Coca Cola 2011 Annual Report Download - page 75

Download and view the complete annual report

Please find page 75 of the 2011 Coca Cola annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

|

|

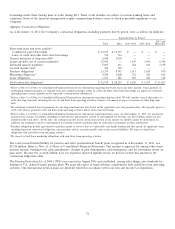

As of December 31, 2011, the projected benefit obligation of the U.S. qualified pension plans was $5,571 million, and the fair

value of plan assets was $4,274 million. The majority of this underfunding was due to the negative impact that the recent credit

crisis and financial system instability had on the value of our pension plan assets and the decrease in the weighted-average

discount rate used to calculate the Company’s benefit obligation.

As of December 31, 2011, the projected benefit obligation of all pension plans other than the U.S. qualified pension plans was

$2,684 million, and the fair value of all other pension plan assets was $1,897 million. The majority of this underfunding is

attributable to an international pension plan for certain non-U.S. employees that is unfunded due to tax law restrictions, as well as

our unfunded U.S. nonqualified pension plans. These U.S. nonqualified pension plans provide, for certain associates, benefits that

are not permitted to be funded through a qualified plan because of limits imposed by the Internal Revenue Code of 1986. The

expected benefit payments for these unfunded pension plans are not included in the table above. However, we anticipate annual

benefit payments for these unfunded pension plans to be approximately $60 million in 2012 and remain near that level through

2030, decreasing annually thereafter. Refer to Note 13 of Notes to Consolidated Financial Statements.

In 2012, we expect to contribute an additional $953 million to various plans, of which approximately $900 million was contributed

in the first quarter of 2012 to the Company’s U.S. pension plans. Refer to Note 13 of Notes to Consolidated Financial Statements.

We did not include our estimated contributions to our various plans in the table above.

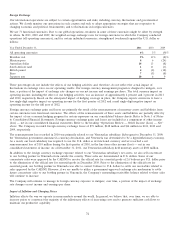

On December 14, 2011, the Company entered into a definitive agreement with Aujan Industries (‘‘Aujan’’), one of the largest

independent beverage companies in the Middle East, to acquire approximately half of the equity in Aujan’s existing beverage

business, excluding Aujan’s Iranian manufacturing and distribution business. Under the terms of the agreement, we will acquire

50 percent of the Aujan entity that holds the rights to Aujan-owned brands, and 49 percent of Aujan’s bottling and distribution

company, which will continue to hold the licensed brand Vimto. Total consideration for this investment, which will be accounted

for under the equity method, is approximately $980 million, which we expect to fund from our existing cash reserves. Closing of

the transaction is subject to certain conditions and is expected to occur in the first half of 2012. We did not include our

anticipated investment in Aujan in the table above.

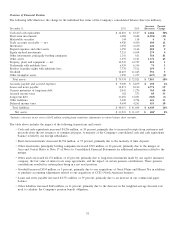

In general, we are self-insured for large portions of many different types of claims; however, we do use commercial insurance

above our self-insured retentions to reduce the Company’s risk of catastrophic loss. Our reserves for the Company’s self-insured

losses are estimated through actuarial procedures of the insurance industry and by using industry assumptions, adjusted for our

specific expectations based on our claim history. As of December 31, 2011, our self-insurance reserves totaled approximately

$527 million. Refer to Note 11 of Notes to Consolidated Financial Statements. We did not include estimated payments related to

our self-insurance reserves in the table above.

Deferred income tax liabilities as of December 31, 2011, were $4,713 million. Refer to Note 14 of Notes to Consolidated Financial

Statements. This amount is not included in the total contractual obligations table because we believe this presentation would not

be meaningful. Deferred income tax liabilities are calculated based on temporary differences between the tax bases of assets and

liabilities and their respective book bases, which will result in taxable amounts in future years when the liabilities are settled at

their reported financial statement amounts. The results of these calculations do not have a direct connection with the amount of

cash taxes to be paid in any future periods. As a result, scheduling deferred income tax liabilities as payments due by period could

be misleading, because this scheduling would not relate to liquidity needs.

73