Coca Cola 2011 Annual Report Download - page 123

Download and view the complete annual report

Please find page 123 of the 2011 Coca Cola annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

|

|

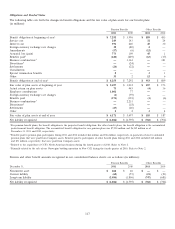

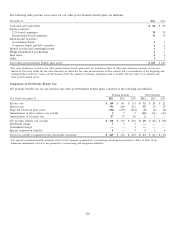

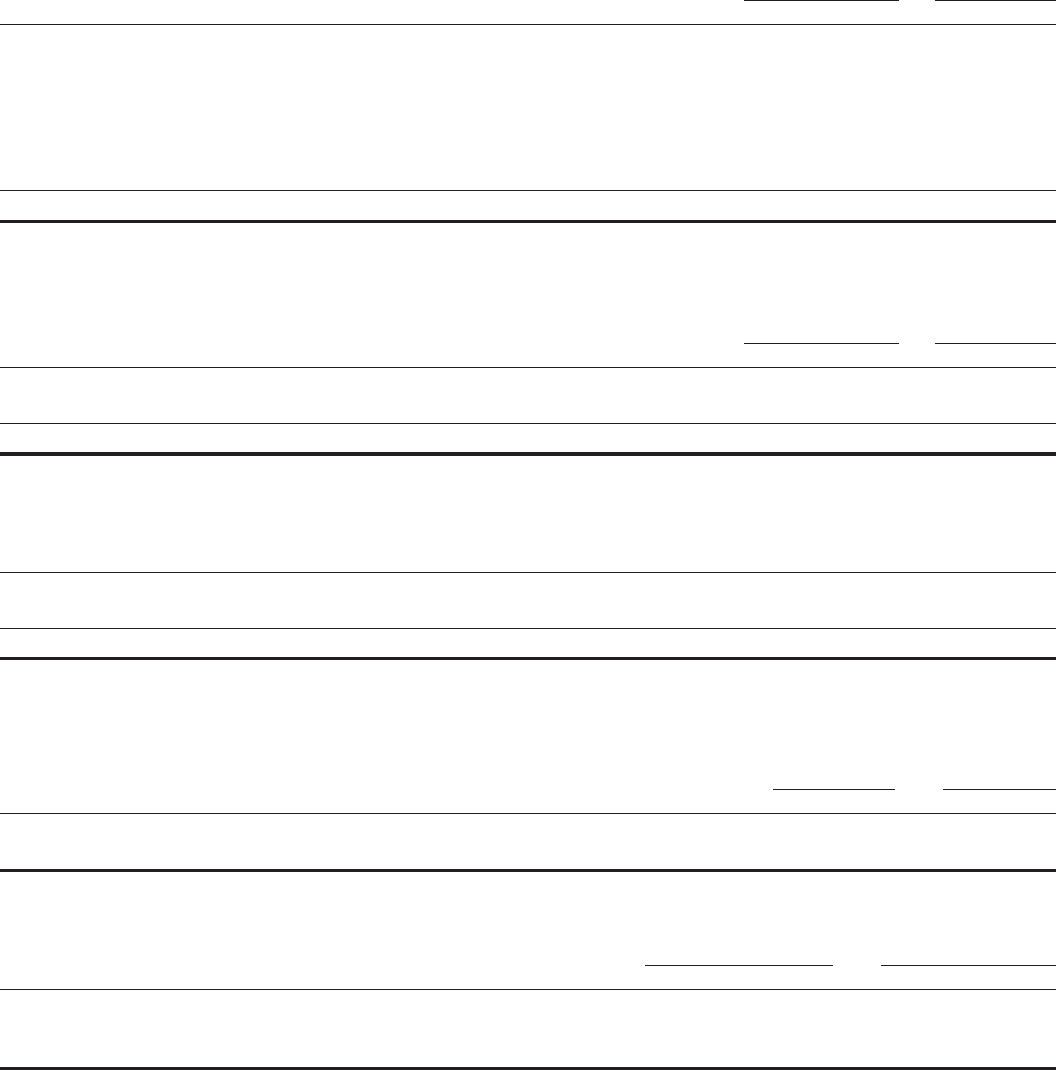

The following table sets forth the changes in AOCI for our benefit plans (in millions, pretax):

Pension Benefits Other Benefits

December 31, 2011 2010 2011 2010

Beginning balance in AOCI $ (1,006) $ (1,119) $72$ 118

Recognized prior service cost (credit) 55(61) (61)

Recognized net actuarial loss (gain) 90 63 23

Prior service credit (cost) arising in current year 57 612 —

Net actuarial (loss) gain arising in current year (1,194) 41 (57) 8

Impact of divestitures1—(8) ——

Translation gain (loss) (7) 6(2) 4

Ending balance in AOCI $ (2,055) $ (1,006) $ (34) $72

1Primarily related to the sale of our Norwegian bottling operation to New CCE. Refer to Note 2.

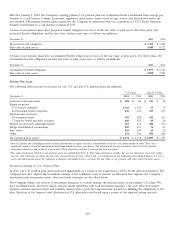

The following table sets forth amounts in AOCI for our benefit plans (in millions, pretax):

Pension Benefits Other Benefits

December 31, 2011 2010 2011 2010

Prior service credit (cost) $14$ (49) $73$ 122

Net actuarial loss (2,069) (957) (107) (50)

Ending balance in AOCI $ (2,055) $ (1,006) $ (34) $72

Amounts in AOCI expected to be recognized as components of net periodic pension cost in 2012 are as follows (in millions,

pretax):

Pension Benefits Other Benefits

Amortization of prior service cost (credit) $ (2) $ (52)

Amortization of actuarial loss 137 7

$ 135 $ (45)

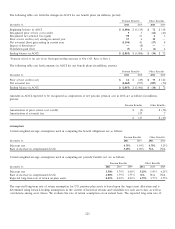

Assumptions

Certain weighted-average assumptions used in computing the benefit obligations are as follows:

Pension Benefits Other Benefits

December 31, 2011 2010 2011 2010

Discount rate 4.75% 5.50% 4.75% 5.25%

Rate of increase in compensation levels 3.25% 4.00% N/A N/A

Certain weighted-average assumptions used in computing net periodic benefit cost are as follows:

Pension Benefits Other Benefits

December 31, 2011 2010 2009 2011 2010 2009

Discount rate 5.50% 5.75% 6.00% 5.25% 5.50% 6.25%

Rate of increase in compensation levels 4.00% 3.75% 3.75% N/A N/A N/A

Expected long-term rate of return on plan assets 8.25% 8.00% 8.00% 4.75% 4.75% 4.75%

The expected long-term rate of return assumption for U.S. pension plan assets is based upon the target asset allocation and is

determined using forward-looking assumptions in the context of historical returns and volatilities for each asset class, as well as

correlations among asset classes. We evaluate the rate of return assumption on an annual basis. The expected long-term rate of

121