Coca Cola 2011 Annual Report Download - page 71

Download and view the complete annual report

Please find page 71 of the 2011 Coca Cola annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

|

|

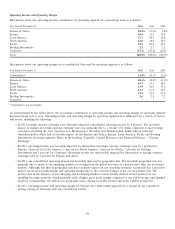

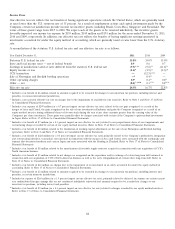

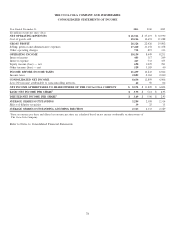

Cash Flows from Financing Activities

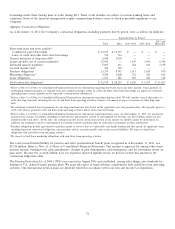

Our cash flows provided by (used in) financing activities were as follows (in millions):

Year Ended December 31, 2011 2010 2009

Issuances of debt $ 27,495 $ 15,251 $ 14,689

Payments of debt (22,530) (13,403) (12,326)

Issuances of stock 1,569 1,666 664

Purchases of stock for treasury (4,513) (2,961) (1,518)

Dividends (4,300) (4,068) (3,800)

Other financing activities 45 50 (2)

Net cash provided by (used in) financing activities $ (2,234) $ (3,465) $ (2,293)

Debt Financing

Our Company maintains debt levels we consider prudent based on our cash flows, interest coverage ratio and percentage of debt

to capital. We use debt financing to lower our overall cost of capital, which increases our return on shareowners’ equity. This

exposes us to adverse changes in interest rates. Our interest expense may also be affected by our credit ratings.

As of December 31, 2011, our long-term debt was rated ‘‘A+’’ by Standard & Poor’s, ‘‘Aa3’’ by Moody’s and ‘‘A+’’ by Fitch. Our

commercial paper program was rated ‘‘A-1’’ by Standard & Poor’s, ‘‘P-1’’ by Moody’s and ‘‘F-1’’ by Fitch. In assessing our credit

strength, all three agencies consider our capital structure (including the amount and maturity dates of our debt) and financial

policies as well as the aggregated balance sheet and other financial information for the Company. In addition, some rating

agencies also consider financial information for certain bottlers, including New CCE, Coca-Cola Amatil, Coca-Cola Bottling Co.

Consolidated, Coca-Cola FEMSA and Coca-Cola Hellenic. While the Company has no legal obligation for the debt of these

bottlers, the rating agencies believe the strategic importance of the bottlers to the Company’s business model provides the

Company with an incentive to keep these bottlers viable. It is our expectation that the credit rating agencies will continue using

this methodology. If our credit ratings were to be downgraded as a result of changes in our capital structure, our major bottlers’

financial performance, changes in the credit rating agencies’ methodology in assessing our credit strength, or for any other reason,

our cost of borrowing could increase. Additionally, if certain bottlers’ credit ratings were to decline, the Company’s share of equity

income could be reduced as a result of the potential increase in interest expense for these bottlers.

We monitor our financial ratios and, as indicated above, the rating agencies consider these ratios in assessing our credit ratings.

Each rating agency employs a different aggregation methodology and has different thresholds for the various financial ratios.

These thresholds are not necessarily permanent, nor are they always fully disclosed to our Company.

Our global presence and strong capital position give us access to key financial markets around the world, enabling us to raise

funds at a low effective cost. This posture, coupled with active management of our mix of short-term and long-term debt and our

mix of fixed-rate and variable-rate debt, results in a lower overall cost of borrowing. Our debt management policies, in conjunction

with our share repurchase programs and investment activity, can result in current liabilities exceeding current assets.

Issuances and payments of debt included both short-term and long-term financing activities. On December 31, 2011, we had

$4,625 million in lines of credit available for general corporate purposes, including commercial paper backup. These backup lines

of credit expire at various times from 2012 through 2016. There were no borrowings under these backup lines of credit during

2011. These credit facilities are subject to normal banking terms and conditions. Some of the financial arrangements require

compensating balances, none of which is presently significant to our Company.

In 2011, the Company had issuances of debt of $27,495 million, which included $25,219 million of issuances of commercial paper

and short-term debt with maturities greater than 90 days. The Company’s total issuances of debt also included long-term debt

issuances of $2,276 million, net of the debt issued to exchange a certain amount of our existing long-term debt. The Company

issued $2,979 million of long-term debt during 2011. We used $979 million of this newly issued debt and paid a premium of

$208 million to exchange $1,022 million of existing long-term debt that was assumed in connection with our acquisition of CCE’s

North American business in the fourth quarter of 2010. The remaining cash from the issuance was used to reduce the Company’s

outstanding commercial paper balance and exchange a certain amount of short-term debt.

69