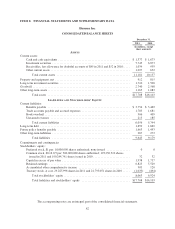

Humana 2011 Annual Report Download - page 102

Download and view the complete annual report

Please find page 102 of the 2011 Humana annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

|

|

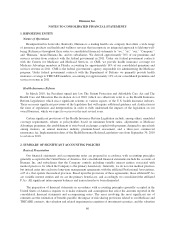

Humana Inc.

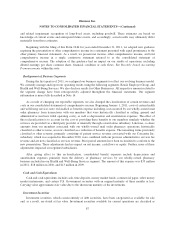

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

ranging from 3 to 10 years for equipment, 3 to 7 years for computer software, and 20 to 40 years for buildings.

Improvements to leased facilities are depreciated over the shorter of the remaining lease term or the anticipated

life of the improvement.

We periodically review long-lived assets, including property and equipment and other intangible assets, for

impairment whenever adverse events or changes in circumstances indicate the carrying value of the asset may not

be recoverable. Losses are recognized for a long-lived asset to be held and used in our operations when the

undiscounted future cash flows expected to result from the use of the asset are less than its carrying value. We

recognize an impairment loss based on the excess of the carrying value over the fair value of the asset.

A long-lived asset held for sale is reported at the lower of the carrying amount or fair value less costs to sell.

Depreciation expense is not recognized on assets held for sale. Losses are recognized for a long-lived asset to be

abandoned when the asset ceases to be used. In addition, we periodically review the estimated lives of all

long-lived assets for reasonableness.

Goodwill and Other Intangible Assets

Goodwill represents the unamortized excess of cost over the fair value of the net tangible and other

intangible assets acquired. We are required to test at least annually for impairment at a level of reporting referred

to as the reporting unit, and more frequently if adverse events or changes in circumstances indicate that the asset

may be impaired. A reporting unit either is our operating segments or one level below the operating segments,

referred to as a component, which comprise our reportable segments. A component is considered a reporting unit

if the component constitutes a business for which discrete financial information is available that is regularly

reviewed by management. We aggregate the components of an operating segment into one reporting unit if they

have similar economic characteristics. Goodwill is assigned to the reporting unit that is expected to benefit from

a specific acquisition. As discussed previously under Realignment of Business Segments within this Note 2,

during the first quarter of 2011, we realigned our business segments to reflect our evolving business model. As a

result, we reassigned goodwill to our new reporting units as of January 1, 2011 using the relative fair value

approach based on an evaluation of future discounted cash flows as discussed in Note 8.

We use a two-step process to review goodwill for impairment. The first step is a screen for potential

impairment, and the second step measures the amount of impairment, if any. Impairment tests are performed, at a

minimum, in the fourth quarter of each year supported by our long-range business plan and annual planning

process. We rely on an evaluation of future discounted cash flows to determine fair value of our reporting units.

Impairment tests completed for 2011, including an interim test completed January 1 in connection with the

segment realignment, 2010 and 2009 did not result in an impairment loss. Beginning in 2012, we are allowed to

first assess qualitative factors to determine whether it is necessary to perform the two-step quantitative goodwill

impairment test. See Recently Issued Accounting Pronouncements within this note.

Other intangible assets primarily relate to acquired customer contracts/relationships and are included with

other long-term assets in the consolidated balance sheets. Other intangible assets are amortized over the useful

life, based upon the pattern of future cash flows attributable to the asset. This sometimes results in an accelerated

method of amortization for customer contracts because the asset tends to dissipate at a more rapid rate in earlier

periods. Other than customer contracts, other intangible assets generally are amortized using the straight-line

method. We review other finite-lived intangible assets for impairment under our long-lived asset policy.

Benefits Payable and Benefit Expense Recognition

Benefit expenses include claim payments, capitation payments, pharmacy costs net of rebates, allocations of

certain centralized expenses and various other costs incurred to provide health insurance coverage to members, as

well as estimates of future payments to hospitals and others for medical care and other supplemental benefits

92