Sysco 2012 Annual Report Download - page 76

Download and view the complete annual report

Please find page 76 of the 2012 Sysco annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

|

|

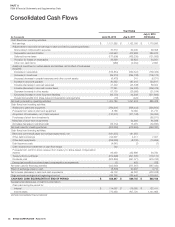

SYSCO CORPORATION-Form10-K 53

PARTII

ITEM8Financial Statements and Supplementary Data

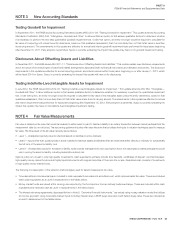

NOTE3 New Accounting Standards

Testing Goodwill for Impairment

In September2011, the FASB issued Accounting Standards Update (ASU) 2011-08, “Testing Goodwill for Impairment.” This update amends Accounting

Standards Codifi cation (ASC) 350, “Intangibles—Goodwill and Other” to allow entities an option to fi rst assess qualitative factors to determine whether

it is necessary to perform the two-step quantitative goodwill impairment test. Under that option, an entity no longer would be required to calculate the

fair value of a reporting unit unless the entity determines, based on that qualitative assessment, that it is more likely than not that its fair value is less than

its carrying amount. The amendments in this update are effective for annual and interim goodwill impairment tests performed for fi scal years beginning

after December15,2011. Early adoption is permitted. Sysco is currently evaluating the impact this update may have on its goodwill impairment testing.

Disclosures About Offsetting Assets and Liabilities

In December2011, the FASB issued ASU 2011-11, “Disclosures About Offsetting Assets and Liabilities.” This update creates new disclosure requirements

about the nature of an entity’s rights of setoff and related arrangements associated with its fi nancial instruments and derivative instruments. The disclosure

requirements in this update are effective for annual reporting periods, and interim periods within those years, beginning on or after January1,2013, which

will be fi scal 2014 for Sysco. Sysco is currently evaluating the impact this update will have on its disclosures.

Testing Indefi nite-Lived Intangible Assets for Impairment

In July2012, the FASB issued ASU 2012-02, “Testing Indefi nite-Lived Intangible Assets for Impairment.” This update amends ASC 350, “Intangibles—

Goodwill and Other” to allow entities an option to fi rst assess qualitative factors to determine whether it is necessary to perform the quantitative impairment

test. Under that option, an entity no longer would be required to calculate the fair value of the intangible asset unless the entity determines, based on that

qualitative assessment, that it is more likely than not that its fair value is less than its carrying amount. The amendments in this update are effective for annual

and interim impairment tests performed for fi scal years beginning after September15,2012. Early adoption is permitted. Sysco is currently evaluating the

impact this update may have on its indefi nite-lived intangibles impairment testing.

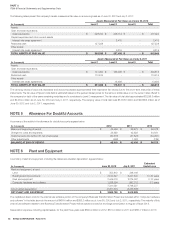

NOTE4 Fair Value Measurements

Fair value is defi ned as the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the

measurement date (i.e. an exit price). The accounting guidance includes a fair value hierarchy that prioritizes the inputs to valuation techniques used to measure

fair value. The three levels of the fair value hierarchy are as follows:

•Level1– Unadjusted quoted prices for identical assets or liabilities in active markets;

•

Level2– Inputs other than quoted prices in active markets for identical assets and liabilities that are observable either directly or indirectly for substantially

the full term of the asset or liability; and

•

Level3– Unobservable inputs for the asset or liability, which include management’s own assumption about the assumptions market participants would

use in pricing the asset or liability, including assumptions about risk.

Sysco’s policy is to invest in only high-quality investments. Cash equivalents primarily include time deposits, certifi cates of deposit, commercial paper,

high-quality money market funds and all highly liquid instruments with original maturities of three months or less. Restricted cash consists of investments

in high-quality money market funds.

The following is a description of the valuation methodologies used for assets measured at fair value.

•

Time deposits and commercial paper included in cash equivalents are valued at amortized cost, which approximates fair value. These are included

within cash equivalents as a Level2 measurement in the tables below.

•

Money market funds are valued at the closing price reported by the fund sponsor from an actively traded exchange. These are included within cash

equivalents and restricted cash as Level1 measurements in the tables below.

•

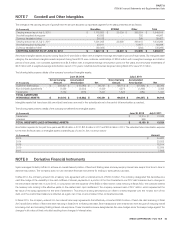

The interest rate swap agreements, discussed further in Note8, “Derivative Financial Instruments,” are valued using a swap valuation model that utilizes

an income approach using observable market inputs including interest rates, LIBOR swap rates and credit default swap rates. These are included as

a Level2 measurement in the tables below.