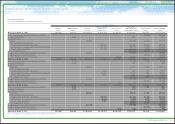

The following table illustrates the effect of an

assumed change in the vehicle return rate and

end-of-term market values, which Toyota believes

are the critical estimates, in determining the

residual value losses, holding all other assump-

tions constant. The following table represents the

impact on the residual value losses in Toyota’s

financial services operations of the change in

vehicle return rate and end-of-term market values

as those changes have a significant impact on

financial services operations.

Toyota periodically reviews the carrying value of

its long-lived assets held and used and assets to

be disposed of, including intangible assets, when

events and circumstances warrant such a review.

This review is performed using estimates of future

cash flows. If the carrying value of a long-lived

asset is considered impaired, an impairment

charge is recorded for the amount by which the

carrying value of the long-lived asset exceeds its

fair value. Management believes that the estimates

of future cash flows and fair values are reason-

able. However, changes in estimates of such

cash flows and fair values would affect the evalua-

tions and negatively affect future operating results

of the automotive operations.

Impairment of Long-Lived Assets

Yen in millions

Effect on the residual

value losses over the

remaining terms of the

operating leases on and

after April 1, 2011

1 percent increase in vehicle

return rate ¥1,164

1 percent increase in end-of-term

market values ¥4,490

Management's Discussion and Analysis of Financial Condition and Results of Operations

Pension costs and obligations are dependent on

assumptions used in calculating such amounts.

These assumptions include discount rates,

benefits earned, interest costs, expected rate of

return on plan assets, mortality rates and other

factors. Actual results that differ from the assump-

tions are accumulated and amortized over future

periods and, therefore, generally affect recognized

expense in future periods. While management

believes that the assumptions used are

appropriate, differences in actual experience or

changes in assumptions may affect Toyota’s

pension costs and obligations.

The two most critical assumptions impacting

the calculation of pension costs and obligations

are the discount rates and the expected rates of

returns on plan assets. Toyota determines the

discount rates mainly based on the rates of high

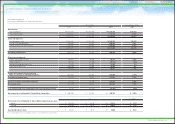

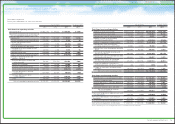

The following table illustrates the effects of assumed changes in weighted-average discount rates and

the weighted-average expected rate of return on plan assets, which Toyota believes are critical estimates

in determining pension costs and obligations, assuming all other assumptions are consistent.

quality fixed income bonds or fixed income

governmental bonds currently available and

expected to be available during the period to

maturity of the defined benefit pension plans.

Toyota determines the expected rates of return for

pension assets after considering several

applicable factors including, the composition of

plan assets held, assumed risks of asset manage-

ment, historical results of the returns on plan

assets, Toyota’s principal policy for plan asset

management, and forecasted market conditions.

A weighted-average discount rate of 2.8% and a

weighted-average expected rate of return on plan

assets of 3.8% are the results of assumptions

used for the various pension plans in calculating

Toyota’s consolidated pension costs for fiscal

2011. Also, a weighted-average discount rate of

2.8% is the result of assumption used for the

various pension plans in calculating Toyota’s

consolidated pension obligations for fiscal 2011.

Sensitivity analysis

Yen in millions

Effect on pre-tax income for

the year ended March 31, 2012 Effect on PBO

as of March 31, 2011

Discount rates

0.5% decrease ¥(10,325) ¥ 124,789

0.5% increase 9,845 (115,671)

Expected rate of return on plan assets

0.5% decrease ¥ (5,917)

0.5% increase 5,917

Pension Costs and Obligations

Natures of estimates and assumptions

Sensitivity analysis

Toyota uses derivatives in the normal course of

business to manage its exposure to foreign currency

exchange rates and interest rates. The accounting

for derivatives is complex and continues to evolve.

In addition, there are significant judgments and

estimates involved, using information from

Derivatives and Other Contracts at Fair Value

68TOYOTA ANNUAL REPORT 2011