Coca Cola 2011 Annual Report Download - page 128

Download and view the complete annual report

Please find page 128 of the 2011 Coca Cola annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

|

|

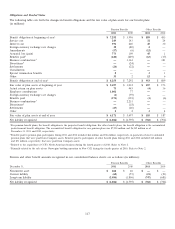

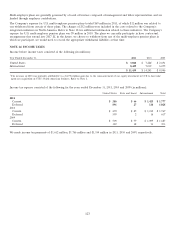

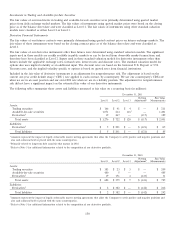

A reconciliation of the changes in the gross balance of unrecognized tax benefit amounts is as follows (in millions):

Year Ended December 31, 2011 2010 2009

Beginning balance of unrecognized tax benefits $ 387 $ 354 $ 369

Increases related to prior period tax positions 926 49

Decreases related to prior period tax positions (19) (10) (28)

Increases related to current period tax positions 633 16

Decreases related to current period tax positions (1) ——

Decreases related to settlements with taxing authorities (5) — (27)

Reductions as a result of a lapse of the applicable statute of limitations (46) (1) (73)

Increase related to acquisition of CCE’s North American business —6—

Increases (decreases) from effects of foreign currency exchange rates (11) (21) 48

Ending balance of unrecognized tax benefits $ 320 $ 387 $ 354

The Company recognizes accrued interest and penalties related to unrecognized tax benefits in income tax expense. The Company

had $110 million, $112 million and $94 million in interest and penalties related to unrecognized tax benefits accrued as of

December 31, 2011, 2010 and 2009, respectively. Of these amounts, $2 million of benefit, $17 million of expense and $16 million

of benefit was recognized through income tax expense in 2011, 2010 and 2009, respectively. If the Company were to prevail on all

uncertain tax positions, the reversal of this accrual would also be a benefit to the Company’s effective tax rate.

It is expected that the amount of unrecognized tax benefits will change in the next 12 months; however, we do not expect the

change to have a significant impact on our consolidated statements of income or consolidated balance sheets. These changes may

be the result of settlement of ongoing audits, statute of limitations expiring, or final settlements in transfer pricing matters that

are the subject of litigation. At this time, an estimate of the range of the reasonably possible outcomes cannot be made.

As of December 31, 2011, undistributed earnings of the Company’s foreign subsidiaries amounted to $23.5 billion. Those earnings

are considered to be indefinitely reinvested and, accordingly, no U.S. federal and state income taxes have been provided thereon.

Upon distribution of those earnings in the form of dividends or otherwise, the Company would be subject to both U.S. income

taxes (subject to an adjustment for foreign tax credits) and withholding taxes payable to the various foreign countries.

Determination of the amount of unrecognized deferred U.S. income tax liability is not practical because of the complexities

associated with its hypothetical calculation; however, unrecognized foreign tax credits would be available to reduce a portion of

the U.S. tax liability.

126