Coca Cola 2011 Annual Report Download - page 121

Download and view the complete annual report

Please find page 121 of the 2011 Coca Cola annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

|

|

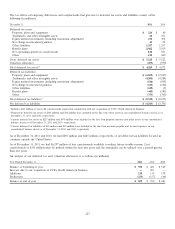

characteristics of each asset class, as well as the correlation of returns among asset classes. Our target allocation is a mix of

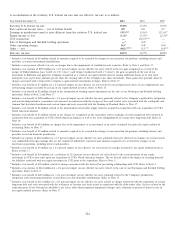

approximately 51 percent equity investments, 31 percent fixed-income investments and 18 percent in alternative investments.

Furthermore, we believe our target allocation will enable us to achieve the following long-term investment objectives:

(1) optimize the long-term return on plan assets at an acceptable level of risk;

(2) maintain a broad diversification across asset classes and among investment managers;

(3) maintain careful control of the risk level within each asset class; and

(4) focus on a long-term return objective.

The guidelines that have been established with each investment manager provide parameters within which the investment

managers agree to operate, including criteria that determine eligible and ineligible securities, diversification requirements and

credit quality standards, where applicable. Unless exceptions have been approved, investment managers are prohibited from

buying or selling commodities, futures or option contracts, as well as from short selling of securities. Additionally, investment

managers agree to obtain written approval for deviations from stated investment style or guidelines. As of December 31, 2011, no

investment manager was responsible for more than 10 percent of total U.S. plan assets.

Our target allocation of 51 percent equity investments is composed of approximately 39 percent domestic large-cap securities,

33 percent international securities and 28 percent domestic small-cap securities. Optimal returns through our investments in

domestic large-cap securities are achieved through security selection and sector diversification. Investments in common stock of

our Company accounted for approximately 12 percent of our investments in domestic large-cap securities and approximately

3 percent of total U.S. plan assets. Our investments in international securities are intended to provide equity-like returns, while at

the same time helping to diversify our overall equity investment portfolio. Our investments in domestic small-cap securities are

expected to experience larger swings in their market value on a periodic basis. Our investments in this asset class are selected

based on capital appreciation potential.

Our target allocation of 31 percent fixed-income investments is composed of 71 percent long-duration bonds and 29 percent

high-yield bonds. Long-duration bonds provide a stable rate of return through investments in high-quality publicly traded debt

securities. Our investments in long-duration bonds are diversified in order to mitigate duration and credit exposure. High-yield

bonds are investments in lower-rated and non-rated debt securities, which generally produce higher returns compared to

long-duration bonds. Investments in high-yield bonds also help diversify our fixed-income portfolio.

In addition to investments in equity securities and fixed-income investments, we have a target allocation of 18 percent in

alternative investments. These alternative investments include hedge funds, private equity limited partnerships, leveraged buyout

funds, international venture capital partnerships and real estate. The objective of investing in alternative investments is to provide

a higher rate of return than that available from publicly traded equity securities. These investments are inherently illiquid and

require a long-term perspective in evaluating investment performance.

Investment Strategy for Non-U.S. Pension Plans

As of December 31, 2011, the long-term target allocation for 42 percent of our international subsidiaries’ plan assets, primarily

certain of our European plans, is 60 percent equity securities and 40 percent fixed-income securities. The allocation for the

remaining 58 percent of the Company’s international subsidiaries’ plan assets consisted of 36 percent mutual, pooled and

commingled funds; 18 percent fixed-income securities; 14 percent equity securities; and 32 percent in other investments. The

investment strategies of our international subsidiaries differ greatly, and in some instances are influenced by local law. None of

our pension plans outside the United States is individually significant for separate disclosure.

Other Postretirement Benefit Plan Assets

Plan assets associated with other benefits primarily represent funding of the U.S. postretirement benefit plan through a U.S.

Voluntary Employee Beneficiary Association (‘‘VEBA’’), a tax-qualified trust. The VEBA assets remain segregated from the

primary U.S. pension master trust and are primarily invested in liquid assets due to the level of expected future benefit payments.

119