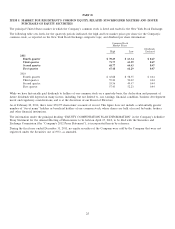

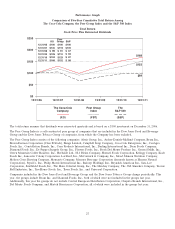

Coca Cola 2011 Annual Report Download - page 36

Download and view the complete annual report

Please find page 36 of the 2011 Coca Cola annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

|

|

Critical Accounting Policies and Estimates

Our consolidated financial statements are prepared in accordance with accounting principles generally accepted in the United

States, which require management to make estimates, judgments and assumptions that affect the amounts reported in our

consolidated financial statements and accompanying notes. We believe our most critical accounting policies and estimates relate to

the following:

• Principles of Consolidation

• Purchase Accounting for Acquisitions

• Recoverability of Noncurrent Assets

• Pension Plan Valuations

• Revenue Recognition

• Income Taxes

Management has discussed the development, selection and disclosure of critical accounting policies and estimates with the Audit

Committee of the Company’s Board of Directors. While our estimates and assumptions are based on our knowledge of current

events and actions we may undertake in the future, actual results may ultimately differ from these estimates and assumptions. For

a discussion of the Company’s significant accounting policies, refer to Note 1 of Notes to Consolidated Financial Statements.

Principles of Consolidation

Our Company consolidates all entities that we control by ownership of a majority voting interest as well as VIEs for which our

Company is the primary beneficiary. Generally, we consolidate only business enterprises that we control by ownership of a

majority voting interest. However, there are situations in which consolidation is required even though the usual condition of

consolidation (ownership of a majority voting interest) does not apply. Generally, this occurs when an entity holds an interest in

another business enterprise that was achieved through arrangements that do not involve voting interests, which results in a

disproportionate relationship between such entity’s voting interests in, and its exposure to the economic risks and potential

rewards of, the other business enterprise. This disproportionate relationship results in what is known as a variable interest, and the

entity in which we have the variable interest is referred to as a ‘‘VIE’’. An enterprise must consolidate a VIE if it is determined to

be the primary beneficiary of the VIE. The primary beneficiary has both (a) the power to direct the activities of the VIE that

most significantly impact the entity’s economic performance, and (b) the obligation to absorb losses or the right to receive benefits

from the VIE that could potentially be significant to the VIE.

Our Company holds interests in certain VIEs, primarily bottling and container manufacturing operations, for which we were not

determined to be the primary beneficiary. Our variable interests in these VIEs primarily relate to profit guarantees or

subordinated financial support. Refer to Note 11 of Notes to Consolidated Financial Statements. Although these financial

arrangements resulted in us holding variable interests in these entities, the majority of these arrangements did not empower us to

direct the activities of the VIEs that most significantly impact the VIEs’ economic performance. Our Company’s investments, plus

any loans and guarantees, related to these VIEs totaled $1,183 million and $1,274 million as of December 31, 2011 and 2010,

respectively, representing our maximum exposures to loss. The Company’s investments, plus any loans and guarantees, related to

these VIEs were not significant to the Company’s consolidated financial statements.

In addition, our Company holds interests in certain VIEs, primarily bottling and container manufacturing operations, for which we

were determined to be the primary beneficiary. As a result, we have consolidated these entities. Our Company’s investments, plus

any loans and guarantees, related to these VIEs totaled $199 million and $191 million as of December 31, 2011 and 2010,

respectively, representing our maximum exposures to loss. The assets and liabilities of VIEs for which we are the primary

beneficiary were not significant to the Company’s consolidated financial statements.

Creditors of our VIEs do not have recourse against the general credit of the Company, regardless of whether they are accounted

for as consolidated entities.

The information presented above reflects the impact of the Company’s adoption of accounting guidance issued by the FASB

related to VIEs in June 2009. This accounting guidance resulted in a change in our accounting policy effective January 1, 2010.

Among other things, the guidance requires more qualitative than quantitative analyses to determine the primary beneficiary of a

VIE, requires continuous assessments of whether an enterprise is the primary beneficiary of a VIE, enhances disclosures about an

enterprise’s involvement with a VIE, and amends certain guidance for determining whether an entity is a VIE.

Beginning January 1, 2010, we deconsolidated certain entities as a result of this change in accounting policy. These entities are

primarily bottling operations and had previously been consolidated due to certain loan guarantees and/or other financial support

34