Coca Cola 2011 Annual Report Download - page 49

Download and view the complete annual report

Please find page 49 of the 2011 Coca Cola annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

|

|

Impact of New Accounting Guidance

Beginning January 1, 2010, we deconsolidated certain entities as a result of the Company’s adoption of new accounting guidance

issued by the FASB. These entities are primarily bottling operations, and the Company accounted for them under the equity

method of accounting upon deconsolidation. The entities that were deconsolidated as a result of this change in accounting

guidance accounted for 3 percent of the Company’s consolidated net operating revenues and less than 1 percent of net income

attributable to shareowners of The Coca-Cola Company in 2009. Refer to the heading ‘‘Critical Accounting Policies and

Estimates — Principles of Consolidation’’ above. These entities accounted for 4 percent of the Company’s equity income in 2010.

Refer to the heading ‘‘Equity Income (Loss) — Net’’ below. The impact that the deconsolidation of these entities had on net

operating revenues was included as a structural change. Refer to the heading ‘‘Net Operating Revenues’’ below.

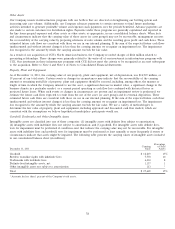

Beverage Volume

We measure the volume of Company beverage products sold in two ways: (1) unit cases of finished products and (2) concentrate

sales. As used in this report, ‘‘unit case’’ means a unit of measurement equal to 192 U.S. fluid ounces of finished beverage (24

eight-ounce servings); and ‘‘unit case volume’’ means the number of unit cases (or unit case equivalents) of Company beverage

products directly or indirectly sold by the Company and its bottling partners to customers. Unit case volume primarily consists of

beverage products bearing Company trademarks. Also included in unit case volume are certain products licensed to, or distributed

by, our Company, and brands owned by Coca-Cola system bottlers for which our Company provides marketing support and from

the sale of which we derive economic benefit. In addition, unit case volume includes sales by joint ventures in which the Company

has an equity interest. We believe unit case volume is one of the measures of the underlying strength of the Coca-Cola system

because it measures trends at the consumer level. The unit case volume numbers used in this report are derived based on

estimates received by the Company from its bottling partners and distributors. Concentrate sales volume represents the amount of

concentrates and syrups (in all cases expressed in equivalent unit cases) sold by, or used in finished beverages sold by, the

Company to its bottling partners or other customers. Unit case volume and concentrate sales volume growth rates are not

necessarily equal during any given period. Factors such as seasonality, bottlers’ inventory practices, supply point changes, timing of

price increases, new product introductions and changes in product mix can impact unit case volume and concentrate sales volume

and can create differences between unit case volume and concentrate sales volume growth rates. In addition to the items

mentioned above, the impact of unit case volume from certain joint ventures, in which the Company has an equity interest, but to

which the Company does not sell concentrates or syrups, may give rise to differences between unit case volume and concentrate

sales volume growth rates.

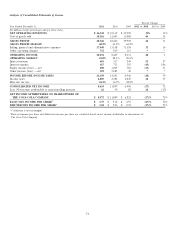

Information about our volume growth by operating segment is as follows:

Percent Change

2011 vs. 2010 2010 vs. 2009

Concentrate Concentrate

Year Ended December 31, Unit Cases1,2 Sales Unit Cases1,2 Sales

Worldwide 5% 5% 5% 5%

Eurasia & Africa 6% 5% 12% 12%

Europe 21——

Latin America 6557

North America 4422

Pacific 5666

Bottling Investments — N/A (1) N/A

1Bottling Investments operating segment data reflects unit case volume growth for consolidated bottlers only.

2Geographic segment data reflects unit case volume growth for all bottlers in the applicable geographic areas, both consolidated and unconsolidated.

47